QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Veterinary Absorbable Sutures- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Veterinary Absorbable Sutures market, including market size, share, demand, industry development status, and forecasts for the next few years.

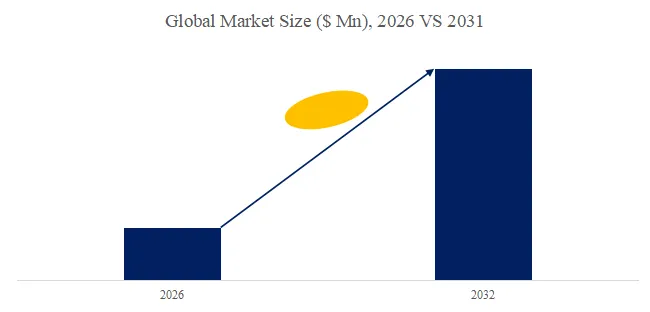

The global market for Veterinary Absorbable Sutures was estimated to be worth US$ 553 million in 2024 and is forecast to a readjusted size of US$ 854 million by 2031 with a CAGR of 6.4% during the forecast period 2025-2031.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/4842908/veterinary-absorbable-sutures

Veterinary Absorbable Sutures Market Summary

According to the latest report “Global Veterinary Absorbable Sutures Market Report 2025-2031″ by the QYResearch research team, the global Veterinary Absorbable Sutures market size is expected to reach US$1.96 billion in 2031, with a compound annual growth rate (CAGR) of 6.15% in the next few years.

Veterinary Absorbable Sutur are suture materials specifically designed for animal surgery. They are characterized by gradual degradation and absorption by the tissue within the body, avoiding postoperative suture removal. These sutures are typically made from natural polymers (such as catgut and collagen) or synthetic polymers (such as polylactic acid and polyglycolic acid), possessing good tensile strength, flexibility, and ligation properties, adaptable to the suturing needs of various tissue types. Based on absorption rate and tissue healing cycle, they can be divided into fast-absorbing and slow-absorbing types, meeting the suturing requirements of skin, muscle, internal organs, and blood vessels. Absorbable sutures for veterinary use are widely applied in surgical procedures on pets, livestock, and wild animals, including wound closure, organ surgery, and reconstructive surgery. They reduce the need for secondary procedures, lower the risk of infection, and promote tissue repair and wound healing, making them an indispensable consumable in modern veterinary surgery.

The veterinary absorbable suture market is a relatively limited but highly specialized, steadily growing, and promising segment. Its development is deeply dependent on the booming global pet economy and the technological upgrades in modern animal husbandry. This market will be characterized by both material innovation-driven growth and differentiated competition. In terms of technological innovation, next-generation products will focus on faster absorption rates, stronger initial tension retention, better flexibility, and the addition of antibacterial coatings (such as triclosan) or growth factors to meet the needs of complex wounds and high-risk surgeries. Simultaneously, the development of specialized sutures for different animal species and tissues (such as fascia, subcutaneous tissue, and mucous membranes) will be an important direction for product differentiation. In terms of business models, with the increasing prevalence of pet insurance and the growing intensification of animal husbandry, the market will pay increasing attention to product efficacy evidence (evidence-based veterinary medicine) and total lifecycle costs. This requires suppliers to not only provide products but also complementary surgical technical support and training. Overall, while the veterinary absorbable suture market is not a mass market, its growth is closely tied to the overall development of the animal health industry, making it a technology-intensive, value-driven, and promising specialized sector.

The driving factors influencing the development of absorbable sutures for veterinary use primarily stem from the continuous growth in animal medical needs and the improvement in surgical techniques. With the increasing number of pets and the large-scale development of livestock farming, the demand for high-quality, safe, and easy-to-handle suture materials is constantly rising, especially in surgeries involving small pets, special livestock and poultry, and wild animals. Absorbable sutures can reduce postoperative suture removal and lower the risk of infection, thus becoming one of the routine consumables in veterinary surgery.

The improvement of regulations and standards is also an important driving factor. Increasingly stringent regulations on the safety, sterility, and biocompatibility of animal medical devices in various countries have prompted manufacturers to continuously improve material performance, control degradation rates, and develop multi-specification sutures suitable for different surgical types to meet compliance requirements and clinical safety standards, thereby increasing market acceptance.

Technological advancements are also a core driving force for industry development. Advances in polymer materials science have optimized the strength, flexibility, absorption period, and ligation performance of sutures. Furthermore, surface modification or drug encapsulation can achieve antibacterial and anti-inflammatory functions, further enhancing their clinical application value. Furthermore, the trends towards digitalization and minimally invasive procedures in veterinary surgery are driving the development of sutures towards easier operation and compatibility with minimally invasive instruments, providing technical support for product innovation and market expansion.

Finally, rising awareness of animal health and the development of the pet economy are also boosting market demand. Pet owners’ emphasis on postoperative recovery and wound healing quality, along with livestock companies’ requirements for growth performance and disease control, are leading to a continuous increase in the use of high-performance, absorbable sutures in veterinary clinics, providing a sustained market driving force for industry development.

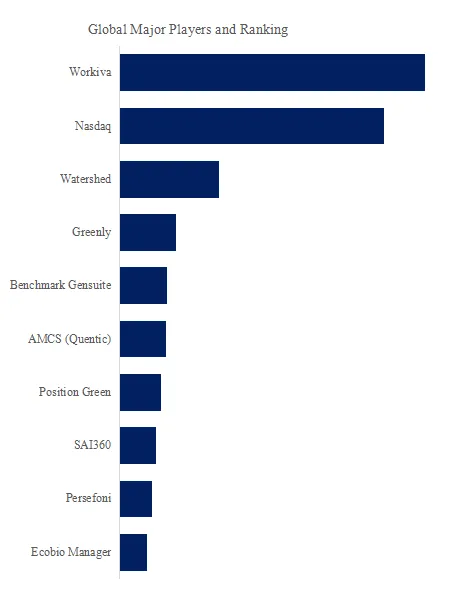

This report profiles key players of Veterinary Absorbable Sutures such as Katsan Medical Devices、MEDTRONIC、Boz Medical、Medico、VMG Vitrex Medical Group、Universal Sutures、Unisur Lifecare、Shandong Haidike Medical Products Co.,Ltd.、CROWNJUN、Orion Sutures、Lotus Surgicals、Corza Medical、Medico、VeterSut、Shanghai Yuyan Instruments Co.,Ltd.、Shinva Medical Instrument、Worldwide Medivest

The veterinary absorbable suture industry chain mainly consists of the following aspects: The upstream supply of raw materials and core technologies is fundamental to determining product performance and biosafety.

This segment has high technological barriers, primarily driven by polymer synthesis and processing technologies. Core raw materials fall into two main categories: first, synthetic polymers such as polyglycolic acid, polylactic acid, polydioxanone, and polycaprolactone. The molecular weight, purity, and copolymerization ratio of these materials directly determine the suture’s absorption period, mechanical strength, and tissue reactivity; second, natural materials such as catgut (collagen) and emerging materials like chitosan and silk fibroin, which possess good biocompatibility but whose performance control is more complex. In addition, special additives (such as barium sulfate for imaging and antibacterial agents for anti-infection), dyes, and precision spinning and coating equipment are also key upstream links. Core competitiveness in this field is held by a few chemical companies with capabilities in medical-grade polymer synthesis and precision processing.

The midstream of the industry chain involves suture design, spinning, post-processing, and sterilization, which are the core of value creation and product finalization.

Manufacturers process upstream raw materials into monofilaments or multifilaments using processes such as melt spinning or solution spinning. This process involves several precision technologies: spinning process control determines the thread’s diameter uniformity and initial strength; stretching and annealing optimize its crystallinity and mechanical properties; surface coating technologies (such as lubricating coatings) improve its feel, knotting performance, and smoothness through tissue; and integrated needle-thread forming and connection technologies directly affect surgical efficiency. Subsequently, the product undergoes rigorous cleaning, slitting, and packaging, and is ultimately sterilized using ethylene oxide or irradiation. Midstream companies can be divided into comprehensive giants spanning human and veterinary medicine (leveraging their human medical device technology, production capacity, and certification systems for backward compatibility) and specialized manufacturers focused on animal health. Their core competitiveness lies in a deep understanding of animal tissue healing characteristics, specialized product lines, cost control capabilities, and quality control systems that comply with veterinary regulations.

Downstream in the industry chain are distribution, clinical applications, and end markets, directly realizing the final value of the product.

Professional veterinary medical device distributors are key channels connecting manufacturers and end-users, responsible for warehousing, logistics, academic promotion, and technical training for veterinarians. End-users fall into two distinct markets: the companion animal (pet) medical market, primarily served by veterinary hospitals and clinics, driven by a demand for minimally invasive procedures, sutureless procedures, and rapid recovery, with products trending towards high-end, sophisticated techniques, similar to high-end human surgery; and the livestock market, primarily served by large-scale breeding groups, ranches, and veterinary stations, where the core needs are ease of use, cost-effectiveness, and efficient herd health management, with products emphasizing standardization, bulk packaging, and reliability. Additionally, wildlife conservation organizations, zoos, and equestrian clubs are also important niche customers. Veterinarians’ usage habits, brand awareness, and surgical training have a decisive influence on product selection.

Throughout the entire industry chain lies a unique regulatory, technological, and market-driven system. While veterinary products typically do not require the extremely lengthy and expensive clinical trials seen in human medical products, they still must comply with the regulatory requirements for veterinary drugs or veterinary medical devices in various countries to ensure their safety and efficacy. The trend of pets becoming “family members,” leading to consumption upgrades, and the large-scale and welfare-oriented development of the livestock industry are two core market drivers. Continuous R&D and innovation not only follow advancements in human medical materials science but also focus on developing specialized products for specific animals (such as ruminants with unique absorption and metabolism characteristics) and specific surgeries (such as orthopedics and ophthalmology). Comprehensive veterinary education and cooperation (establishing professional recognition through sponsored training and surgical demonstrations) are key to building a competitive advantage for brands. Ultimately, the value of this industry chain lies not only in providing an absorbable suture but also in offering a complete solution for animal surgery that promotes healing, reduces pain, and improves overall medical or production efficiency.

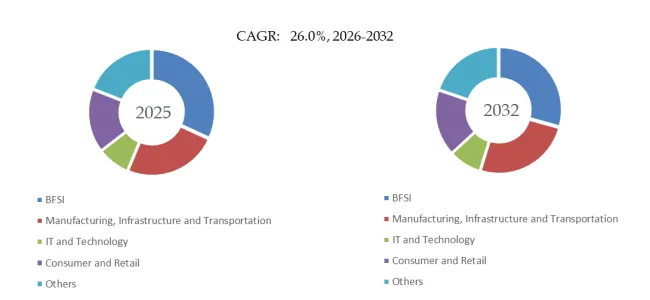

The competitive landscape of veterinary absorbable sutures mainly exhibits the following characteristics: From a segmented perspective, the competitive landscape of veterinary absorbable sutures is primarily characterized by differentiated competition based on product type and material technology. On the one hand, based on material source, sutures can be divided into natural polymer sutures (such as catgut and collagen) and synthetic polymer sutures (such as polylactic acid and polyglycolic acid). The former has good biocompatibility and mild absorption, making it suitable for general tissue suturing; the latter offers strong controllability, high strength, and adjustable degradation cycles, making it suitable for high-stress or deep tissue suturing. On the other hand, based on absorption cycle, sutures can be divided into fast-absorbing, standard-absorbing, and slow-absorbing types to meet the needs of different surgical sites and healing periods. Some high-end products also possess antibacterial, anti-inflammatory, or drug-encapsulated functions, creating diversified competition in technological approaches.

From the perspective of company type, the market presents a pattern of international brands and local manufacturers operating in parallel. Internationally renowned medical consumable companies from Europe, America, and Japan hold an advantage in the high-end pet healthcare and professional livestock markets due to their R&D strength, product certifications, brand trust, and global sales and service networks. Meanwhile, local manufacturers in China and other emerging markets have significant advantages in price, customized specifications, rapid supply, and local after-sales service, especially in small and medium-sized animal hospitals and local farms. Furthermore, some companies venturing into medical materials or biopolymers are also establishing new competitive strength in the high-end, differentiated market through material innovation and product functional extensions.

Overall, the veterinary absorbable suture industry exhibits competitive characteristics of “diverse materials and technological routes, diverse company types, and significant regional differentiation.” The high-end market is dominated by international brands, while competition in the mid-to-low-end and localized markets is fierce. In the future, with the growth of the pet economy, improvements in surgical techniques, and the development of functional suture technology, comprehensive manufacturers capable of combining biocompatibility, controllable absorption, and additional functions are expected to increase their market share, driving a gradual increase in industry concentration.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Veterinary Absorbable Sutures market is segmented as below:

By Company

Katsan Medical Devices

MEDTRONIC

Boz Medical

Medico

VMG Vitrex Medical Group

AIP Medical

Unisur Lifecare

Haidike

CROWNJUN

Orion Sutures

Lotus Surgicals

Corza Medical

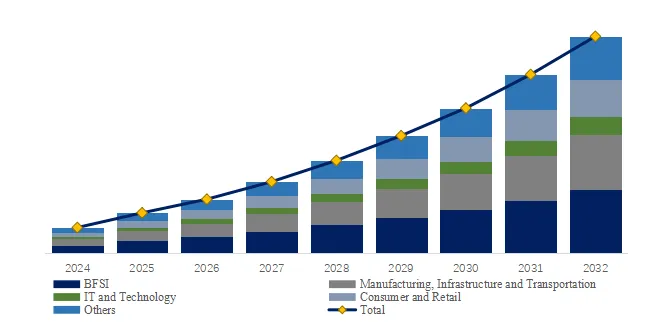

Segment by Type

Natural Polymers

Synthetic Polyesters

Polylactic Acid

Copolymers

Others

Segment by Application

Pets

Livestock

Aquatic Animals

Others

Each chapter of the report provides detailed information for readers to further understand the Veterinary Absorbable Sutures market:

Chapter 1: Introduces the report scope of the Veterinary Absorbable Sutures report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Veterinary Absorbable Sutures manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Veterinary Absorbable Sutures market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

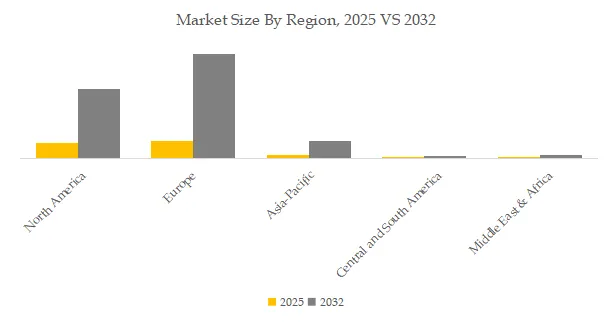

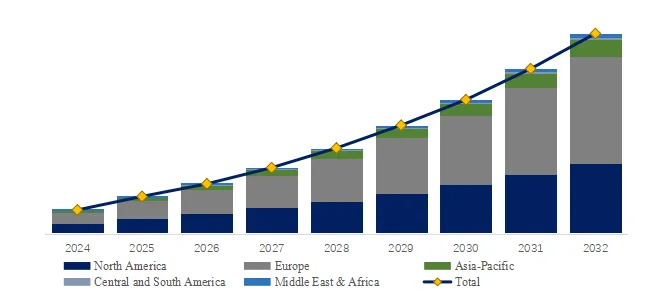

Chapter 5: Sales, revenue of Veterinary Absorbable Sutures in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Veterinary Absorbable Sutures in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Veterinary Absorbable Sutures competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Veterinary Absorbable Sutures comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Veterinary Absorbable Sutures market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Veterinary Absorbable Sutures Market Research Report 2025

Global Veterinary Absorbable Sutures Market Outlook, In‑Depth Analysis & Forecast to 2031

Global Veterinary Absorbable Sutures Sales Market Report, Competitive Analysis and Regional Opportunities 2025-2031

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp