QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Single-acting Pneumatic Actuator- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Single-acting Pneumatic Actuator market, including market size, share, demand, industry development status, and forecasts for the next few years.

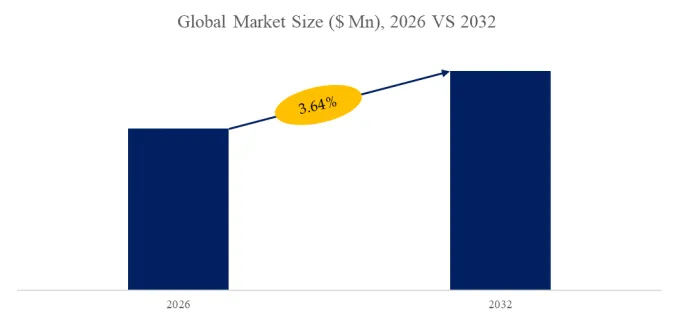

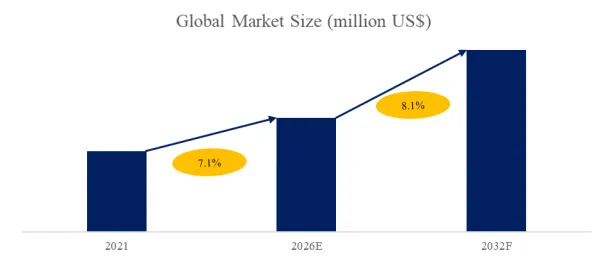

The global market for Single-acting Pneumatic Actuator was estimated to be worth US$ 601 million in 2025 and is projected to reach US$ 909 million, growing at a CAGR of 6.1% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5990335/single-acting-pneumatic-actuator

Single-acting Pneumatic Actuator Market Summary

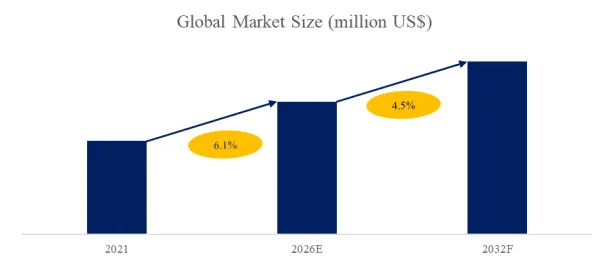

According to the latest report “Global Single-acting Pneumatic Actuator Market Report 2025-2031″ by the QYResearch research team, the global Single-acting Pneumatic Actuator market size is expected to reach US$0.91 billion in 2031, with a compound annual growth rate (CAGR) of 6.1% in the next few years.

A single-acting pneumatic actuator is an automated actuator that uses compressed air as a power source, is driven by air pressure on only one side, and is reset by a spring or external force. It is mainly used to open or close valves or mechanisms. Its basic structure typically consists of a cylinder, piston, return spring, sealing assembly, and connecting mechanism. During operation, compressed air enters the cylinder and pushes the piston to produce linear or rotary motion, completing the actuation action. When the air source is disconnected or fails, the built-in spring automatically releases energy, returning the actuator to its initial safe position. Compared to double-acting pneumatic actuators, single-acting pneumatic actuators have a simpler structure, require less air, and possess the inherent safety characteristic of automatic reset upon air loss, making them particularly suitable for applications with high safety requirements. These actuators are widely used in on/off valve control scenarios in petrochemical, natural gas, energy, power, water treatment, and process industries, often for emergency shut-off, fail-safe closure, or system opening. Based on the output form, single-acting pneumatic actuators can be divided into two main categories: linear stroke and rotary stroke. Their core advantages lie in safety, reliability, rapid response, and low maintenance costs, making them one of the common and critical actuators in industrial automation control systems.

The single-acting pneumatic actuator market is experiencing steady growth, benefiting from the global trend of industrial automation and smart manufacturing. As industries increasingly demand higher production efficiency, reliability, and safety, single-acting pneumatic actuators, with their simple structure, low maintenance costs, and fast response speed, are gradually becoming the preferred solution for factory automation, process control, and valve actuation. Simultaneously, the growing demand for energy conservation, emission reduction, and equipment intelligence in sectors such as new energy, environmental protection, petrochemicals, and chemicals provides sustained market momentum for this product.

In the future, product upgrades will focus on high-precision control, high-temperature and high-pressure resistance, and IoT connectivity to meet the needs of smart factories and remote operation and maintenance. Furthermore, while the domestic and international market competition remains dominated by a few large enterprises, small and medium-sized enterprises (SMEs) also have significant growth potential through differentiated products and customized services. Therefore, while maintaining stable growth, the single-acting pneumatic actuator market also presents significant opportunities for technological innovation and supply chain integration.

The primary driver of the development of single-acting pneumatic actuators is the continuous improvement in industrial safety and regulatory requirements. In high-risk industries such as petrochemicals, natural gas, energy, and chemical plants, automatic reset upon gas loss is considered a critical safety function. Increasingly, safety regulations and engineering standards require valves to return to a preset safe position when the gas supply is interrupted. This directly drives the increased application of single-acting pneumatic actuators in emergency shut-off valves and critical control points.

The second important driving factor is the demand for automation and equipment upgrades in process industries. With the increase in the replacement of aging equipment and new projects, companies are placing greater emphasis on system reliability and simplification. Single-acting pneumatic actuators have a relatively simple structure, fewer gas paths, and lower maintenance difficulty, making them particularly suitable for on/off valves and high-frequency operation scenarios, ensuring stable demand in automation upgrades and replacement of existing equipment.

Third, energy structure adjustments and infrastructure construction are also key driving forces. The large-scale construction and expansion of oil and gas pipelines, LNG receiving terminals, chemical industrial parks, and water treatment facilities have significantly increased the demand for actuators with fail-safe characteristics. Single-acting pneumatic actuators, due to their inherent safety attributes, have become the preferred choice in these infrastructure projects.

Furthermore, cost control and system integration requirements also influence market development. Compared to double-acting actuators, single-acting products offer advantages in terms of air source configuration, number of control components, and system complexity, helping to reduce overall system costs. They are particularly favored by small and medium-sized engineering projects and the standardized valve supply market.

Finally, advancements in materials and manufacturing processes have also supported the development of single-acting pneumatic actuators. The application of high-performance spring materials, sealing technologies, and anti-corrosion coatings significantly improves the actuator’s lifespan and stability, enabling it to withstand higher pressures, greater corrosiveness, and more complex industrial conditions, thereby broadening its application scope and extending its product lifecycle.

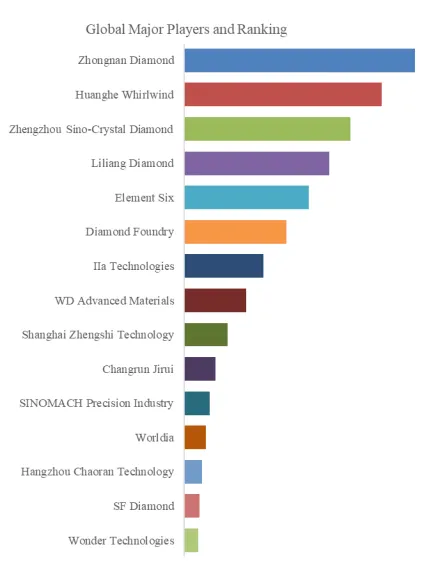

This report profiles key players of Single-acting Pneumatic Actuator such as MT Valves & Fittings、Uflow Automation、COVNA、EBRO ARMATUREN、Quifer Actuators, SL、Autorun Control Valve Co.,Ltd、JUHANG、Marsh Automation、Aira Euro Automation、FREYA、FLOWX、ZHONGZHI VALVE GROUP、ACTUATECH、SHANGHAI QUGONG VALVE PIPE ENGINEERING CO.,LTD、Huaershi、Kinetrol、VINCER.

The supply chain for single-acting pneumatic actuators is a typical technology-intensive precision manufacturing and system integration chain, mainly comprising the following aspects:

The upstream segment begins with the supply of core basic materials.

This segment is highly specialized, primarily including high-strength aluminum alloys, stainless steel, ductile iron, and other metal raw materials used for casting or machining actuator housings, cylinders, and key structural components; high-performance engineering plastics and special sealing materials, such as PTFE (polytetrafluoroethylene), FKM (fluororubber), and NBR (nitrile butadiene rubber), used to manufacture piston seals, O-rings, and valve stem seals, ensuring reliability and long service life under wide temperature ranges and harsh media; and precision spring steel, which is the core for achieving the “spring return” function, its fatigue life and force stability directly determining the actuator’s reliable operating frequency and fail-safe performance. In addition, the supply of high-precision sensors, solenoid valves, positioners, and other electro-pneumatic components also constitutes an important part of the upstream segment.

The midstream segment comprises the design, manufacturing, and integration of single-acting pneumatic actuators, which is the core of value creation.

Manufacturers utilize upstream raw materials and components, employing processes such as precision casting, CNC machining, and automated assembly to produce standardized actuator bodies. The core technologies in this process lie in the precise fit between the cylinder and piston, the accurate selection and preload of the spring, and the optimized design of the entire motion mechanism (such as gears, racks, and shift forks) to achieve the required output torque, speed, and reliability. Leading manufacturers not only produce hardware but also provide add-on modules such as intelligent positioners, limit switches, and manual operating mechanisms, and can offer non-standard customization based on customer needs (such as special sizes, explosion-proof ratings, and anti-corrosion coatings). The competitiveness of midstream companies is reflected in the completeness of their product lines, consistency of quality, delivery cycles, and cost control capabilities.

Downstream is the system integrator and end-application, responsible for transforming the actuator into a final solution.

System integrators and valve manufacturers play a key role here, assembling single-acting pneumatic actuators with valve bodies such as ball valves, butterfly valves, and plug valves to form pneumatic valves, which are then integrated into broader industrial automation control systems. These systems are widely used in end-user industries such as oil and gas, chemicals, power, water treatment, pharmaceuticals, and food and beverage. Single-acting actuators, due to their inherent safety feature of automatic reset upon gas failure (fault-on or fault-off), are the preferred choice for applications requiring safety interlocking or emergency shut-off. Downstream demand directly drives technological iteration in midstream products, with increasing demands for higher protection ratings (IP68), wider temperature adaptability (-40°C to +150°C), and digital interfaces (such as PROFIBUS and Modbus).

Throughout the entire industry chain is a robust horizontal support system. This includes stringent international standards and certifications, such as ISO 5211 installation standards, ATEX/IECEx explosion-proof certification, and SIL functional safety certification, which provide benchmarks for product interoperability and market access. Continuous R&D and innovation focus on improving energy efficiency, reducing friction, extending spring life, and developing integrated intelligent diagnostic functions. A comprehensive distribution network and technical services ensure rapid product delivery and provide end-users with installation, commissioning, maintenance training, and after-sales support, thus completing the final transformation from product to reliable productivity.

The competitive landscape of single-acting pneumatic actuators exhibits the following characteristics: From a segmented perspective, the single-acting pneumatic actuator market displays a clear tiered competitive structure. In the high-end market, competition is primarily concentrated among manufacturers with long-term technological accumulation and international engineering project experience. These companies possess significant advantages in product reliability, spring design life, corrosion and explosion-proof ratings, and international certification systems. Their products are mostly supplied to large-scale petrochemical, oil and gas pipeline, and multinational engineering projects, resulting in strong customer loyalty, high barriers to entry, and relatively stable prices and profit margins. The mid-range market is dominated by reliable, cost-effective standardized products, with the largest number of manufacturers. These primarily serve regional engineering projects and established industrial clients, with competition focusing on delivery time, customization capabilities, and after-sales service. The low-end market is dominated by general-purpose, low-specification products. Technological barriers are low, price competition is fierce, and product homogeneity is significant. Manufacturers primarily compete through large-scale production and cost control.

From a regional competition perspective, European and American companies maintain a strong influence in high-end applications and core technologies, while Asia-Pacific manufacturers hold a clear advantage in the low-to-mid-end market and supporting capabilities, and are continuously penetrating the mid-to-high-end market through cost, delivery, and localized services. Differences in material selection, design standards, and certification systems among manufacturers in different regions further intensify the stratified competition in the market.

Overall, the single-acting pneumatic actuator industry exhibits a pattern of “high-end concentration, mid-range dispersion, and intense competition in the low-end.” As safety standards become more stringent and engineering projects demand higher reliability, market demand is gradually shifting towards high-performance, high-certification-level products. Industry competition will shift from simple price competition to comprehensive competition based on technological reliability, application experience, and system solution capabilities. Companies with advantages in brand, certification, and engineering support are expected to continue to increase their market share.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Single-acting Pneumatic Actuator market is segmented as below:

By Company

MT Valves & Fittings

Uflow Automation

COVNA

EBRO ARMATUREN

Quifer Actuators, SL

Autorun Control Valve Co.,Ltd

JUHANG

Marsh Automation

Aira Euro Automation

FREYA

FLOWX

ZHONGZHI VALVE GROUP

ACTUATECH

SHANGHAI QUGONG VALVE PIPE ENGINEERING CO.,LTD

Huaershi

Kinetrol

VINCER

Segment by Type

Torque <100 Nm

Torque 100-2000 Nm

Torque >2000 Nm

Others

Segment by Application

Petroleum

Chemicals

Metallurgy

Water Treatment

Others

Each chapter of the report provides detailed information for readers to further understand the Single-acting Pneumatic Actuator market:

Chapter 1: Introduces the report scope of the Single-acting Pneumatic Actuator report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Single-acting Pneumatic Actuator manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Single-acting Pneumatic Actuator market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Single-acting Pneumatic Actuator in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Single-acting Pneumatic Actuator in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Single-acting Pneumatic Actuator competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Single-acting Pneumatic Actuator comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Single-acting Pneumatic Actuator market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Single-acting Pneumatic Actuator Market Research Report 2026

Global Single-acting Pneumatic Actuator Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Single-acting Pneumatic Actuator Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp