QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Lightning Strike Protection Film- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Lightning Strike Protection Film market, including market size, share, demand, industry development status, and forecasts for the next few years.

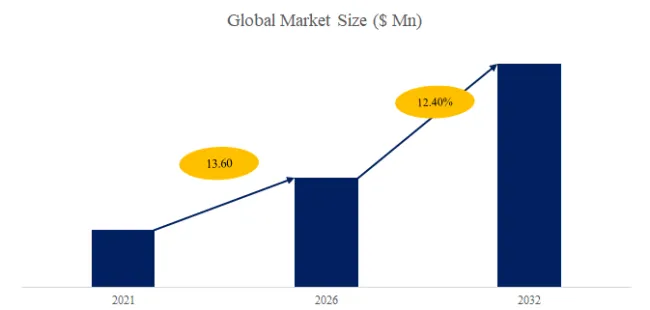

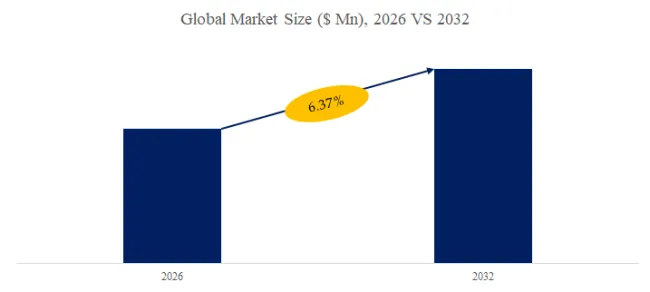

The global market for Lightning Strike Protection Film was estimated to be worth US$ 455 million in 2025 and is projected to reach US$ 696 million, growing at a CAGR of 6.4% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5775127/lightning-strike-protection-film

Lightning Strike Protection Film (LSPF) Market Summary

Lightning Strike Protection Film (LSPF) is a specialized material designed to protect surfaces, primarily in aerospace applications, from damage caused by lightning strikes. Aircraft, wind turbines, and other structures that operate in lightning-prone environments are particularly vulnerable to lightning-induced damage, which can compromise structural integrity and safety. LSPF is typically a lightweight, durable, and conductive film that is applied to external surfaces to dissipate the high energy of a lightning strike, minimizing thermal, electrical, and physical damage. Its use enhances safety, reduces maintenance costs, and prolongs the lifespan of protected equipment.

According to the new market research report “Global Lightning Strike Protection Film Market Report 2021-2032”, published by QYResearch, the global Lightning Strike Protection Film market size is projected to reach USD 0.7 billion by 2032, at a CAGR of 6.4% during the forecast period.

Figure00001. Global Lightning Strike Protection Film (LSPF) Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global Lightning Strike Protection Film (LSPF) Market Report 2021-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

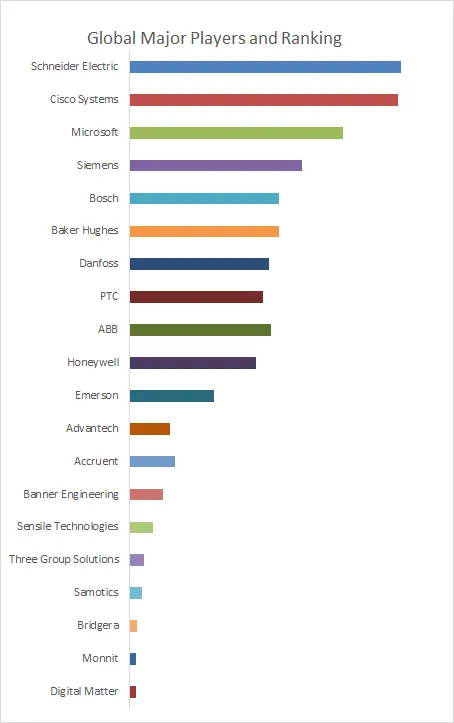

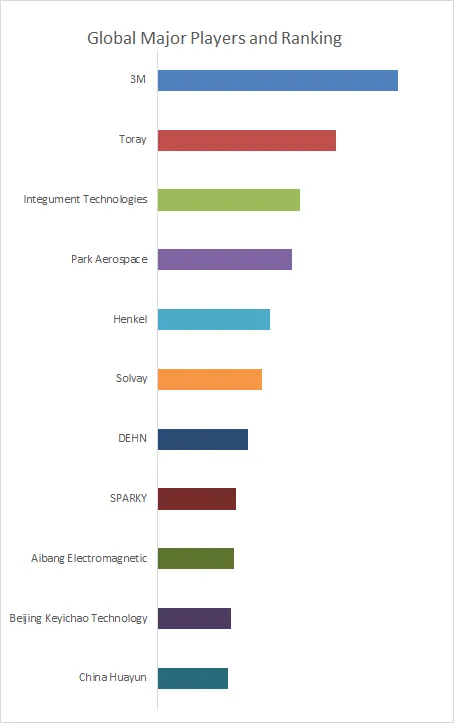

Figure00002. Global Lightning Strike Protection Film (LSPF) Top 11 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Lightning Strike Protection Film (LSPF) Market Report 2021-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

Table 1. Lightning Strike Protection Film (LSPF) Industry Chain Analysis

| Item | Description | |

| Upstream | Copper-plated steel | The copper-plated steel used in the lightning protection film is a composite metal material that uses electroplating/cladding technology to composite a highly conductive copper layer on the surface of a high-quality steel core. It is the core conductive structural substrate for the lightning protection film to achieve lightning current conduction and grounding dissipation, and unlike pure copper or pure steel materials, it combines the mechanical strength of steel with the high conductivity of copper. |

| Integrated intelligent monitoring module | The integrated intelligent monitoring module integrated into the lightning protection film is a miniature intelligent monitoring terminal that integrates a lightning strike sensor, data acquisition chip, wireless communication module, and low-power power supply unit. It is the core intelligent component for the lightning protection film to achieve lightning strike event monitoring, status warning, and data traceability, giving traditional lightning protection films digital and intelligent attributes. | |

| Varistor | The varistor (MOV) in the lightning protection film is a non-linear resistive semiconductor component with zinc oxide as the core raw material. It is the core protection component for the lightning protection film to achieve overvoltage clamping and surge suppression, connected in series/parallel in the copper-plated steel conductive circuit, and is a key device for lightning surge protection. | |

| Downstream | Power sector | The main applications include lightning protection films for high-voltage transmission lines, lightning protection films for power equipment enclosures, and surge protection films for power cabinets. They are divided into flexible, wrap-around types (suitable for lines and insulators) and rigid, adhesive types (suitable for equipment enclosures and cabinets), with some models integrating grounding terminals for direct connection to the power system grounding network. |

| Aerospace | The main applications include lightning protection films for spacecraft surfaces, lightning protection films for aircraft fuselage carbon fiber substrates, and lightning protection films for aerospace launch pads. All are customized flexible ultra-thin types that can be directly attached to aerospace-specific substrates such as carbon fiber, aluminum alloy, and composite materials, without increasing the weight and volume of the protected object. The main products include lightning protection films specifically designed for ancient building roofs/walls, lightning protection films for cultural relics, and lightning protection films for museum display cases. These are all flexible, matte films with customizable colors (to match the appearance of ancient buildings/cultural relics). They utilize a removable adhesive layer, supporting drill-free and weld-free adhesive installation. The copper-plated steel used features a customized low conductivity to prevent electrochemical corrosion. | |

| Building and cultural heritage protection | Other main products include lightning protection films for consumer electronics casings, surge protection films for household appliance interiors, and electrostatic discharge (ESD) protection films for portable electronic devices. These are all ultra-thin, flexible, and transparent films that can be directly applied to the casings or internal circuit boards of mobile phones, computers, home appliances, and smart home devices. Their small size and light weight are compatible with the miniaturized design of consumer electronic devices. | |

| Consumer electronics | The copper-plated steel used in the lightning protection film is a composite metal material that uses electroplating/cladding technology to composite a highly conductive copper layer on the surface of a high-quality steel core. It is the core conductive structural substrate for the lightning protection film to achieve lightning current conduction and grounding dissipation, and unlike pure copper or pure steel materials, it combines the mechanical strength of steel with the high conductivity of copper. |

Source: Secondary Sources, Press Releases, Expert Interviews and QYResearch, 2025

Table 2. Lightning Strike Protection Film (LSPF) Industry Policy Analysis

| Policy | Description | |

| 1 | The Meteorological Law of the People’s Republic of China and the Regulations on Meteorological Disaster Prevention and Mitigation | Buildings and facilities must be equipped with lightning protection devices that meet national standards and are subject to a regular inspection system. For example, flammable and explosive locations are inspected twice a year, while other locations are inspected once a year. |

| 2 | Measures for the Management of Lightning Protection and Disaster Reduction | It is further clarified that lightning protection devices for new, renovated, and expanded projects must be designed, constructed, and put into use simultaneously with the main project, and the lightning protection design review and completion acceptance are the responsibility of the meteorological authority. |

| 3 | Outline for High-Quality Development of Meteorology (2022-2035) | The improvement of the lightning protection safety standard system is being promoted. The demand for customized lightning protection and grounding systems is increasing in the new energy sector (such as photovoltaic power plants and wind power projects), and emerging fields such as smart grids and high-speed railways are becoming important application areas. |

Source: Secondary Sources, Press Releases, Expert Interviews and QYResearch, 2025

Table 3. Lightning Strike Protection Film (LSPF) Industry Development Trends

| Development Trends | Description | |

| 1 | Improvement of the national standard system and alignment with international standards | In April 2025, the National Technical Committee for Standardization of Lightning Protection released five national standards (GB/T 33588.1-6), covering the requirements for lightning protection system components such as connectors, isolation discharge gaps, and conductor fasteners, which are equivalent to the IEC 62561 international standard. At the same time, the GB/T 21714 series of standards clarifies the classification of lightning protection levels (LPL) and design standards for lightning current parameters, such as a peak current of 200kA and a rolling sphere radius of 60m for LPL I, providing quantitative basis for the design of lightning protection systems and promoting the alignment of industry technical specifications with global standards. |

| 2 | Strict market access and qualification control | The “Negative List for Market Access (2025 Edition)” includes “design review of lightning protection devices” and “qualification certification of lightning protection device testing units” in the negative list. Construction projects in the building and civil engineering sectors are prohibited without permission from the meteorological bureau. Lightning protection testing qualifications are divided into two levels: Class A can test all types of buildings and structures, while Class B is limited to the third category, ensuring the professionalism and authority of testing institutions and regulating market order. |

| 3 | Mandatory installation and regular inspection system | According to the “Meteorological Law” and “Regulations on Meteorological Disaster Prevention,” buildings and facilities must be equipped with lightning protection devices that meet national standards and are designed, constructed, and put into use simultaneously with the main project. Explosion/fire hazardous locations should be inspected every six months, while other locations should be inspected annually. The testing agency must possess CMA/CNAS accreditation, and the test reports must be internationally recognized to ensure the continued effectiveness of the lightning protection facilities. |

Source: Secondary Sources, Press Releases, Expert Interviews and QYResearch, 2025

About The Authors

|

Zhang Hao – Main Analyst of this Article |

| zhanghao@qyresearch.com | |

| Mr. Zhang has many years of experience in industry analysis and has long focused on related industry research in the field of materials science and engineering. |

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Lightning Strike Protection Film market is segmented as below:

By Company

3M

Toray

Integument Technologies

Park Aerospace

Henkel

Solvay

DEHN

SPARKY

Aibang Electromagnetic

Beijing Keyichao Technology

China Huayun

Segment by Type

Self-adhesive film

Non-self-adhesive film

Segment by Application

Electronic Equipment

Aerospace

Architecture & Heritage

Other

Each chapter of the report provides detailed information for readers to further understand the Lightning Strike Protection Film market:

Chapter 1: Introduces the report scope of the Lightning Strike Protection Film report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Lightning Strike Protection Film manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Lightning Strike Protection Film market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Lightning Strike Protection Film in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Lightning Strike Protection Film in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Lightning Strike Protection Film competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Lightning Strike Protection Film comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Lightning Strike Protection Film market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Lightning Strike Protection Film Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Lightning Strike Protection Film Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Lightning Strike Protection Film Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp