QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Flame-Retardant EV Battery Case Material- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Flame-Retardant EV Battery Case Material market, including market size, share, demand, industry development status, and forecasts for the next few years.

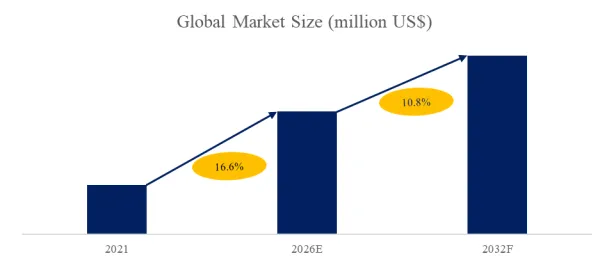

The global market for Flame-Retardant EV Battery Case Material was estimated to be worth US$ 46.95 million in 2025 and is projected to reach US$ 91.61 million, growing at a CAGR of 10.8% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5990220/flame-retardant-ev-battery-case-material

EV Battery Case Material Market Summary

Flame-Retardant EV Battery Case Material refers to non-metal material systems used in electric vehicle designed to delay ignition and slow flame development under extreme thermal conditions. A key advantage of these materials is their ability to extend the time to ignition and reduce the rate of flame propagation during thermal runaway or external fire exposure. By slowing the onset and spread of combustion, flame-retardant battery case materials provide additional response time for thermal management systems, safety interventions, and occupant evacuation.

According to the new market research report “Global EV Battery Case Material Market Report 2026-2032”, published by QYResearch, the global EV Battery Case Material market size is projected to reach USD 0.09 billion by 2032, at a CAGR of 10.8% during the forecast period.

Figure00001. Global EV Battery Case Material Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global EV Battery Case Material Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

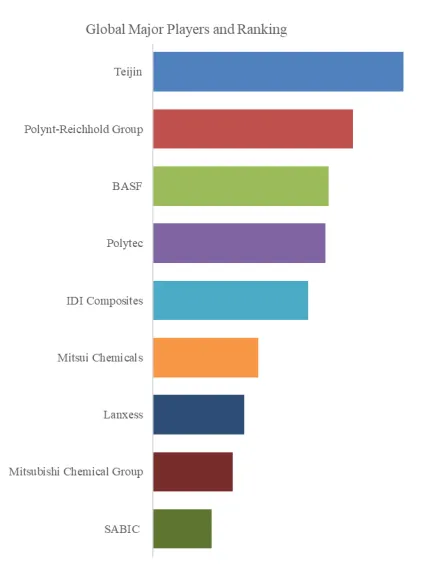

Figure00002. Global EV Battery Case Material Top 9 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global EV Battery Case Material Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

According to QYResearch Top Players Research Center, the global key manufacturers of EV Battery Case Material include Teijin, Polynt-Reichhold Group, BASF, etc. In 2025, the global top three players had a share approximately 36.14% in terms of revenue.

Industrial Chain

The upstream of flame-retardant EV battery case materials is centered on resin systems, fillers, and reinforcing fibers. The core matrix materials include thermosetting resins such as unsaturated polyester resins and vinyl ester resins, supplied by AOC, INEOS Composites, Ashland, and Eternal Materials, which provide crosslinking performance and thermal stability during compression molding. Fillers including calcium carbonate, aluminum trihydrate, glass microspheres, and clay are critical for cost control and flame-retardant efficiency, with key suppliers such as Huber Engineered Materials, Chalco, Nabaltec AG, and Hindalco Industries. Reinforcing fibers, mainly glass fiber and carbon fiber, determine mechanical strength and rigidity, with major suppliers including China Jushi, Owens Corning, Taishan Fiberglass, CPIC, and Johns Manville.

The midstream focuses on formulation design, compounding, and molding processes that convert raw materials into flame-retardant battery case components. Key activities include resin–filler ratio optimization, fiber dispersion control, flame-retardant system balancing, and rheological tuning to ensure stable compression molding or thermoplastic forming. Manufacturers in this stage integrate mechanical strength, thermal resistance, flame retardancy, and dimensional stability into a single material system, while also meeting automotive requirements for lightweighting, consistency, and mass-production efficiency.

Downstream applications of flame-retardant EV battery case materials are primarily concentrated in battery enclosure and battery cover. These materials are adopted by leading automotive OEMs including Volkswagen Group, General Motors, Hyundai Motor Group, and Toyota, where high flame resistance, structural integrity, and crash safety are mandatory.

Influencing Factors

Drivers:

The continuous growth of global EV production is a fundamental driver for flame-retardant EV battery case materials. As EV output increases year by year, the total number of battery packs installed in vehicles rises accordingly, which directly enlarges the addressable base for battery safety–related materials. Even if the penetration rate of flame-retardant battery case materials remains relatively low, higher vehicle volumes translate into growing absolute demand. In addition, higher production volumes increase the exposure of OEMs to large-scale quality and safety risks. A single safety incident can affect a much larger vehicle population, amplifying potential recall costs and reputational damage. This scale effect encourages manufacturers to reassess safety margins at the material level, including the role of flame-retardant materials in battery cases.

Regulatory attention to EV battery safety is intensifying, providing a strong policy-driven driver for flame-retardant battery case materials. Governments and regulatory bodies are updating safety standards to address fire exposure, thermal runaway behavior, and post-incident containment. While regulations may not mandate specific materials, they raise performance expectations for battery systems as a whole. This indirectly increases scrutiny on battery case materials and encourages OEMs to adopt solutions that improve compliance margins. As regulatory requirements evolve, material choices are increasingly influenced by their ability to support certification and reduce approval risk. For manufacturers, selecting materials with proven flame-retardant behavior can simplify regulatory discussions and reduce uncertainty during homologation. Over time, tighter safety frameworks reinforce demand for materials that contribute to meeting or exceeding regulatory expectations at the system level.

Challenges:

The first challenge is the strong structural inertia of metal battery cases in the EV industry. Metal enclosures benefit from long-standing validation history, well-established supply chains, and deep integration into vehicle architectures. For many OEMs, metal battery cases are considered a proven baseline with predictable performance and low engineering risk. As a result, flame-retardant non-metal materials face limited opportunities for substitution, particularly on existing platforms. Even when alternative materials demonstrate technical feasibility, changing the battery case material often requires redesign of interfaces, mounting concepts, and validation pathways. This inertia slows adoption and confines demand mainly to new platform launches rather than mid-cycle upgrades. Consequently, market growth for flame-retardant battery case materials is constrained not by lack of interest, but by the difficulty of displacing entrenched metal solutions.

Another challenge lies in the demanding qualification and validation process for battery case materials. Flame-retardant materials must demonstrate stable performance across large parts, long service life, and extreme thermal conditions. Testing requirements are time-consuming and costly, often requiring part-level and vehicle-level validation. These barriers favor established suppliers with proven track records and make entry difficult for new participants. For OEMs, switching materials also involves redesign, tooling changes, and new validation programs, further slowing decision-making. This limits the speed at which new flame-retardant materials can enter production.

Trend:

Across new-generation EV platforms, flame-retardant battery case materials are increasingly being considered during early platform planning, rather than being excluded by default. Historically, battery cases were assumed to be metallic, and non-metal options were rarely evaluated beyond concept studies. This situation is changing as safety discussions around thermal runaway, external fire exposure, and containment time become more prominent at the platform level. As a result, material shortlists are expanding to include flame-retardant composites and engineered plastics for battery case applications.

Development is increasingly centered on mass-production readiness for battery case parts. Material projects are now more often tied to real tooling, real cycle-time targets, and stable quality at large part sizes. For thermoset SMC, this means improving molding stability and reducing defect sensitivity on large covers and trays. For flame-retardant thermoplastics, the focus is on making large parts consistently, improving repeatability, and ensuring assembly and sealing can be delivered with stable yield. In practice, the industry is moving from “material capability discussions” to “production feasibility proof,” because platform decisions require predictable supply, consistent dimensions, and controllable scrap rates. This trend matters because once a material system proves it can be manufactured reliably at scale, it becomes much easier to replicate across platform variants and to convince OEMs to commit to program-level adoption.

About The Authors

Lead Author: Julie Zhang

Email: zhangjianan@qyresearch.com

Julie Zhang, a key industry analyst a industry analyst of QYResearch (Beijing Hengzhou Bozhi International Information Consulting Co.,Ltd.), focuses on market research and trend forecasting of the entire industry chain upstream and downstream of the electric vehicle and lithium battery industry, we are good at providing strategic market insights through in-depth data mining, focusing on trends and technological innovations in the automotive and lithium battery industry, and helping the company achieve sustainable success in the highly competitive market environment. Typical studies include Electronic Fusing IC, EV Skateboard Platform, Electric Vehicle Controller, Automotive Interior Monitoring System, Automotive PCIe Switch Chips, End-To-End Automotive Software Platform, LiFSI Electrolyte Salts, Portable Power Supply, Outdoor Mobile Powers, and Solar Energy Storage Battery, etc.

About QYResearch

QYResearch founded in California, USA in 2007. It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Flame-Retardant EV Battery Case Material market is segmented as below:

By Company

Mitsubishi Chemical Group

Teijin

Polytec

SABIC

BASF

Mitsui Chemicals

IDI Composites

Polynt-Reichhold Group

Lanxess

Segment by Type

Sheet Molding Compound

Thermoplastics

Others

Segment by Application

Enclosure

Cover

Others

Each chapter of the report provides detailed information for readers to further understand the Flame-Retardant EV Battery Case Material market:

Chapter 1: Introduces the report scope of the Flame-Retardant EV Battery Case Material report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Flame-Retardant EV Battery Case Material manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Flame-Retardant EV Battery Case Material market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Flame-Retardant EV Battery Case Material in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Flame-Retardant EV Battery Case Material in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Flame-Retardant EV Battery Case Material competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Flame-Retardant EV Battery Case Material comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Flame-Retardant EV Battery Case Material market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Flame-Retardant EV Battery Case Material Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Flame-Retardant EV Battery Case Material Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Flame-Retardant EV Battery Case Material Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp