Global Leading Market Research Publisher QYResearch announces the release of its latest report “Automotive Dead Reckoning (ADR) Module – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Automotive Dead Reckoning (ADR) Module market, including market size, share, demand, industry development status, and forecasts for the next few years.

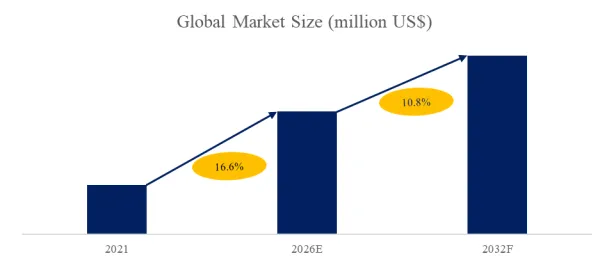

For automakers, navigation system developers, and drivers alike, the frustration of losing GPS signal in tunnels, parking garages, and urban canyons represents a persistent usability gap in modern vehicle navigation. More critically, for advanced driver assistance systems (ADAS) and autonomous driving platforms, any interruption in positioning data creates safety risks and operational limitations. Automotive Dead Reckoning (ADR) modules address this challenge by combining Global Navigation Satellite System (GNSS) data with information from the vehicle’s own sensors—including wheel speed sensors (wheel ticks) and gyroscopes—to continuously estimate vehicle location and speed, even when satellite signals are unavailable. Through sophisticated sensor fusion algorithms, often employing Kalman filters, ADR modules deliver uninterrupted, precise navigation in tunnels, underpasses, and other challenging environments. The global market for ADR modules was valued at US$ 302 million in 2025 and is projected to grow at a CAGR of 5.3% to reach US$ 431 million by 2032, driven by the increasing demand for seamless navigation experiences, the expansion of ADAS and autonomous driving features, and the migration of ADR technology from high-end vehicles to mainstream models. In 2024, global production reached approximately 624,000 units, with an average market price of US$ 462 per unit.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6098641/automotive-dead-reckoning–adr–module

Market Definition and Product Segmentation

Automotive Dead Reckoning modules represent a specialized category within the vehicle positioning and navigation ecosystem, distinguished by their integration of GNSS data with vehicle internal sensors. Unlike consumer-grade navigation devices that rely solely on satellite signals, ADR modules leverage the vehicle’s existing sensor infrastructure to maintain positioning continuity.

Product Type Segmentation

The market is stratified by dimensionality of positioning capability:

- 3D ADR Module: The premium segment, providing three-dimensional positioning including altitude and elevation data. 3D modules incorporate gyroscopes and accelerometers to track vehicle movement across all axes, enabling accurate positioning in multi-level parking structures, complex highway interchanges, and hilly terrain. This segment is increasingly specified for autonomous vehicles and premium navigation systems.

- 2D ADR Module: The established volume segment, providing two-dimensional positioning (latitude and longitude) using wheel speed sensors and yaw rate data. 2D modules offer cost-effective solutions for mainstream navigation applications where elevation tracking is less critical.

Application Segmentation

The market serves distinct channels with varying requirements:

- OEM (Original Equipment Manufacturer): The dominant and higher-growth segment, representing factory-installed ADR modules integrated into new vehicles. OEM adoption is driven by automakers’ need to deliver seamless navigation experiences and enable ADAS features that require continuous positioning.

- Aftermarket: Serving vehicle retrofits and aftermarket navigation systems, offering growth opportunities as consumers seek to upgrade existing vehicles with enhanced positioning capabilities.

Industry Value Chain and Competitive Landscape

Upstream Supply Chain

The ADR module industry relies on specialized upstream components:

- Inertial Sensors: Gyroscopes and accelerometers from manufacturers including Honeywell, Analog Devices, and Northrop Grumman provide the motion sensing essential for dead reckoning

- Wheel Speed Sensors: Vehicle-integrated sensors that provide wheel tick data critical for distance and velocity estimation

- GNSS Chips: Multi-constellation satellite receivers providing baseline positioning data

- Sensor Fusion Software: Kalman filters and advanced algorithms that combine disparate sensor inputs into continuous positioning solutions

Downstream Applications

ADR modules are ultimately deployed in in-vehicle navigation systems and smart cockpits, delivering seamless navigation experiences that resolve the common user pain point of “losing navigation signals in tunnels.” While initially featured in high-end vehicles, ADR technology is progressively migrating to mainstream models as consumer expectations for uninterrupted navigation expand. Autonomous driving systems represent the most demanding application, requiring continuous, high-precision positioning for safe operation.

Competitive Landscape

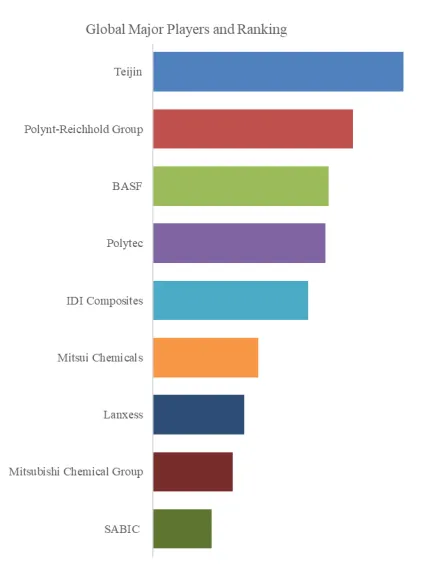

The ADR module market features a concentrated competitive landscape dominated by specialized positioning and semiconductor companies. Key players include u-blox, Locosys, STMicroelectronics, Telit Cinterion, SkyTraq, Allystar Technology, Cisco, and Quectel.

Industry Development Characteristics

1. Consumer Navigation Experience Driving Adoption

A case study from QYResearch’s industry monitoring reveals that consumer frustration with navigation signal loss in tunnels and parking structures has become a significant driver of ADR adoption. Automakers increasingly position seamless navigation—maintaining positioning through all driving environments—as a competitive differentiator, particularly in premium and mid-range vehicle segments.

2. ADAS and Autonomous Driving Requirements

Advanced driver assistance systems and autonomous driving platforms impose the most stringent requirements on positioning continuity. A case study from the autonomous vehicle sector indicates that Level 2+ and Level 3 systems require uninterrupted positioning for safe operation of lane-keeping, adaptive cruise control, and automated lane-change functions. ADR modules provide the essential bridging capability when GNSS signals are temporarily unavailable.

3. Migration from High-End to Mainstream Vehicles

The technology migration pattern observed in many automotive electronics—initially debuting in premium vehicles before cascading to mainstream segments—is evident in ADR adoption. Over the past 18 months, mid-range vehicle platforms have increasingly incorporated ADR modules as standard equipment, expanding the addressable market significantly.

4. Sensor Fusion Algorithm Advancement

Recent advances in Kalman filter implementations and AI-enhanced sensor fusion have improved ADR accuracy while reducing computational requirements. Modern systems leverage machine learning to recognize environmental patterns and predict positioning errors, enabling more robust performance in challenging urban environments.

Exclusive Industry Insights: The Smart Cockpit Integration Opportunity

Our proprietary analysis identifies the smart cockpit as a key growth frontier for ADR modules. As vehicle interiors evolve into integrated digital environments, navigation positioning serves as foundational data for a range of features—from augmented reality head-up displays to predictive energy management in electric vehicles. ADR modules that deliver continuous, high-accuracy positioning enable these advanced applications, creating value beyond basic navigation functionality.

Strategic Outlook

For industry executives, investors, and marketing leaders evaluating opportunities in the Automotive Dead Reckoning module market, the projected 5.3% CAGR reflects sustained demand from consumer expectations for seamless navigation, ADAS expansion, and the migration of ADR technology to mainstream vehicle segments. Manufacturers positioned to capture disproportionate share share three characteristics: demonstrated expertise in sensor fusion algorithms; established relationships with automotive OEMs; and proven reliability in automotive-grade applications. As the market evolves toward higher levels of autonomy and more sophisticated smart cockpit experiences, the ability to deliver cost-effective, high-accuracy ADR solutions meeting automotive safety standards will define competitive leadership.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp