QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Hydrophilic Intermittent Urinary Catheter- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Hydrophilic Intermittent Urinary Catheter market, including market size, share, demand, industry development status, and forecasts for the next few years.

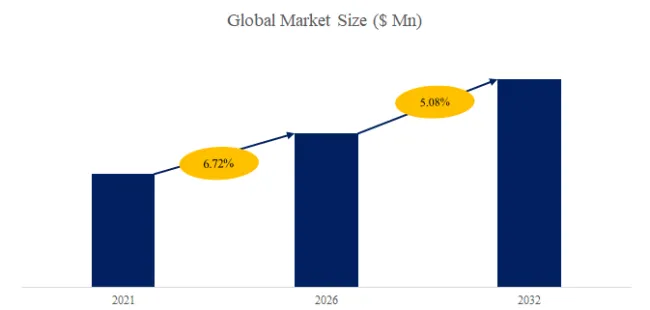

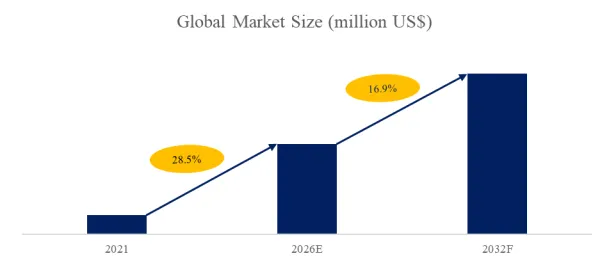

The global market for Hydrophilic Intermittent Urinary Catheter was estimated to be worth US$ 5760 million in 2025 and is projected to reach US$ 11809 million, growing at a CAGR of 10.8% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5990275/hydrophilic-intermittent-urinary-catheter

Hydrophilic Intermittent Urinary Catheter Market Summary

According to the latest report “Global Hydrophilic Intermittent Urinary Catheter Market Report 2025-2031″ by the QYResearch research team, the global Hydrophilic Intermittent Urinary Catheter market size is expected to reach US$11.8 billion in 2031, with a compound annual growth rate (CAGR) of 10.8% in the next few years.

The hydrophilic intermittent urinary catheter is a medical device specifically designed for patients requiring intermittent catheterization. Its surface is treated with a special hydrophilic coating, allowing for rapid lubrication upon contact with urine or aqueous solutions, significantly reducing friction and irritation to the urethral mucosa during insertion and removal. Typically made of soft polyurethane or silicone, this catheter possesses excellent flexibility and shape memory, adapting to different urethral anatomy structures while minimizing urethral injury, infection risk, and discomfort. The hydrophilic intermittent urinary catheter is suitable for individuals requiring intermittent catheterization, including those with neurogenic bladder, those recovering from urological surgery, elderly patients, and long-term bedridden patients. It can be used single-use or multiple-use (disposable or reusable models) and is widely used in hospitals, rehabilitation centers, and home care settings. It is a safe, convenient, and highly patient-compliant auxiliary device in modern urological care.

Hydrophilic intermittent urinary catheters, as an advanced disposable urological care device, have experienced significant growth in both the global and Chinese markets in recent years. The core market driver stems from increasing clinical demand, particularly for the long-term management of patients with neurogenic bladder dysfunction (such as those with spinal cord injury or multiple sclerosis), and the treatment of temporary urinary difficulties such as benign prostatic hyperplasia and postoperative urinary retention. Compared to traditional non-hydrophilic catheters, the hydrophilic coating technology forms a smooth surface upon contact with water, significantly reducing friction damage and the risk of infection during insertion, thus significantly improving patient comfort and safety. This significant clinical advantage has made it the standard recommended product in the field of intermittent catheterization.

Globally, this market is dominated by several international medical device giants. Technological iterations focus on coating improvements (such as reducing allergic reactions and enhancing lubrication durability), integrated packaging design (such as pre-lubrication and sterile individual packaging), and improved ease of use. Domestic products are gradually expanding their market share due to their cost-effectiveness, but they still lag behind leading international brands in high-end coating technology and brand trust.

Future market development is expected to focus on product differentiation and accessibility. Technological innovation directions include the integration of antimicrobial coatings, the application of biodegradable materials, and the development of intelligent connectivity devices (for monitoring urination data). Furthermore, with the increasing prevalence of home care models and enhanced patient self-management awareness, the expansion of the consumer market and the deepening of education and training will be key growth drivers. Overall, the hydrophilic intermittent catheter market is at a crucial stage of evolution from specialized medical products to broader, more humanized health management solutions, and its market size and penetration rate are expected to continue to increase.

The main drivers influencing the development of Hydrophilic intermittent urinary catheters are demographic changes and growing healthcare needs. With the accelerating global aging population and the rising number of patients with prolonged bed rest and neurogenic bladder, the demand for safe, comfortable intermittent catheters that reduce urethral injury continues to increase. In addition, the increase in urological surgeries and the widespread adoption of home care are also driving patients’ and care institutions’ reliance on high-performance catheters, thus becoming an important external driver of market expansion.

The improvement of regulations and clinical standards is also a key driver. Stringent safety, biocompatibility, and sterility requirements for disposable medical devices in various countries have prompted manufacturers to optimize material properties, coating processes, and product specifications to meet clinical safety and compliance requirements. This has not only improved product quality but also raised market entry barriers, thereby driving technological iteration and innovation.

Technological advancements also play a crucial role in industry development. The maturity of hydrophilic coating materials, flexible polymer substrates, and low-friction surface treatment technologies has continuously improved the lubricity, flexibility, durability, and patient comfort of urinary catheters. Furthermore, these advancements can be combined with smart nursing or disposable recyclable designs to reduce infection risks and care costs, expanding applications in hospital and home care scenarios.

In addition, increased patient health awareness and the trend towards digitalized care are also driving market development. Patients’ and caregivers’ focus on reducing urinary tract infections, improving ease of operation, and enhancing compliance has made hydrophilic intermittent urinary catheters more popular in clinical and home use, creating long-term, stable market demand and providing a continuous driving force for product upgrades and industry expansion.

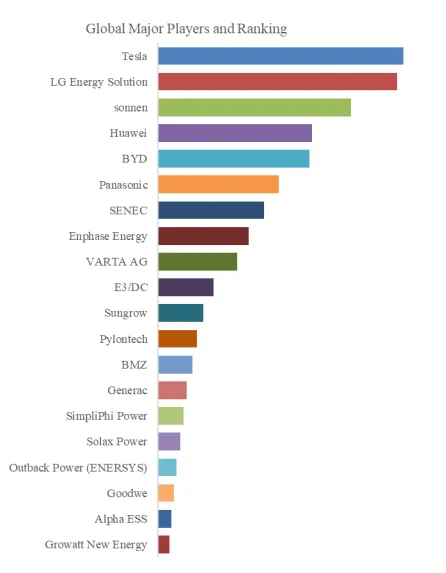

This report profiles key players of Hydrophilic Intermittent Urinary Catheter such as Becton Dickinson、Convatec、Wellspect、Hollister Incorporated、Teleflex、Well Lead Medical Co.,Ltd.、Coloplast、Boen Healthcare Co.,Ltd、Bevermedical、AdvaCare Pharma、GCMEDICA、Bonree Medical Co., Ltd、Manfred Sauer GMBH、Otsuka Pharmaceutical Factory, Inc.、Daxan

The hydrophilic intermittent urinary catheter industry chain is a complete system from basic materials to end-clinical applications. Its core lies in combining polymer materials science with precision medical device manufacturing, ultimately serving patients and medical institutions. Each link in the industry chain is closely interconnected, jointly determining the product’s performance, cost, and market competitiveness.

Upstream: Raw material and core technology supply.

This is the technological starting point and value foundation of the industry chain. It mainly includes:

Polymer materials: such as medical-grade polyvinyl chloride (PVC), silicone, latex, etc., used to manufacture the catheter body. In recent years, the softer silicone material has increasingly become the preferred choice for high-end products due to its higher biocompatibility.

Hydrophilic coating materials: This is where the core technology lies, typically high-molecular polymers such as polyvinylpyrrolidone (PVP). The coating formulation and process (such as covalent bonding or physical adsorption) directly determine lubricity, durability, and biocompatibility.

Other components and packaging materials: including connectors, urine drainage bags, sterile water for injection packs (used to activate the hydrophilic coating), and sterile barrier packaging systems that meet medical device standards.

Upstream suppliers’ R&D capabilities and quality control are key to product differentiation, especially patented coating technologies, which are the core of international giants’ competitive barriers.

Midstream: R&D, Production, and Assembly

This is the core link in transforming raw materials into the final product, led by medical device manufacturers. The process includes:

Catheter Extrusion and Molding: Polymer materials are extruded into catheters using precision extrusion processes.

Hydrophilic Coating: In a cleanroom, hydrophilic polymers are uniformly coated onto the catheter surface using processes such as impregnation and spraying, followed by curing. This step requires extremely high stability and consistency in the process.

Assembly and Sterilization: The catheter and connectors are assembled and sealed in the final packaging along with activation water. Sterilization is then performed using ethylene oxide or irradiation to ensure the product’s sterility.

Quality Control and Registration: Rigorous quality control throughout the entire process, necessitating completion of medical device registration application with the National Medical Products Administration (NMPA) and obtaining a registration certificate before the product can be marketed. This stage involves the highest levels of technology, capital, and regulatory hurdles.

Downstream: Distribution, End-User Use, and Service

The value realization links in the industry chain connect products and end users:

Distribution channels: These include medical device distributors and agents at all levels, as well as increasingly important e-commerce platforms (B2B and B2C). The breadth and efficiency of channel coverage directly affect product accessibility.

End users:

Medical institutions: Hospitals (urology, rehabilitation, neurology, operating rooms, etc.) are the main purchasers and users; their clinical recognition and recommendations are crucial.

Individual patients: Purchased through prescriptions at pharmacies or online for long-term home-based intermittent catheterization. Patient education, usage guidance, and affordability are key factors influencing consumption.

Payers and support systems: Medical insurance reimbursement policies (coverage and reimbursement rates) are one of the core factors affecting market penetration. In addition, professional training for nurses and rehabilitation therapists, as well as patient education services provided by companies, together constitute a support network promoting correct product use and market expansion.

In summary, the hydrophilic intermittent catheter industry chain exhibits typical characteristics of “high-tech driven and strongly regulated.” Upstream material innovation and midstream precision manufacturing are fundamental to product competitiveness, while downstream payment policies and patient services are key levers for market expansion. The synergistic efficiency of the entire chain is driving products towards greater safety, comfort, and convenience.

The competitive landscape of hydrophilic intermittent urinary catheters exhibits a clear hierarchical and dynamic evolution, which can be analyzed from the following perspectives:

Multinational giants dominate the high-end market. Leveraging their deep R&D accumulation, global brand influence, mature hydrophilic coating patent technology, and complete product lines, they have long held a dominant position in the global and Chinese high-end markets. Their products are renowned for their superior lubricity, safety, and user experience, and are relatively expensive, making them the preferred choice for many large hospitals and senior clinical experts.

Leading domestic companies are rapidly emerging. Through continuous technology introduction and independent R&D, they have achieved product quality approaching international standards. With significant cost-effectiveness advantages, flexible sales strategies, and deep penetration of local channels, they have secured a solid share in the mid-range market and are continuously challenging the high-end market, becoming a significant driver of growth in the domestic market.

Numerous regional companies are also competing. Many small and medium-sized medical device manufacturers primarily focus on the low-end market. Their products are mostly imitations, with differences in coating technology and stability, but they maintain a certain survival space in primary healthcare institutions and price-sensitive markets due to their low prices. This segment is highly competitive with low market concentration.

Potential entrants and innovators: Besides traditional manufacturers, some biotechnology companies specializing in new materials and processes are attempting breakthroughs at the source of coating technology. Simultaneously, internet healthcare platforms and new distributors are exploring value chain extensions from sales to patient management by integrating products and services, potentially changing the future competitive landscape.

In summary, the current hydrophilic intermittent urinary catheter market has formed an overall pattern of “foreign companies leading in technology and brands, while domestic companies dominate in scale penetration.” The core of competition is shifting from simple product price and channel competition to in-depth competition in coating technology innovation, material upgrades, product differentiation design, and integrated solutions combining professional services. In the future, with the advancement of medical insurance cost control policies such as volume-based procurement, companies with core technologies, cost control capabilities, and complete service ecosystems will further consolidate their advantages, market concentration is expected to continue to increase, and competition will become more of a contest of comprehensive strength.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Hydrophilic Intermittent Urinary Catheter market is segmented as below:

By Company

Becton Dickinson

Convatec

Wellspect

Hollister Incorporated

Teleflex

Well Lead Medical Co.,Ltd.

Coloplast

Boen Healthcare Co., Ltd

Bevermedical

AdvaCare Pharma

GCMEDICA

Bonree Medical Co., Ltd

Manfred Sauer GMBH

Otsuka Pharmaceutical Factory, Inc.

Daxan

Segment by Type

Ready-to-use

Water-activated Type

Segment by Application

Neurogenic Bladder

Postoperative/Acute Urinary Retention

Others

Each chapter of the report provides detailed information for readers to further understand the Hydrophilic Intermittent Urinary Catheter market:

Chapter 1: Introduces the report scope of the Hydrophilic Intermittent Urinary Catheter report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Hydrophilic Intermittent Urinary Catheter manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Hydrophilic Intermittent Urinary Catheter market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Hydrophilic Intermittent Urinary Catheter in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Hydrophilic Intermittent Urinary Catheter in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Hydrophilic Intermittent Urinary Catheter competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Hydrophilic Intermittent Urinary Catheter comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Hydrophilic Intermittent Urinary Catheter market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Hydrophilic Intermittent Urinary Catheter Market Research Report 2026

Global Hydrophilic Intermittent Urinary Catheter Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Hydrophilic Intermittent Urinary Catheter Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp