QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “AI-powered CSRD Reporting Software- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global AI-powered CSRD Reporting Software market, including market size, share, demand, industry development status, and forecasts for the next few years.

The global market for AI-powered CSRD Reporting Software was estimated to be worth US$ 1869 million in 2024 and is forecast to a readjusted size of US$ 4972 million by 2031 with a CAGR of 15.0% during the forecast period 2025-2031.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/4940384/ai-powered-csrd-reporting-software

AI-powered CSRD Reporting Software Market Summary

AI-powered CSRD Reporting Software is an advanced reporting tool that integrates artificial intelligence technology to automatically extract and analyze critical ESG data from businesses, swiftly generating compliant reports that meet CSRD standards through intelligent algorithms. Its essence lies in its capability to monitor and evaluate a company’s environmental, social, and governance performance in real-time, autonomously identify and alert to potential compliance risks, while also providing deep data insights to assist businesses in formulating and optimizing their ESG strategies. By automating processes and conducting precise data analysis, it significantly enhances the efficiency and accuracy of reporting, offering robust support for enterprises in achieving their sustainable development goals.

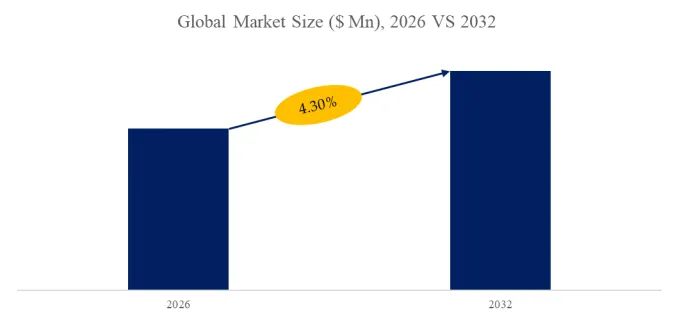

According to the new market research report “Global AI-powered CSRD Reporting Software Market Report 2026-2032”, published by QYResearch, the global AI-powered CSRD Reporting Software market size is projected to reach USD 1.43 billion by 2032, at a CAGR of 26.0% during the forecast period.

Figure00001. Global AI-powered CSRD Reporting Software Market Size (US$ Million), 2026-2032

Above data is based on report from QYResearch: Global AI-powered CSRD Reporting Software Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

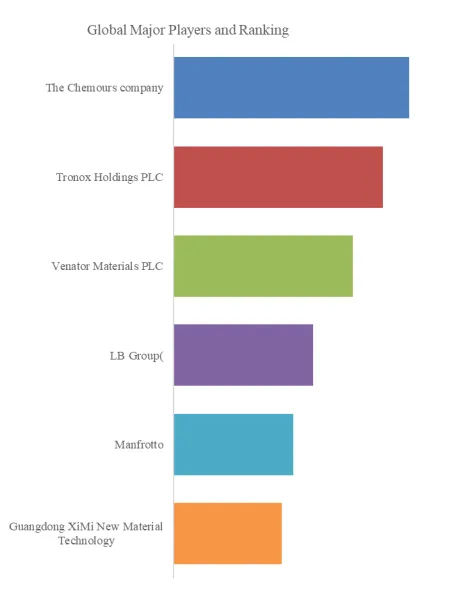

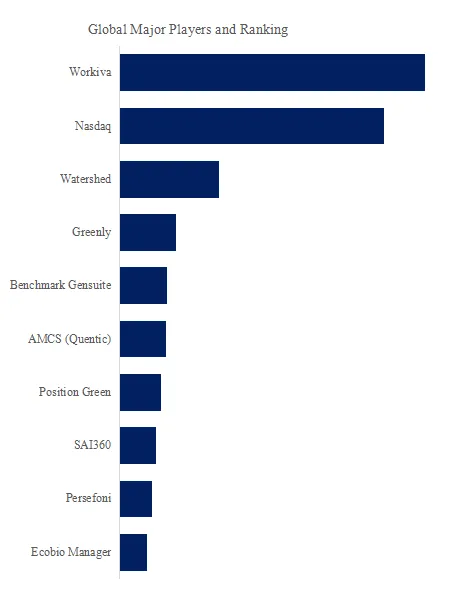

Figure00002. Global AI-powered CSRD Reporting Software Top 10 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global AI-powered CSRD Reporting Software Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

According to QYResearch Top Players Research Center, the global key manufacturers of AI-powered CSRD Reporting Software include Workiva, Nasdaq, Watershed, Greenly, Benchmark Gensuite, AMCS (Quentic), Position Green, SAI360, Persefoni, Ecobio Manager, etc. In 2025, the global top five players had a share approximately 48.0% in terms of revenue.

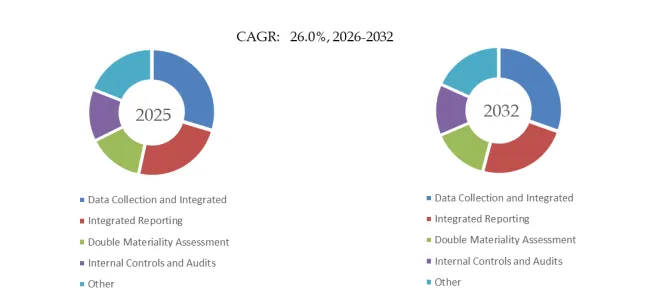

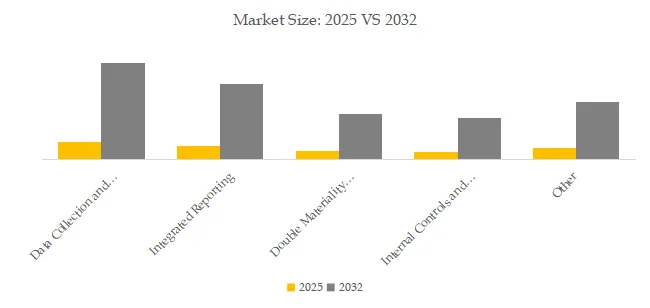

Figure00003. AI-powered CSRD Reporting Software, Global Market Size, Split by Product Segment

Based on or includes research from QYResearch: Global AI-powered CSRD Reporting Software Market Report 2026-2032.

In terms of product type, currently Data Collection and Integrated is the largest segment, hold a share of 29.6%.

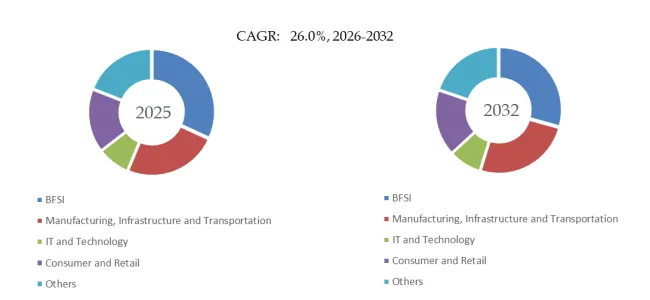

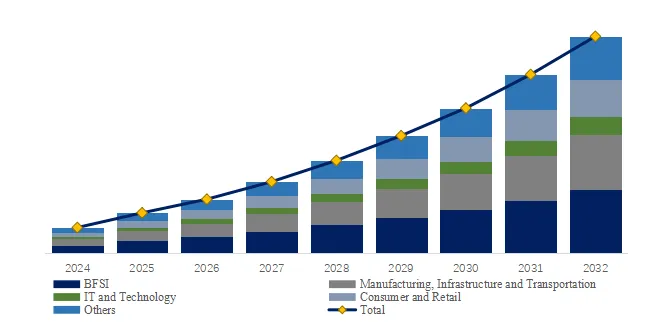

Figure00004. AI-powered CSRD Reporting Software, Global Market Size, Split by Application Segment

Based on or includes research from QYResearch: Global AI-powered CSRD Reporting Software Market Report 2026-2032.

In terms of product application, currently BFSI is the largest segment, hold a share of 31.9%.

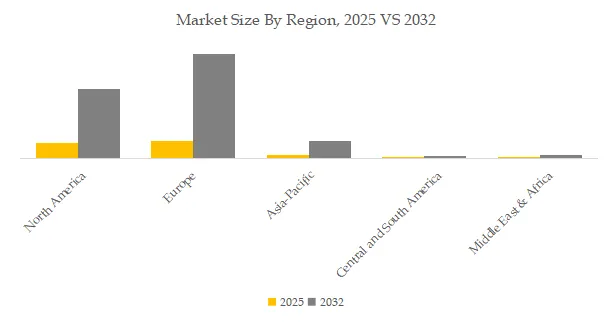

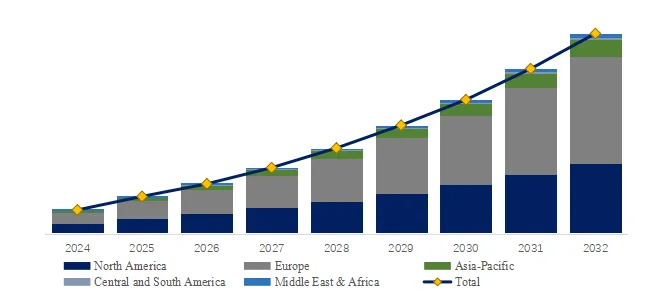

Figure00005. AI-powered CSRD Reporting Software, Global Market Size, Split by Region

Based on or includes research from QYResearch: Global AI-powered CSRD Reporting Software Market Report 2026-2032.

Key Drivers:

1. Regulatory & Compliance Drivers (The “Mandate”)

The Law is Non-Negotiable: CSRD is enshrined in EU law. Approximately 50,000+ companies are legally obligated to report. This is not a voluntary “nice-to-have”; it is a mandatory compliance exercise with deadlines and potential fines.

The Extraterritorial Reach: The law captures non-EU companies (US, Asia) with significant EU operations, expanding the Total Addressable Market (TAM) globally.

Assurance Requirements: The mandate for third-party auditing (“Limited Assurance”) renders manual spreadsheets obsolete, forcing companies into software with audit trails.

2. Operational Complexity Drivers (The “Pain Point”)

Volume of Data (1,000+ Data Points): The ESRS standards require disclosure on over 1,000 individual data points. Managing this manually is impossible.

Scope 3 Complexity: Mandatory reporting of value chain emissions requires collecting data from potentially thousands of suppliers. AI is the only scalable solution.

Unstructured Data: Sustainability data lives in PDFs, emails, and invoices. AI-powered OCR and NLP are required to digitize this information.

3. Economic & Financial Drivers (The “Incentive”)

Cost of Labor vs. Software: Hiring large sustainability teams is expensive. AI software offers a clear ROI by automating manual work.

Access to Capital: Investors and banks are tying financing terms (Green Bonds, Sustainability-Linked Loans) to verified ESG data, pushing companies towards auditable software.

Risk Mitigation: The cost of non-compliance (fines) or greenwashing (lawsuits, reputational damage) far exceeds the cost of software.

Key Challenges:

1. Data Quality & Availability Challenges

The “Garbage In, Garbage Out” Problem:

Issue: AI models are only as good as the data they are trained on. Many companies, especially SMEs, do not have historical sustainability data. If a company has never tracked water usage, no amount of AI can invent it.

Impact: Software vendors spend significant time on data cleansing and advisory services, which is not scalable.

Lack of Standardized Source Data:

Issue: Unlike financial data (which follows GAAP/IFRS), sustainability data from suppliers comes in thousands of different formats, units, and levels of quality.

Impact: AI models require constant retraining to interpret new and unusual data formats, increasing R&D costs.

2. The “AI Black Box” Problem (Explainability)

Issue: CSRD requires auditable data. If an AI model uses a complex neural network to estimate an emission factor, it must be able to explain how it arrived at that number to an external auditor.

Challenge: Many advanced AI models (especially deep learning) are inherently “black boxes.” They provide answers without clear reasoning.

Market Impact: Auditors and legal teams are pushing back against pure “AI” solutions, demanding “Explainable AI” (XAI) or deterministic calculations that can be easily verified. This slows the adoption of cutting-edge AI.

3. Integration Complexity with Legacy Systems

Issue: Large enterprises run on legacy ERP systems (SAP ECC, Oracle JD Edwards) that are decades old. These systems were not designed to output sustainability data.

Challenge: Building and maintaining connectors to these legacy systems is expensive and requires specialized engineering talent.

Market Impact: The “Data Collection” segment, while having the largest market share, also has the lowest profit margins due to the high cost of maintaining these integrations.

About QYResearch

QYResearch founded in California, USA in 2007. It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The AI-powered CSRD Reporting Software market is segmented as below:

By Company

SustainLab

Watershed

Benchmark Gensuite

Ecocharting

Pulsora

Workiva

Greenly

Planmark

Ecodrisil

ZeroScope

Glacier

Sweep

Greenomy

Coolset

Novisto

Footprint Intelligence

FINGREEN AI

Karomia

Klimado

Ecobio Manager

Code Gaia

Quentic

Position Gree

Segment by Type

End to End Solution

End to Cloud Solution

Segment by Application

Chemicals

Oil & Gas

Manufacturing

Transportation

Others

Each chapter of the report provides detailed information for readers to further understand the AI-powered CSRD Reporting Software market:

Chapter 1: Introduces the report scope of the AI-powered CSRD Reporting Software report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of AI-powered CSRD Reporting Software manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various AI-powered CSRD Reporting Software market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of AI-powered CSRD Reporting Software in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of AI-powered CSRD Reporting Software in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth AI-powered CSRD Reporting Software competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides AI-powered CSRD Reporting Software comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides AI-powered CSRD Reporting Software market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global AI-powered CSRD Reporting Software Market Outlook, In‑Depth Analysis & Forecast to 2031

Global AI-powered CSRD Reporting Software Market Research Report 2025

Global AI-powered CSRD Reporting Software Sales Market Report, Competitive Analysis and Regional Opportunities 2025-2031

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp