QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Photography Light Control Accessories- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Photography Light Control Accessories market, including market size, share, demand, industry development status, and forecasts for the next few years.

The global market for Photography Light Control Accessories was estimated to be worth US$ 94.50 million in 2024 and is forecast to a readjusted size of US$ 124 million by 2031 with a CAGR of 3.6% during the forecast period 2025-2031.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5376345/photography-light-control-accessories

Photography Light Control Accessories Market Summary

Photographic light control accessories are a general term for various tools used to actively intervene, shape, and optimize lighting effects during the shooting process. Their core function is to modify the inherent characteristics of natural or artificial light, including its quality, direction, intensity, color, and distribution. Common light control accessories include reflectors, softboxes/umbrellas, grids/grids, and beauty dishes/beauty dishes. Through sophisticated optical design and physical blocking principles, these accessories empower photographers with powerful capabilities, from subtle adjustments to complete lighting reshaping. They are indispensable technical means for achieving creative image expression, controlling tonal gradations, and enhancing the professionalism of their work. They are widely used in professional photography fields such as portraiture, still life, commercials, and film and television production.

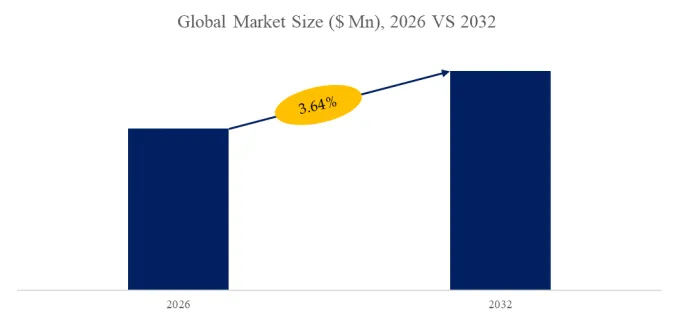

Driven by the explosive growth in global demand for video content creation and the popularization of photography technology, the Photography Light Control Accessories market is undergoing a structural transformation from traditional photography aids to core systems for video creation. According to the latest data from QYResearch, the global market size reached $99.7 million in 2025 and is projected to climb to $128 million by 2032, representing a CAGR of 3.64% from 2026 to 2032. This growth is supported by three core factors: the daily content upload volume on global short video platforms maintains a growth rate of over 25%, the cost of professional-grade LED light sources has decreased by 40% (compared to 2020), and the high-performance, cost-effective solutions provided by the Chinese supply chain (similar products are 30-50% cheaper than European and American brands). Currently, the market exhibits a clear trend of consumer segmentation: the high-end professional market pursues technological excellence, the mid-range creative market emphasizes ecosystem integrity, and the entry-level market focuses on portability and cost-effectiveness. This article analyzes product forms, competitive landscape, and regional market characteristics based on the technological changes in the content creation industry in 2025, providing decision-making references for the strategic adjustments of relevant enterprises.

Figure00001. Global Photography Light Control Accessories Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global Photography Light Control Accessories Market Report 2025-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

Technological Evolution: Intelligentization and Lightweighting Lead Product Innovation

The current technological development of Photography Light Control Accessories exhibits three main characteristics: intelligent integration, lightweight design, and the democratization of professional performance. With the maturity of LED light source technology, high color rendering index and stable color temperature have become industry standards, while true differentiation is gradually shifting towards wireless control, multi-device collaboration, and the integration of hardware and software ecosystems. The widespread adoption of lightweight carbon fiber materials and quick-release systems has significantly improved the mobility and deployment efficiency of professional equipment, enabling individual creators to quickly complete complex lighting setups.

From a product structure perspective, the market presents a dual-track pattern of professional and mass-market offerings. Professional film and television-grade accessories emphasize system integrity, environmental adaptability, and industrial-grade reliability, while the mass-market focuses more on a balance between portability, ease of use, and cost-effectiveness. It is worth noting that while intelligent Photography Light Control Accessories currently have a limited market share, they have become the fastest-growing segment, demonstrating a clear path for the industry to shift from a hardware-oriented to a system service-oriented approach.

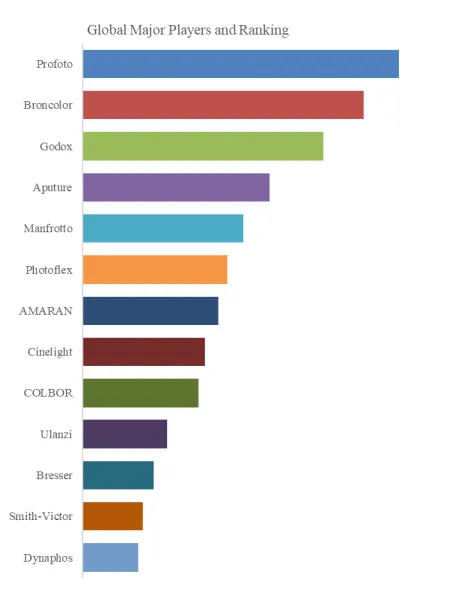

Figure00002. Global Photography Light Control Accessories Top 13 players Ranking (Ranking is based on the revenue of 2025, continually updated)

According to QYResearch Top Players Research Center, the global key manufacturers of Photography Light Control Accessories include Profoto, Broncolor, Godox, Aputure, Manfrotto, etc. In 2025, the global top five players had a share approximately 43.5% in terms of revenue.

Competitive Landscape and Vendor Dynamics

The global Photography Light Control Accessories market exhibits a three-tiered competitive landscape. The first tier, represented by European professional brands such as Profoto and Broncolor, holds approximately 25% of the high-end market share, leveraging their technological advantages and comprehensive ecosystems to build competitive barriers. The second tier includes brands like Aputure and Godox, holding approximately 50% of the market share and dominating the creator market through a “high performance + excellent cost-effectiveness” strategy. The third tier, represented by brands like Ulanzi and SmallRig, holds approximately 25% of the market share, meeting mass-market needs with rapid response and exceptional cost-effectiveness.

Regionally, North America and Europe together account for approximately 45% of the global market share, continuing to lead technological development. The Asia-Pacific market (centered on China) currently accounts for approximately 35%, projected to rise to 40% by 2032, becoming the main engine of industry growth. Emerging markets (Southeast Asia, Latin America, etc.) account for 20%, demonstrating significant growth potential with the rise of local content industries.

Cost Structure and Supply Chain Evolution

In 2025, fluctuations in global electronic component prices and changes in logistics costs will have a structural impact on the market: First, cost pressures will be transmitted, with gross profit margins for mid-to-low-end products generally shrinking by 5-8 percentage points, forcing brands to strengthen vertical integration of the supply chain or seek technological differentiation to maintain profits. Second, manufacturing centers will shift, with international brands relocating more mid-range product manufacturing to Southeast Asia (such as Vietnam and Thailand) to optimize costs and be closer to the market. Meanwhile, China’s supply chain, with its complete industrial support and engineering talent pool, will continue to upgrade towards R&D and high-end manufacturing. Third, channel transformation will deepen, with professional film and television equipment distributors still controlling the high-end market, but e-commerce platforms (especially interest-based e-commerce and B2B platforms) now account for more than 60% of sales in the mid-to-low-end market, driving the transformation of marketing models towards content-driven and scenario-based approaches.

Typical Cases and Technological Breakthroughs

Aputure has achieved market breakthroughs through its “technology equality” concept: its Light Storm series of lights, paired with the Sidus Link ecosystem, provides small and medium-sized teams with near-cinematic wireless lighting control solutions at a cost far lower than traditional high-end brands, and has been widely used in web dramas, advertising, and high-quality short video production. SmallRig, with its exceptional product definition and rapid supply chain response, has pioneered a new category of “modular ecosystem accessories.” Its magnetic connection system and abundant expansion parts meet the highly personalized lighting and shooting setup needs of creators, making it one of the preferred brands for DIY creators worldwide. Regarding technological challenges, the industry currently faces the issues of “heat dissipation and size balance for high-power LEDs” and the ecosystem barrier of “incompatibility between cross-brand wireless control protocols,” which provides breakthrough opportunities for companies with self-developed control systems and heat dissipation technologies.

Future Trends and Core Challenges

Technological convergence will profoundly reshape the industry landscape. The widespread adoption of virtual production technology will drive the deep integration of photography light control accessories with digital content production workflows, while the application of artificial intelligence in light simulation and automated lighting may redefine creative workflows. Business model innovation is also noteworthy; new models such as device-as-a-service and cloud-based lighting library subscriptions are emerging and may change the way value is distributed in the industry.

However, the industry still faces structural challenges such as ecosystem fragmentation due to inconsistent standards and homogeneous competition in the low-to-mid-end market. The next stage of competition will not only be a contest of product performance but also a comprehensive test of ecosystem building capabilities, depth of understanding of user scenarios, and continuous innovation. Companies that can grasp the pace of technological evolution, accurately position their target markets, and build differentiated competitive advantages will gain greater development space during this period of transformation.

About The Authors

|

Shang Tianmin – Main Analyst for this Article

Email: shangtianmin@qyresearch.com

Ms. Shang has 3 years of industry research experience, focusing on the fields of mechanical equipment (such as self-climbing cranes, autonomous surface ships, autonomous mobile robots 3D cameras, etc.) and business services and software (such as patent databases, cold storage lighting, laboratory piping systems, etc.). Ms. Sang is engaged in the development of technology and market reports and is good at pre-sales services for customized projects. |

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Photography Light Control Accessories market is segmented as below:

By Company

Manfrotto

Photoflex

Aputure

Ulanzi

Godox

Broncolor

Profoto

AMARAN

Cinelight

Bresser

Smith-Victor

Dynaphos

COLBOR

Segment by Type

Diffusion Accessories

Reflection Accessories

Blocking and Focusing Accessories

Gel Accessories

Others

Segment by Application

Professional Portrait Photography

Commercial Photography and Advertising

E-Commerce and Still Life Product Photography

Others

Each chapter of the report provides detailed information for readers to further understand the Photography Light Control Accessories market:

Chapter 1: Introduces the report scope of the Photography Light Control Accessories report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Photography Light Control Accessories manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Photography Light Control Accessories market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Photography Light Control Accessories in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Photography Light Control Accessories in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Photography Light Control Accessories competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Photography Light Control Accessories comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Photography Light Control Accessories market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Photography Light Control Accessories Market Research Report 2025

Global Photography Light Control Accessories Market Outlook, In‑Depth Analysis & Forecast to 2031

Global Photography Light Control Accessories Sales Market Report, Competitive Analysis and Regional Opportunities 2025-2031

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp