QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Sealing Leakage Monitoring System- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Sealing Leakage Monitoring System market, including market size, share, demand, industry development status, and forecasts for the next few years.

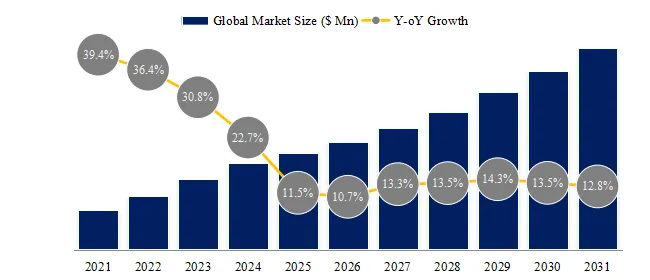

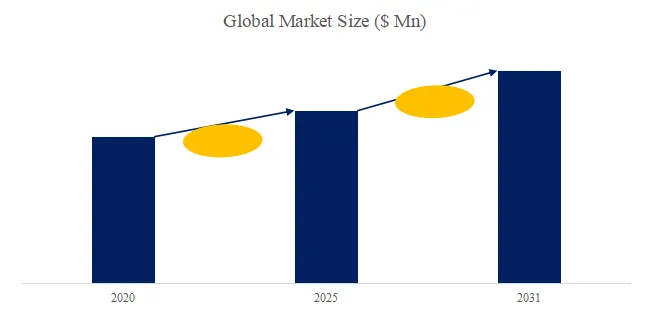

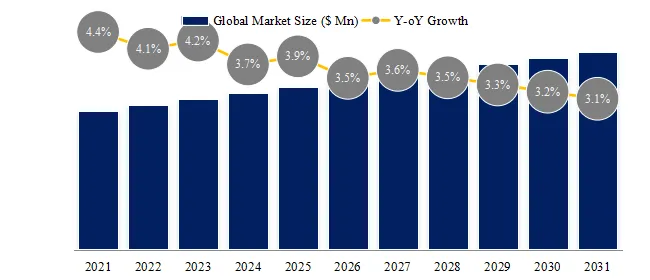

The global market for Sealing Leakage Monitoring System was estimated to be worth US$ 1312 million in 2025 and is projected to reach US$ 2190 million, growing at a CAGR of 7.6% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5686247/sealing-leakage-monitoring-system

Sealing Leakage Monitoring System Market Summary

According to the latest report “Global Sealing Leakage Monitoring System Market Report 2025-2031″ by the QYResearch research team, the global Sealing Leakage Monitoring System market size is expected to reach US$2 billion in 2031, with a compound annual growth rate (CAGR) of 7.6% in the next few years.

A sealing leakage monitoring system is a specialized system used for continuous or periodic monitoring of industrial installations, pipelines, tanks, valves, flanges, and other sealed connections. Its core purpose is to promptly identify and locate unplanned leaks of gas or liquid under conditions of seal failure. This system typically integrates sensor technology, data acquisition units, signal processing algorithms, and monitoring software. By analyzing changes in parameters such as pressure, flow rate, concentration, acoustics, infrared, or spectroscopy, it achieves early detection and risk warning for even minor leaks. Sealing leakage monitoring systems can be applied in industries such as oil and gas, chemicals, energy, power, pharmaceuticals, semiconductors, and environmental protection to ensure safe operation of equipment, reduce material loss, prevent environmental pollution, and meet regulatory compliance requirements. In practical applications, the system can be deployed independently or integrated with an enterprise’s existing automated control system, equipment management system, or safety instrumented system to form a leak management system covering the entire lifecycle of the equipment. Through systematic and digital monitoring methods, sealing leakage monitoring systems can help enterprises shift from reactive maintenance to predictive maintenance, improving operational reliability and overall operational efficiency.

The market for sealing leakage monitoring system is at a critical juncture of steady growth and technological upgrades. Its core drivers are increasingly stringent global safety and environmental regulations (such as the EPA’s LDAR regulations and the EU’s Industrial Emissions Directive), the urgent need for asset integrity management and preventative maintenance among enterprises, and the societal consensus on reducing volatile organic compound (VOC) emissions and ensuring production safety. The market is rapidly transitioning from traditional, periodic manual inspections to continuous, online, intelligent, and predictive monitoring models.

In terms of market size and growth, this is a typical B2B industrial market, substantial in scale and with stable growth. The fastest-growing segments include oil and gas, refining, and chemicals. These industries have complex processes, dense equipment, and highly hazardous media, making them the primary application areas for monitoring systems. Furthermore, the pharmaceutical and food and beverage industries’ requirements for clean production and product purity, as well as the power generation and offshore platforms’ pursuit of ultimate safety and reliability, are also contributing continuous growth to the market.

Regarding technological evolution trends, the market exhibits a clear path towards digitalization and intelligentization. Traditional dominant technologies—flame ionization detectors and optical gas imaging—are still widely used, but are undergoing deep integration with the Internet of Things (IoT). The current mainstream trend is to deploy fixed, networked sensor arrays (such as laser absorption spectroscopy and ultrasonic sensors) combined with wireless transmission technology to achieve 24/7 uninterrupted monitoring. The most cutting-edge development involves the introduction of artificial intelligence and big data analytics. Through deep learning of historical leakage data, equipment operating parameters, and environmental conditions, the system can not only provide real-time alarms but also predict potential failure risks of seals, achieving a paradigm shift from “responding after a leak” to “intervening before a leak.”

Looking ahead, this market will deeply benefit from the advancement of Industry 4.0 and “dual carbon” goals. Monitoring systems will no longer be isolated safety units but will be deeply integrated into the factory’s digital twin and overall asset performance management platform, becoming the fundamental data nodes for enterprises to achieve safe operation, energy efficiency improvement, and carbon footprint management. Simultaneously, specialized monitoring needs in emerging fields such as hydrogen energy and carbon capture and storage will also spur new technological iterations and market opportunities. Overall, the seal leakage monitoring system market has evolved from an auxiliary compliance tool into a core intelligent infrastructure ensuring industrial safety, environmental protection, and efficiency, and its strategic value and market potential are being continuously reassessed.

The primary driving force behind the development of sealing leakage monitoring systems stems from the continuous strengthening of safety and compliance. In high-risk industries such as petrochemicals, chemicals, pharmaceuticals, and energy, seal failures are often directly linked to leaks of toxic, harmful, and flammable media. Increasingly stringent regulations on VOC emissions, occupational health, and process safety in various countries are pushing companies to shift from post-inspection to online, continuous leak monitoring and early warning systems to meet compliance audits and safe production requirements. This has become the core external driver of market growth.

The second important driving factor is the higher reliability requirements resulting from the increasing scale and continuous operation of equipment. Modern process industry equipment tends to operate under high temperature, high pressure, and high corrosion conditions. Mechanical seals, flanges, and valves are numerous and have extended operating cycles, making it difficult for traditional manual inspections to detect minute leaks in a timely manner. Sealing leakage monitoring systems, through real-time data acquisition and trend analysis, can identify seal performance degradation in advance, reducing unplanned shutdowns and cascading failures, significantly lowering the total lifecycle maintenance cost, and thus gaining widespread acceptance from owners and EPC contractors.

Technological advancements are also a key internal factor driving the development of this system. The maturity of high-sensitivity sensors, wireless communication, low-power IoT, edge computing, and AI algorithms has upgraded leak monitoring from single-point alarms to multi-parameter fusion and intelligent diagnostics, significantly improving monitoring accuracy and reliability. Simultaneously, system deployment and maintenance costs continue to decline, expanding its application scope in small and medium-sized plants and existing infrastructure upgrade projects.

Furthermore, the trend of enterprise digitalization and smart factory construction is accelerating the popularization of seal leak monitoring systems. More and more companies want to integrate seal status data into DCS, MES, or asset management platforms to achieve equipment health management and predictive maintenance. Seal leak monitoring is no longer an isolated safety tool but has become an important data source for process optimization, energy efficiency management, and ESG indicator management. This extended value significantly enhances the investment attractiveness of the system.

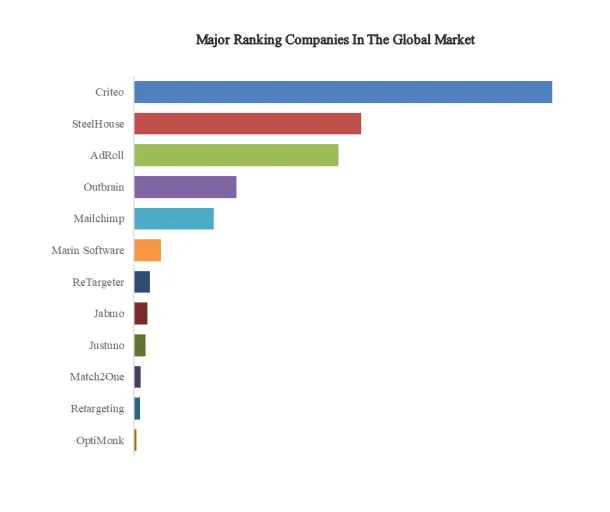

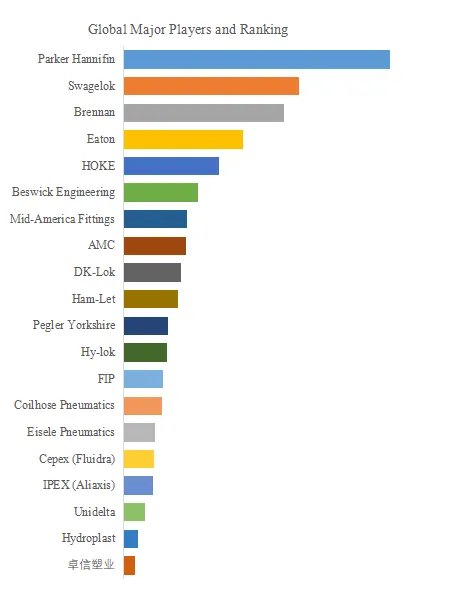

This report profiles key players of Sealing Leakage Monitoring System such as TEXPLOR、Flexaseal、EagleBurgmann、Qipack、KSB Group、Freudenberg-NOK Sealing Technologies、OMNTEC、KLINGER、INFICON、Ishida、ANHUI WANYI SCIENCE AND TECHNOLOGY CO., LTD.

The supply chain of a sealing leak monitoring system mainly comprises the following levels:

The supply chain begins with the upstream supply of core components and materials, which forms the cornerstone of the entire system’s technological level and reliability.

This segment is highly specialized and primarily includes: high-sensitivity sensor chips (such as laser diodes for TDLAS, microelectromechanical systems microphones for photoacoustic spectroscopy, and hydrogen flame ionization detectors for FID); precision optical components (lenses, filters, mirrors); high-performance data processing and transmission modules (embedded microprocessors, application-specific integrated circuits, and wireless communication modules); and special materials (such as Hastelloy sensor housings for corrosive environments and high-transmittance sapphire windows). Furthermore, mechanical structural components used for system integration, valves, and standard gases for calibration are also key upstream products. The core of competition in this field lies in the sensor’s sensitivity, selectivity, stability, power consumption, and cost; leading semiconductor and precision instrument companies possess strong technological barriers in this segment.

The midstream of the supply chain involves the research, development, integration, and manufacturing of the monitoring system, which is crucial for value creation and solution development.

Manufacturers integrate various upstream components with their proprietary algorithms, mechanical design, electrical engineering, and calibration technologies into deliverable products. This process involves several layers: first, detection instrument manufacturers produce handheld, portable, or stationary gas detectors and imagers; second, system integrators integrate sensors, sampling probes, data acquisition devices, communication gateways, and software platforms into complete online monitoring systems or LDAR solutions; and third, software and data analytics service providers develop cloud platforms or local server software responsible for data aggregation, visualization, alarm management, and predictive diagnostics. The core competitiveness of midstream companies lies in their ability to integrate multiple technology routes, the robustness of their systems in complex industrial environments, the ease of use and intelligence of their software, and their engineering capabilities to meet different industry standards (such as SIL certification).

Downstream in the industry chain is the deployment, service, and end-user application of the systems, directly facing end users and creating real value.

Engineering service providers and maintenance companies are responsible for installing the midstream systems at the customer’s factory site, conducting commissioning, calibration, and training. Subsequently, the industry chain has spawned a continuous service market, including LDAR compliance testing services (regular leak detection and repair as required by regulations), system hosting and data interpretation services, and predictive maintenance consulting services. The end-use market spans all industries involving hazardous media or with stringent sealing requirements: petrochemicals, natural gas processing, and refining are the largest consumers, monitoring VOCs leaks in flanges, valves, and pumps; the pharmaceutical and fine chemical industries focus on sterile environments and product cross-contamination; the power industry (especially nuclear and thermal power) focuses on leaks of working fluids such as hydrogen and SF6; the food and beverage industry monitors ammonia refrigerant leaks; and emerging hydrogen energy industry chains and carbon capture and storage projects have placed new, high-standard demands on seal monitoring.

Throughout the entire industry chain is a powerful horizontal support and driving system. The core driving force is increasingly stringent global and local environmental and safety regulations (such as the US EPA’s OOPSA and LDAR rules, and China’s “Standard for the Control of Unorganized Emissions of Volatile Organic Compounds”), which have created mandatory market demand. International standards and certification systems (such as IECEx and ATEX explosion-proof certification, and SIL functional safety certification) ensure market access and reliability of products. Continuous R&D and innovation focus on sensor technologies with higher sensitivity and lower power consumption, as well as intelligent diagnostic algorithms based on artificial intelligence and digital twins. A comprehensive distribution channel and technical service network ensures that complex systems receive timely and effective support, completing the entire process from product sales to value realization. Ultimately, the value of this industry chain lies not only in selling hardware and software, but also in providing customers with reliable data and decision-making support to ensure safety, compliance, efficiency, and risk reduction.

The competitive landscape of sealing leakage monitoring systems exhibits the following characteristics: From a segmented perspective, the competitive landscape of sealing leakage monitoring systems is primarily reflected in the differentiated competition between different technological approaches. One type of manufacturer focuses on gas detection and analysis technology, emphasizing online monitoring of VOCs, combustible or toxic gases. Their advantages lie in high sensitivity and strong regulatory compliance, with typical customers concentrated in the petrochemical and fine chemical industries. Another type of manufacturer uses multi-parameter sensing, such as pressure, temperature, vibration, and acoustic emission, to determine sealing status through indirect characteristics. They emphasize trend analysis and predictive maintenance capabilities, making them suitable for large-scale, continuously operating installations. Meanwhile, solutions based on wireless sensor networks and low-power nodes are forming a new niche market, primarily targeting the retrofitting of existing installations and large-scale deployments.

From the perspective of company type, market competition exhibits cross-industry integration characteristics. Traditional process instrumentation and automation giants, leveraging their complete product lines, global service networks, and deep integration with DCS systems, dominate the high-end and large-scale project markets. Specialized sealing and rotating equipment manufacturers, on the other hand, enter the market through integrated “sealing + monitoring” solutions, leveraging their deep understanding of failure mechanisms and extensive field experience to demonstrate strong competitiveness in critical equipment and high-value application scenarios. Meanwhile, a number of industrial IoT and software companies, excelling in algorithms, platforms, and data analysis, emphasize system openness and rapid deployment, continuously expanding their influence in digital transformation and multi-brand equipment usage scenarios.

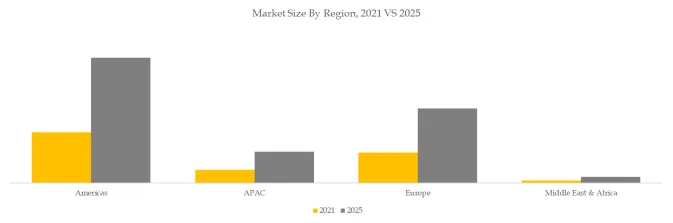

From a regional and customer structure perspective, the competitive landscape also exhibits clear stratification. The European, American, and Japanese markets have high technological maturity and well-established standards, with customers placing greater emphasis on system reliability and compliance certification, resulting in a high concentration of leading manufacturers. China and other emerging markets are in a rapid adoption phase, with local manufacturers possessing significant advantages in cost control, customization, and local services, creating differentiated competition with international brands. This leads to a large number of market participants and relatively low market concentration.

Overall, the sealing leakage monitoring system industry presents a competitive landscape characterized by “diverse technological approaches, diverse enterprise types, and significant regional differentiation.” In the short term, leading manufacturers will continue to dominate the high-end market due to their brand, certification, and system integration capabilities. In the medium to long term, with increasingly stringent regulations and deeper digitalization, comprehensive manufacturers that can integrate sensing hardware, diagnostic algorithms, and platform services are expected to increase their market share, and the industry concentration is likely to gradually increase.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Sealing Leakage Monitoring System market is segmented as below:

By Company

TEXPLOR

Flexaseal

EagleBurgmann

Qipack

KSB Group

Freudenberg-NOK Sealing Technologies

OMNTEC

KLINGER

INFICON

Ishida

WANYI

Segment by Type

Optical/Visual Monitoring

Acoustic/Ultrasonic Monitoring

Others

Segment by Application

Chemicals

Power

Pharmaceuticals

Food

Others

Each chapter of the report provides detailed information for readers to further understand the Sealing Leakage Monitoring System market:

Chapter 1: Introduces the report scope of the Sealing Leakage Monitoring System report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Sealing Leakage Monitoring System manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Sealing Leakage Monitoring System market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Sealing Leakage Monitoring System in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Sealing Leakage Monitoring System in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Sealing Leakage Monitoring System competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Sealing Leakage Monitoring System comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Sealing Leakage Monitoring System market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Sealing Leakage Monitoring System Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Sealing Leakage Monitoring System Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Sealing Leakage Monitoring System Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp