QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Outdoor Camping Headlamp- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Outdoor Camping Headlamp market, including market size, share, demand, industry development status, and forecasts for the next few years.

The global market for Outdoor Camping Headlamp was estimated to be worth US$ 147 million in 2024 and is forecast to a readjusted size of US$ 221 million by 2031 with a CAGR of 6.1% during the forecast period 2025-2031.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/3539136/outdoor-camping-headlamp

Outdoor Camping Headlamp Market Summary

Outdoor camping headlamp is a head-mounted lighting device designed for camping and outdoor activity scenarios, with the primary objective of providing hands-free illumination with stable output and repeatable user experience. These products typically balance wide-area flood lighting with reliable runtime performance, making them suitable for campsite setup, nighttime movement, and multitasking activities. Compared with handheld lighting tools, camping headlamps offer clear advantages in operational freedom, wearing convenience, and sustained reliability, while their weather resistance and structural robustness allow consistent performance in outdoor environments.

According to the new market research report “Global Outdoor Camping Headlamp Market Report 2026-2032”, published by QYResearch, the global Outdoor Camping Headlamp market size is projected to reach USD 215 million by 2032, at a CAGR of 5.3% during the forecast period.

Figure00001. Global Outdoor Camping Headlamp Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global Outdoor Camping Headlamp Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

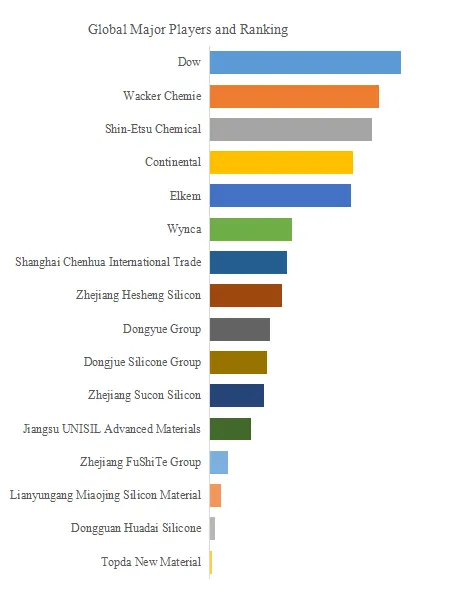

Figure00002. Global Outdoor Camping Headlamp Top 15 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Outdoor Camping Headlamp Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

According to QYResearch Top Players Research Center, the global key manufacturers of Outdoor Camping Headlamp include Black Diamond, Petzl, Fenix, BioLite, Energizer, etc. In 2025, the global top five players had a share approximately 38.0% in terms of revenue.

Industrial Chain

In the upstream segment of the industrial chain, outdoor camping headlamps rely primarily on LED chips and lithium batteries as core components. LED chips determine luminous efficiency, color quality, and thermal stability, forming the foundation of lighting performance. Representative LED suppliers include Nichia, OSRAM, and Cree LED, all of which have established track records in high-efficiency and high-reliability lighting solutions. Lithium batteries directly affect runtime, safety, and cycle life, with representative suppliers including CATL, Samsung SDI, and LG Energy Solution. The performance consistency and quality control of upstream components directly influence brightness stability, runtime reliability, and product safety.

The midstream segment represents the core value-creation stage for outdoor camping headlamps. It encompasses optical and thermal design, driver and control system development, battery system integration, waterproof and impact-resistant structural design, reliability testing, and final assembly and quality control. Manufacturers must carefully balance luminous output, power consumption, and heat dissipation while ensuring stable performance under repeated charge–discharge cycles, drops, and environmental exposure. Engineering capability at this stage determines brightness consistency, usable runtime, and total product lifespan, directly shaping brand reputation and user loyalty.

In the downstream segment, outdoor camping headlamps are primarily sold through online and offline retail channels to end consumers. Online channels emphasize specification transparency and user reviews, while offline channels focus on fit, comfort, and hands-on experience. Because usage scenarios are frequent and highly repeatable, manufacturers seek to build brand loyalty through scenario-based configurations and consistent product quality. Premium positioning is increasingly achieved through reliability and user experience rather than pure price competition.

Influencing Factors

Drivers:

The market faces challenges from product homogenization and price-driven competition. Basic lighting specifications are easily replicated, leading some products to compete primarily on lumen output rather than long-term performance. In addition, battery safety, waterproofing reliability, and consistency over long-term use require strong engineering and quality validation capabilities, creating hurdles for smaller or less experienced brands.

Challenges:

The market faces challenges from product homogenization and price-driven competition. Basic lighting specifications are easily replicated, leading some products to compete primarily on lumen output rather than long-term performance. In addition, battery safety, waterproofing reliability, and consistency over long-term use require strong engineering and quality validation capabilities, creating hurdles for smaller or less experienced brands.

Trend:

Looking ahead, outdoor camping headlamps are expected to evolve toward higher energy efficiency, more intelligent control, and stronger environmental adaptability. Multi-mode lighting, refined brightness management, and more robust battery systems will become key areas of differentiation. As consumers place greater emphasis on durability and user experience, market competition is likely to shift from price-centric strategies toward quality- and reputation-driven positioning.

About The Authors

Lead Author: Julie Zhang

Email: zhangjianan@qyresearch.com

Julie Zhang, a key industry analyst a industry analyst of QYResearch (Beijing Hengzhou Bozhi International Information Consulting Co.,Ltd.), focuses on market research and trend forecasting of the entire industry chain upstream and downstream of the electric vehicle and lithium battery industry, we are good at providing strategic market insights through in-depth data mining, focusing on trends and technological innovations in the automotive and lithium battery industry, and helping the company achieve sustainable success in the highly competitive market environment. Typical studies include Electronic Fusing IC, EV Skateboard Platform, Electric Vehicle Controller, Automotive Interior Monitoring System, Automotive PCIe Switch Chips, End-To-End Automotive Software Platform, LiFSI Electrolyte Salts, Portable Power Supply, Outdoor Mobile Powers, and Solar Energy Storage Battery, etc.

About QYResearch

QYResearch founded in California, USA in 2007. It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Outdoor Camping Headlamp market is segmented as below:

By Company

Energizer

Petzl

Nitecore

BioLite

Black Diamond

GRDE

Coast

Shining Buddy

Thorfire

Xtreme Bright

Northbound Train

Aennon

Lighting Ever

VITCHELO

Yalumi Corporation

FENIX

RAYVENGE

Durapower

Browning

Sunree

Boruit

Rayfall Technologies

Segment by Type

Rechargeable Type

Batteries Type

Segment by Application

Online Store

Specialty Shop

Supermarket

Other

Each chapter of the report provides detailed information for readers to further understand the Outdoor Camping Headlamp market:

Chapter 1: Introduces the report scope of the Outdoor Camping Headlamp report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Outdoor Camping Headlamp manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Outdoor Camping Headlamp market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Outdoor Camping Headlamp in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Outdoor Camping Headlamp in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Outdoor Camping Headlamp competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Outdoor Camping Headlamp comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Outdoor Camping Headlamp market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Outdoor Camping Headlamp Sales Market Report, Competitive Analysis and Regional Opportunities 2025-2031

Global Outdoor Camping Headlamp Market Outlook, In‑Depth Analysis & Forecast to 2031

Global Outdoor Camping Headlamp Market Research Report 2025

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp