Global Leading Market Research Publisher QYResearch announces the release of its latest report “Dustproof and Waterproof Center Caps – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Dustproof and Waterproof Center Caps market, including market size, share, demand, industry development status, and forecasts for the next few years.

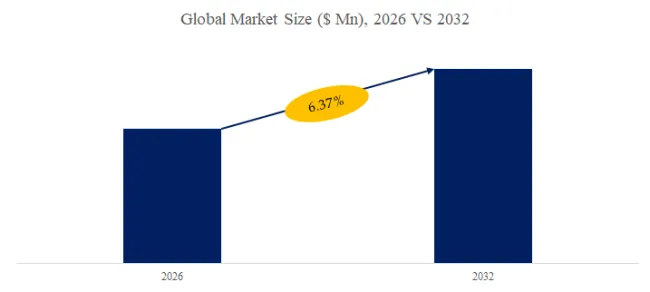

For automotive OEMs, aftermarket wheel manufacturers, and vehicle owners, the wheel hub assembly represents a critical component that must be protected from environmental contaminants to ensure longevity and performance. Standard decorative center caps, while aesthetically pleasing, often fail to prevent the ingress of dust, water, mud, and road salt—contaminants that can accelerate bearing wear, corrode lug nuts, and compromise hub integrity. Dustproof and waterproof center caps address this vulnerability with protective covers engineered with sealed designs, gaskets, or advanced materials that prevent environmental ingress. These specialized caps protect wheel bearings, lug nuts, and hub assemblies while maintaining aesthetic appeal, making them essential for vehicles exposed to harsh weather, off-road conditions, or high-performance environments. The global market for dustproof and waterproof center caps was valued at US$ 1,471 million in 2025 and is projected to grow at a CAGR of 5.1% to reach US$ 2,074 million by 2032, driven by increasing demand for enhanced wheel protection in SUVs, off-road vehicles, and premium automotive segments. In 2024, global production reached approximately 254.5 million units, with an average market price of US$ 5.5 per unit.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6097233/dustproof-and-waterproof-center-caps

Market Definition and Product Segmentation

Dustproof and waterproof center caps represent a specialized category within automotive wheel accessories, distinguished by their engineered sealing capabilities that go beyond decorative function. These caps incorporate gaskets, O-rings, or advanced material formulations to create a barrier against environmental contaminants while maintaining the aesthetic appearance expected of premium wheel accessories.

Mounting Type Segmentation

The market is stratified by attachment mechanism, each addressing distinct application and durability requirements:

- Snap-on Type: The dominant segment for OEM and aftermarket applications, featuring a friction-fit design that allows for quick installation without tools. Snap-on caps are widely used in passenger vehicles and offer cost-effective protection with adequate sealing for standard driving conditions.

- Screw-on Type: The premium segment for high-performance and off-road applications, featuring threaded attachment that provides a more secure, vibration-resistant fit. Screw-on caps are preferred for vehicles subjected to severe conditions where snap-on caps may be dislodged by impacts or vibrations.

- Magnetic Type: The emerging segment for specialized applications, utilizing magnetic retention for tool-free installation with enhanced security. Magnetic caps offer advantages in applications requiring frequent wheel access.

Application Segmentation

The market serves two distinct channels:

- OEM: Factory-installed caps designed to meet manufacturer specifications for fit, finish, and durability. OEM applications represent the larger volume segment, with automakers increasingly specifying sealed center caps as standard equipment on SUVs, trucks, and premium vehicles.

- Aftermarket: Replacement and upgrade caps offering enhanced protection or aesthetic customization. Aftermarket demand is driven by vehicle owners seeking to upgrade standard caps to sealed versions, particularly in regions with harsh winter road conditions and among off-road enthusiasts.

Competitive Landscape

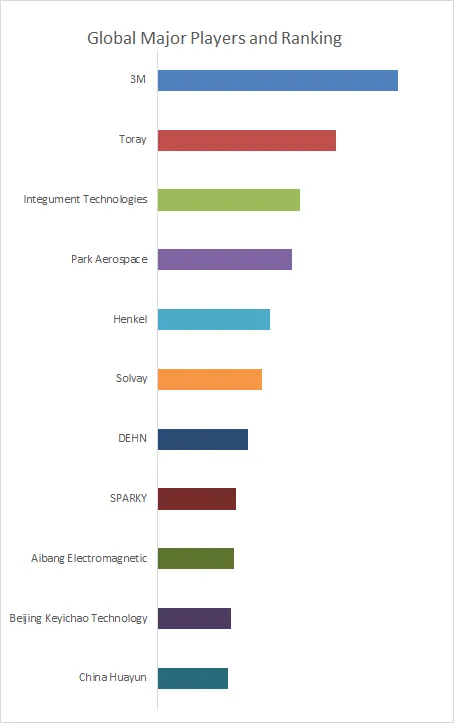

The dustproof and waterproof center caps market features a competitive landscape combining premium wheel manufacturers with specialized automotive accessory suppliers. Key players include BBS, OZ, Antera, ATS, Enkei, Rays, Advan, Yakuhama, Wed’s, Work, HRE, Giovanna, American Racing, Vossen, Forgiato, Vorsteiner, Adv.1, 3SDM, and Mercedes-Benz.

Industry Development Characteristics

1. SUV and Off-Road Vehicle Growth

A case study from QYResearch’s industry monitoring reveals that the proliferation of SUVs, crossovers, and off-road vehicles has increased demand for sealed center caps. These vehicles are frequently exposed to mud, water, and road salt—conditions that accelerate hub corrosion and bearing wear—making effective sealing essential for component longevity.

2. Winter and Harsh Climate Applications

In regions with harsh winter conditions, road salt and slush cause rapid corrosion of unprotected wheel components. A case study from the automotive aftermarket indicates that sealed center caps are highly valued in northern climates, where standard caps often fail to prevent salt ingress that leads to seized lug nuts and accelerated hub wear.

3. Premium and Performance Vehicle Segments

High-performance and luxury vehicle owners increasingly demand components that combine aesthetics with functional protection. A case study from the premium wheel market indicates that sealed center caps are standard on many luxury and performance models, reflecting consumer expectations for both appearance and durability.

4. Material and Sealing Technology Advances

Advances in sealing materials—including high-durability elastomers, UV-resistant polymers, and anti-corrosion coatings—have improved the long-term performance of sealed center caps. A case study from the materials sector indicates that modern sealing technologies maintain integrity across temperature extremes and prolonged exposure to environmental contaminants.

Strategic Outlook

For industry executives, investors, and marketing leaders evaluating opportunities in the dustproof and waterproof center caps market, the projected 5.1% CAGR reflects sustained demand from SUV and off-road vehicle growth, harsh climate applications, and the increasing emphasis on wheel component protection. Manufacturers positioned to capture disproportionate share share three characteristics: demonstrated expertise in sealing technology and material science; product portfolios spanning snap-on, screw-on, and magnetic configurations; and established relationships with OEM wheel manufacturers, aftermarket distributors, and premium automotive brands. As the market evolves toward integrated wheel systems and enhanced durability requirements, the ability to deliver reliable, aesthetically appealing, and robust sealing solutions will define competitive leadership.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp