High-end Electronic Glass Fiber Cloth Market Summary

High-end Electronic Glass Fiber Cloth is a premium electronic reinforcement material manufactured from high-purity electronic-grade glass fiber yarn through high-precision weaving and advanced surface treatment processes. It is designed to meet stringent requirements for electrical performance, consistency, and long-term reliability in advanced electronic substrates. The product delivers excellent electrical insulation, stable dielectric properties, and superior dimensional, thermal, and chemical stability. Its advantages lie in enabling high-density circuit design, improved signal integrity, and robust compatibility with high-performance resin systems, making it suitable for high-reliability electronic applications.

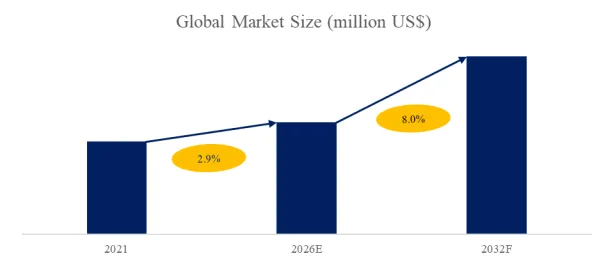

According to the new market research report “Global Electronic Glass Cloth for CCL Market Report 2026-2032”, published by QYResearch, the global Electronic Glass Cloth for CCL market size is projected to reach USD 2.73 billion by 2032, at a CAGR of 5.5% during the forecast period.

Figure00001. Global High-end Electronic Glass Fiber Cloth Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global High-end Electronic Glass Fiber Cloth Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

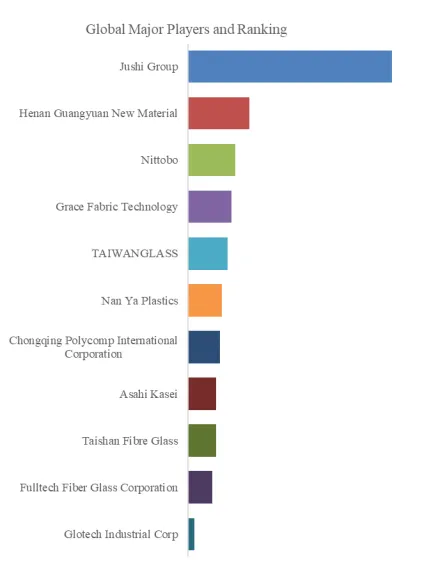

Figure00002. Global High-end Electronic Glass Fiber Cloth Top 11 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global High-end Electronic Glass Fiber Cloth Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

According to QYResearch Top Players Research Center, the global key manufacturers of High-end Electronic Glass Fiber Cloth include Jushi Group, Henan Guangyuan New Material, Nittobo, etc. In 2025, the global top three players had a share approximately 47.1% in terms of revenue.

Industrial Chain

Upstream:

The upstream of high-end electronic glass fiber cloth consists of electronic-grade glass fiber yarn, which accounts for approximately 60%–70% of total cost and represents the most technically demanding core segment. The production process uses raw materials such as silica sand, limestone, soda ash, and kaolin, which are melted at temperatures exceeding 1,400°C to form molten glass. Through precise formulation control (e.g., SiO₂, Al₂O₃, B₂O₃ content), key properties such as low dielectric constant, low thermal expansion, and high thermal stability are achieved. The molten glass is then drawn through platinum-rhodium bushings at high speed to form ultra-fine filaments with diameters of approximately 5–9 μm. These fibers are coated with specialized sizing agents to ensure high consistency and weavability, and are subsequently assembled into yarn. This segment requires exceptional expertise in formulation design, furnace operation, and fiber drawing processes. Representative companies include Nittobo, Asahi Kasei, Taiwan Glass Group, Honghe Technology, and Sinoma Science & Technology.

Midstream:

The midstream involves the weaving and post-processing of electronic glass fiber cloth, which is the key stage for achieving targeted material performance. Through ultra-fine yarn weaving technology, precise tension control, and defect management, manufacturers can produce ultra-thin fabrics (including extremely thin cloth), with high uniformity and low defect rates. Surface treatment and sizing optimization further enable properties such as low dielectric constant (Low-Dk), low dielectric loss (Low-Df), and low coefficient of thermal expansion (Low-CTE), meeting the requirements of high-frequency and high-speed signal transmission. The core competitiveness of this segment lies in weaving precision, yield control, and product consistency validation.

Downstream:

Downstream applications are primarily concentrated in high-end copper clad laminates (CCL) and printed circuit boards (PCB), which serve high-frequency and high-speed electronic systems. Key applications include AI servers, data centers, advanced communication equipment (5G/future 6G), automotive electronics, and high-end consumer electronics. Representative customers include Huawei, ZTE, Samsung Electronics, Foxconn, and Intel. Increasing demand for low loss, high reliability, and dimensional stability continues to drive the high-end evolution of electronic glass fiber cloth.

Influencing Factors

Key Drivers:

The rapid development of AI chips is accelerating the upgrade of high-end electronic glass fiber cloth toward higher frequency, higher speed, and greater reliability. As AI training and inference workloads continue to grow, chip packaging and board-level interconnects are evolving toward higher bandwidth and lower latency. This places more stringent requirements on dielectric stability, low loss characteristics, and dimensional stability of CCL and high-speed PCBs. As a result, electronic glass fiber cloth must continuously improve in ultra-fine yarn technology, weaving uniformity, defect control, and surface treatment consistency. Meanwhile, rising power consumption of AI chips introduces greater thermal stress, making high Tg systems, low CTE matching, and superior moisture and heat resistance critical. Companies with capabilities in ultra-thin fabric mass production, high yield rates, and rapid customer qualification are expected to capture significant growth opportunities in high-end applications.

Key Barriers:

Intensifying competition and product homogenization have led to price declines, posing a major challenge to profitability in the high-end electronic glass fiber cloth market. Mid- and low-end products, due to high standardization, are prone to periodic oversupply, forcing manufacturers to compete on price and compress margins. Even in the high-end segment, as technology diffuses and capacity expands, coupled with increasing concentration among downstream CCL manufacturers, bargaining power is gradually shifting to customers, intensifying price competition. Companies lacking differentiation in key areas such as ultra-thin capability, low defect rates, high strength, and automotive-grade reliability (e.g., CAF resistance) may face the risk of “volume growth without profit growth.” Therefore, the industry increasingly relies on cost control, yield improvement, and optimization of high-end product mix to maintain competitiveness.

Industry Trends:

The high-end electronic glass fiber cloth industry is accelerating toward vertical integration and premiumization. Leading companies are building integrated value chains from glass fiber yarn to fabric production, enabling full-process control from formulation design and fiber drawing to weaving. This integration enhances product consistency, performance stability, and yield rates while mitigating risks from upstream raw material price fluctuations and reducing manufacturing costs through process synergy. In ultra-thin and high-frequency/high-speed applications, integrated capabilities allow for customized product development tailored to specific scenarios, improving value-added and pricing power. As production scale expands to tens of millions of square meters, the combined effect of scale and technological barriers will further strengthen the competitive position of leading players. Additionally, improved supply chain responsiveness and controllability will enhance stable supply capabilities and long-term growth potential in the global high-end electronic materials market.

About The Authors

Lead Author: Julie Zhang

Email: zhangjianan@qyresearch.com

Julie Zhang, a key industry analyst a industry analyst of QYResearch (Beijing Hengzhou Bozhi International Information Consulting Co.,Ltd.), focuses on market research and trend forecasting of the entire industry chain upstream and downstream of the electric vehicle and lithium battery industry, we are good at providing strategic market insights through in-depth data mining, focusing on trends and technological innovations in the automotive and lithium battery industry, and helping the company achieve sustainable success in the highly competitive market environment. Typical studies include Electronic Fusing IC, EV Skateboard Platform, Electric Vehicle Controller, Automotive Interior Monitoring System, Automotive PCIe Switch Chips, End-To-End Automotive Software Platform, LiFSI Electrolyte Salts, Portable Power Supply, Outdoor Mobile Powers, and Solar Energy Storage Battery, etc.

About QYResearch

QYResearch founded in California, USA in 2007. It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp