Medical Laser Rental Service Market Summary

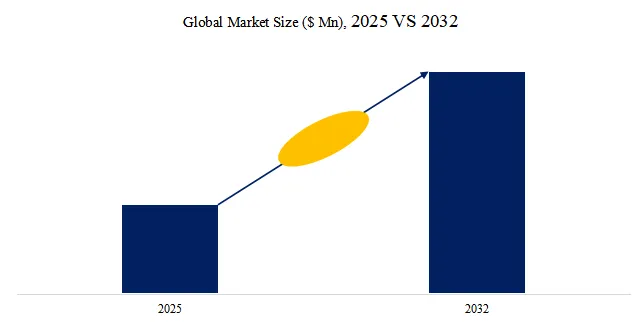

According to the latest report “Global Medical Laser Rental Service Market Report 2025-2031″ by the QYResearch research team, the global Medical Laser Rental Service market size is expected to reach US$1.953 billion in 2031, with a compound annual growth rate (CAGR) of 11.2% in the next few years.

Medical laser rental services represent an equipment utilization model tailored for healthcare institutions, offering temporary or long-term access to high-performance laser devices through leasing rather than outright purchase. This approach aims to alleviate the pressure of capital expenditures on hospitals and clinics while simultaneously meeting their needs for flexible equipment usage. The service encompasses a wide array of medical laser types—including CO2 lasers, diode lasers, Nd:YAG lasers, and pulsed dye lasers—and finds extensive application across disciplines such as dermatology, ophthalmology, dentistry, general surgery, and aesthetic medicine. Service packages typically include equipment installation, operational training, routine maintenance, and technical support; lease terms can be flexibly structured on a daily, monthly, or annual basis to accommodate the diverse clinical requirements of healthcare institutions of varying sizes. This leasing model empowers healthcare providers to achieve greater flexibility in upgrading their equipment fleets while simultaneously minimizing asset idle rates and depreciation costs. The upstream segment of this industry involves laser manufacturers and suppliers of core optical components, while the downstream segment targets hospitals, clinics, and specialized medical aesthetic centers. Driven by the growing demand among healthcare institutions for cost containment and efficient equipment utilization—coupled with the expanding multidisciplinary application of laser technology—medical laser rental services have emerged as a vital complementary model within the broader medical equipment service sector, demonstrating continuously expanding market potential.

From a holistic market perspective, medical laser rental services are gradually transitioning from a supplementary option to a mainstream equipment procurement strategy. The primary drivers behind this shift are the tightening of capital expenditure budgets within healthcare institutions and the significantly accelerated upgrade cycles for high-end laser equipment. While demand for multi-wavelength, multi-functional laser systems continues to rise across surgery, dermatology, ophthalmology, and medical aesthetics, the high unit costs, rapid technological obsolescence, and inherent risks of asset idleness associated with such devices make “leasing over buying” a distinctly advantageous strategy in terms of cost control and technological agility. Consequently, the market penetration rate of rental services has seen particularly pronounced growth among small-to-medium-sized hospitals and private healthcare institutions.

In terms of regional and demand-side structures, the North American and European markets are characterized by mature regulatory frameworks and clearly defined requirements within specialized medical fields; consequently, rental services in these regions tend to focus on high-end surgical and ophthalmological laser systems. The Asia-Pacific region, conversely, is benefiting from the expansion of healthcare service capacity and the growth of consumer spending on medical aesthetics; demand here leans more toward lasers for dermatological and minimally invasive treatments, characterized by rapid growth rates but also more intense price competition. Overall, it is projected that medical laser rental services will become a pivotal pathway for the commercialization of high-value medical equipment in the future—offering long-term growth potential characterized by stable cash flows, scalable business models, and synergistic value amplification through integration with consumables and data-driven services. The growth of medical laser rental services is primarily driven by a confluence of factors.

First and foremost, the need for healthcare institutions to control equipment investment costs serves as the core driving force; given the high price tags associated with high-performance lasers, the leasing model significantly reduces capital expenditure and alleviates depreciation pressures—making it particularly well-suited for small-to-medium-sized hospitals and private clinics.

Secondly, the rapid pace of technological advancement is another critical factor; as medical lasers undergo frequent iterations, leasing enables institutions to flexibly upgrade their equipment, thereby maintaining the cutting edge of clinical technology without incurring the long-term risks associated with outright ownership.

Thirdly, the demand for healthcare services continues to rise—particularly in the fields of dermatology, ophthalmology, dentistry, and medical aesthetics—where increasing patient volumes and treatment frequencies are fueling a growing need for the flexible availability of laser systems.

Furthermore, increasingly stringent regulatory policies and medical device market access requirements are prompting institutions to rely more heavily on service providers for equipment training, maintenance, and compliance support, thereby mitigating operational risks.

Finally, the enhanced service integration capabilities inherent in the leasing model—including remote monitoring, routine maintenance, and operational training—enable hospitals to utilize their equipment resources more efficiently and boost overall clinical operational effectiveness. Taken together, cost control, technological innovation, growing market demand, and service convenience collectively serve as the driving forces behind the continued expansion of the medical laser rental services market.

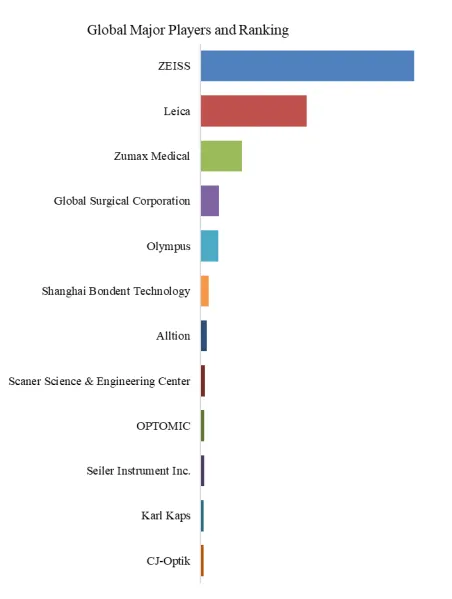

This report profiles key players of Medical Laser Rental Service such as Agiliti、Monarch、HealthTronics、Laser RX、Southeast Laser、Laser Service Solutions、Advanced Surgical Technologies、VMS Biomedical、Nuderma Esthetique、Allura Glow LLP、Lasers2u、MapQuest、Med One Group、Luxinar、Phoxton.

The value chain of medical laser rental services constitutes a comprehensive industrial ecosystem centered on equipment manufacturers and rental service providers, bolstered by capital support, and driven by the demand from end-user medical institutions. Built around the “lease-over-buy” business model, this value chain efficiently bridges the gap between high-end laser equipment and the demand for medical services, thereby emerging as a pivotal pathway for the commercialization of high-value medical devices. The following sections provide a detailed breakdown of this value chain across its three distinct segments: upstream, midstream, and downstream.

Upstream of the Value Chain: Laser Equipment Manufacturing and Capital Supply.

The upstream segment of the value chain primarily encompasses two core elements: the R&D and manufacturing of medical laser equipment, and the capital resources that facilitate equipment procurement. Together, these elements constitute the material foundation and financial guarantee upon which rental services are built.

In the equipment manufacturing segment, upstream suppliers consist primarily of manufacturers producing various types of medical lasers. The products manufactured by these firms span a diverse range of categories, including aesthetic lasers (such as picosecond and CO2 lasers), surgical lasers (used in fields such as urology and gynecology), and ophthalmic lasers (such as femtosecond lasers). The equipment itself is characterized by high unit costs, rapid technological iteration, and demanding maintenance requirements; the acquisition cost for a single piece of high-end medical laser equipment can range from hundreds of thousands to millions of RMB, making it financially burdensome—if not prohibitive—for many medical institutions to bear the upfront capital pressure of a direct purchase.

In the capital support segment, financial leasing companies and leasing platforms established directly by equipment manufacturers play a pivotal role. Licensed financial institutions—exemplified by firms such as CITIC Financial Leasing and Hongzhan Financial Leasing—provide medical institutions with the necessary capital for equipment procurement through methods such as “direct leasing” or “sale-leaseback” arrangements, with cumulative funding amounts reaching into the hundreds of millions of RMB. These financial institutions forge close collaborative ties with equipment manufacturers, establishing a synergistic mechanism wherein “manufacturers recommend equipment—financial institutions fund the purchase—medical institutions lease and utilize the equipment.” Furthermore, in an effort to expand market share and accelerate capital turnover, equipment manufacturers have begun establishing their own leasing platforms or engaging in deep-level cooperation with professional leasing firms; this strategy streamlines intermediate channels and enhances the overall efficiency of the value chain.

The core value of the upstream segment lies in lowering the financial entry threshold for medical institutions, thereby enabling high-end laser technologies to be integrated into clinical practice in a more flexible and accessible manner.

Midstream of the Value Chain: Rental service Providers and Business Model Innovation.

The midstream segment of the value chain constitutes the operational core of the rental service ecosystem. It is primarily composed of professional rental service providers responsible for a comprehensive range of functions, including equipment procurement, inventory management, client acquisition, equipment delivery, and full-lifecycle operation and maintenance support. In terms of business models, midstream service providers are continuously innovating the forms of their leasing products to meet the diverse needs of various healthcare institutions. Based on the specific leasing method employed, these offerings can be categorized into the following types:

**All-inclusive Leasing:** Service providers furnish a comprehensive suite of services—including equipment supply, installation, maintenance, consumables provision, and operational training. Healthcare institutions pay a fixed fee on a recurring basis; this model is ideal for institutions seeking a “turnkey” operational solution.

**Pay-per-Use Leasing:** This model is suitable for institutions with highly fluctuating surgical volumes or for specific diagnostic and treatment procedures. Healthcare institutions pay based on the actual number of times the equipment is utilized, incurring no costs when the equipment sits idle. It is particularly well-suited for settings such as medical aesthetics clinics and specialized outpatient centers.

**Long-term Financial Leasing:** Typically involving a lease term of 3 to 5 years, this arrangement offers the option to renew the lease or purchase the equipment at a reduced price upon expiration. Essentially serving as an alternative to installment-based purchasing, it is ideal for medium-to-large-scale institutions with stable, long-term equipment requirements.

**Short-term Temporary Leasing:** Designed to address temporary needs—such as during equipment maintenance periods or peak surgical seasons—this model offers lease terms calculated on a daily or weekly basis, thereby providing critical operational backup.

From the perspective of service content, the midstream sector of the industry value chain is evolving from a simple “equipment rental” model toward a comprehensive service paradigm encompassing “equipment + consumables + operations & maintenance + clinical support.” Leading service providers are enhancing customer loyalty and lifetime value by offering value-added services such as periodic calibration, rapid fault response, and regulatory compliance support. This transformation signifies that rental services are no longer merely a simple transfer of equipment usage rights, but rather professional solutions that encompass the entire equipment lifecycle management.

**Downstream Sector: End-User Applications and Demand Drivers**

The downstream sector of the industry value chain comprises the ultimate end-users of rental services—primarily various healthcare institutions and medical aesthetics providers. The specific structure of their demand and their prevailing development trends directly shape the overall trajectory of the entire industry chain.

Based on the types of end-users, the downstream market can be broadly categorized into three main segments:

**General Hospitals:** Large-scale public hospitals typically possess extensive in-house equipment inventories. Consequently, their demand for rental services primarily arises during transitional periods for equipment upgrades and replacements, during temporary departmental capacity expansions, or when piloting new medical programs. Surgical departments—such as Ophthalmology, Urology, and Obstetrics & Gynecology—represent the primary users of these rental services within this segment.

**Private Specialty Hospitals and Medical Aesthetics Institutions:** This segment represents the fastest-growing area for rental services, exhibiting the highest market penetration rates. Private healthcare institutions often operate with relatively limited capital budgets; however, they face an urgent need for advanced medical equipment. The leasing model enables these institutions to provide technical treatments on par with those offered by public hospitals, all while effectively managing their cash flow. Taking Gaochun People’s Hospital in Nanjing as an example: by utilizing a public bidding process to lease Intense Pulsed Light (IPL) and laser systems—specifically ultra-picosecond devices—under a three-year service term with annual contract renewals, the hospital demonstrates the growing acceptance among healthcare institutions of flexible equipment leasing models.

Outpatient Surgery Centers and Imaging Centers: These types of facilities are typically smaller in scale and operate with greater agility. The leasing model enables them to flexibly allocate equipment resources in direct response to patient volume, thereby preventing the underutilization of fixed assets.

In terms of application scenarios, the demand for medical laser leasing spans a wide array of specialized fields, including general surgery, aesthetic dermatology, ophthalmology, and dentistry. Among these, aesthetic dermatology lasers constitute the fastest-growing sub-segment, driven by the sustained surge in demand for “light aesthetics” (non-invasive cosmetic procedures); meanwhile, ophthalmology lasers maintain a steady demand, bolstered by the continuous increase in the volume of myopia correction and cataract surgeries.

Regarding regional demand structures: the North American and European markets are characterized by mature regulatory frameworks and clearly defined clinical specializations, where rental services tend to favor high-end surgical and ophthalmological lasers. Conversely, the Asia-Pacific region—benefiting from the expansion of healthcare service capacity and rising consumer spending on medical aesthetics—exhibits a demand profile that leans more toward lasers for dermatological and minimally invasive treatments; while this segment demonstrates faster growth, it is also subject to more intense price competition. These regional disparities significantly influence the strategic positioning and market approaches adopted by various industry participants.

Industry Chain Support Factors and Development Trends

The healthy functioning of the medical laser leasing industry chain relies on a confluence of supporting factors, while the sector as a whole is simultaneously exhibiting distinct evolutionary trends.

Regarding core growth drivers: the widespread adoption of minimally invasive surgery stands as the primary catalyst for the industry chain’s expansion. Minimally invasive procedures offer distinct advantages—such as faster recovery times, fewer complications, and shorter hospital stays—and have consequently emerged as the future trajectory of modern surgery; laser devices, in turn, serve as the indispensable core tools for executing these procedures.

Regarding core challenges: the substantial costs associated with equipment maintenance and calibration constitute the primary pressure point facing the industry chain. Laser devices require periodic calibration, preventive maintenance, and breakdown repairs performed by specialized technical personnel; service providers must shoulder the burden of managing equipment operations and maintenance across multiple geographic locations, a requirement that significantly inflates operational costs. Furthermore, the operation of these sophisticated devices necessitates specialized training, and a shortage of skilled personnel in certain regions currently constrains service delivery capabilities. Additionally, stringent regulatory frameworks governing the safety of medical devices keep compliance costs consistently high.

Regarding development trends: the industry chain is currently evolving toward greater scale, enhanced intelligence, and a stronger service-oriented focus. Leading leasing firms are expanding their market share through resource integration and capital operations; consequently, industry concentration is expected to rise gradually. Meanwhile, equipment manufacturers are establishing their own leasing platforms to compete directly in the market, thereby narrowing the scope for independent leasing providers. Furthermore, the synergistic effects between rental services, consumables, and data services are becoming increasingly prominent, fostering diversified profit models. In the long run, medical laser rental services are poised to become a pivotal pathway for the commercialization of high-value medical equipment, offering the potential for stable cash flows and scalable replication.

Overall, the medical laser leasing value chain is currently undergoing a critical transition—shifting from a “supplementary model” to a “mainstream configuration.” The synergy between upstream equipment manufacturing and capital supply, the continuous innovation in midstream service models, and the constant expansion of downstream application scenarios collectively form the foundation for the value chain’s robust growth. Looking ahead, driven by the rising adoption of minimally invasive surgeries and the ongoing trend of medical resource decentralization, this value chain is expected to maintain its steady growth trajectory.

The competitive landscape of the medical laser rental service sector is characterized by the following features:

From a segmented perspective, the high-end market is dominated by international medical equipment leasing companies. Leveraging their mature laser product lines, comprehensive maintenance service systems, and strong brand reputation, these firms provide holistic solutions—including equipment upgrades, operational training, and remote technical support—to large-scale hospitals and specialized medical institutions. The mid-range market is led by regional leasing providers and select medical device distributors; these entities cater to the needs of small-to-medium-sized hospitals and private clinics through competitive pricing, flexible lease terms, and localized services. The low-end market, conversely, is populated by a large number of small-scale leasing companies that primarily offer single-unit rentals or short-term usage services; competition in this segment centers mainly on price and accessibility, with relatively limited added value derived from technology and services.

From a regional perspective, the markets in North America and Europe exhibit high levels of concentration, with high-end service providers holding a significant market share. The Asia-Pacific region, while characterized by a large and fragmented pool of market participants, has recently witnessed local enterprises gradually bolstering their competitiveness within the mid-range market, driven by the increasing demand among medical institutions for greater equipment flexibility.

In summary, the medical laser rental service industry presents a competitive landscape characterized by “international brands dominating the high-end market, while regional enterprises and small-scale providers engage in fierce competition within the mid-to-low-end markets.” Moving forward, as the pace of laser technology innovation accelerates and leasing models become increasingly standardized, companies possessing strong technical service capabilities and offering comprehensive system solutions are expected to further expand their market share, thereby driving a gradual increase in overall industry concentration.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp