Laminate Bus Bar Market Summary

A Laminated Bus Bar (LBB) is a multilayer construction of conductors: copper or aluminum separated by thin dielectric materials, laminated in one structure. Electrically, it is a multilayer electrical circuit that distributes the electrical current from capacitors (buffer) to power modules (IGBT) through specific connections. Busbars are metal bars designed for carrying large amounts of current. Often made of copper or aluminum, every home electrical panel has busbars to distribute ac power to the rows of circuit breakers. Busbars are engineered for power distribution.

Laminated busbars can be defined as a multi-layer conductor structure (typically copper or aluminum) in which conductor layers are separated by insulating dielectrics and laminated/pressed into a single integrated assembly. In power-conversion modules (e.g., inverters and converters), the core value proposition versus conventional wiring is the ability to minimize stray inductance and associated over-voltage/EMI stresses, while improving packaging consistency and power-loop performance—hence its frequent positioning as a “super circuit board” for power units. Beyond standard laminated busbars, the market also includes higher-integration formats such as capacitor-integrated DC-link busbars, power+signal hybrid busbars, compact/3D high power-density designs, and higher-temperature or enhanced insulation variants; for market sizing, these remain in-scope as long as the product’s core architecture is laminated conductor layers with insulation serving power distribution/interconne.

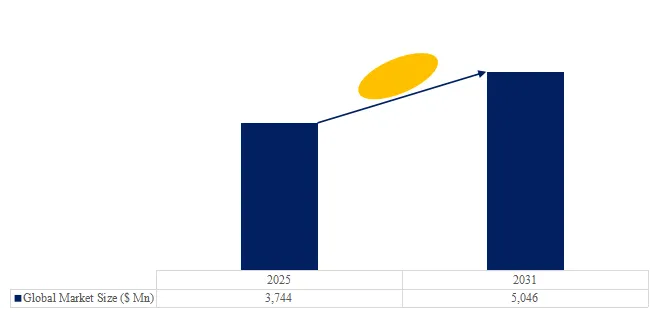

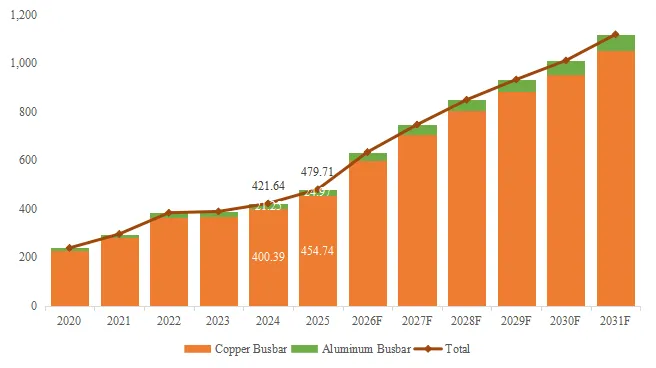

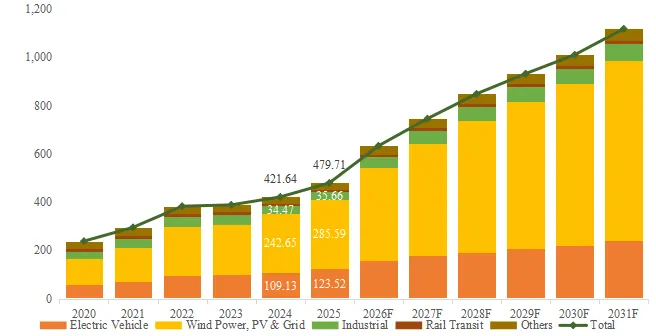

According to the new market research report “Global Laminate Bus Bar Market Report 2025-2031″, published by QYResearch, the global Laminate Bus Bar market size is projected to grow from USD 421.64 million in 2024 to USD 1118.79 million by 2031, at a CAGR of 15.16% during the forecast period.

Above data is based on report from QYResearch: Global Laminate Bus Bar Market Report 2025-2031 (published in 2025). If you need the latest data, plaese contact QYResearch.

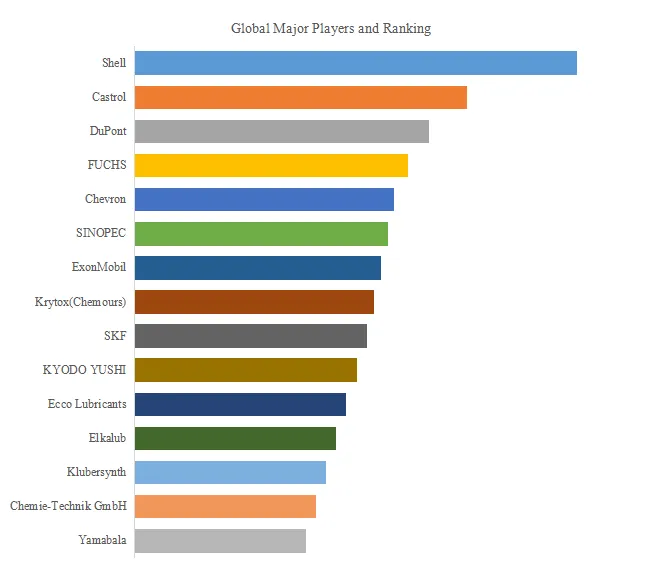

Figure00002. Global Laminate Bus Bar Top 18 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Laminate Bus Bar Market Report 2025-2031 (published in 2024). If you need the latest data, plaese contact QYResearch.

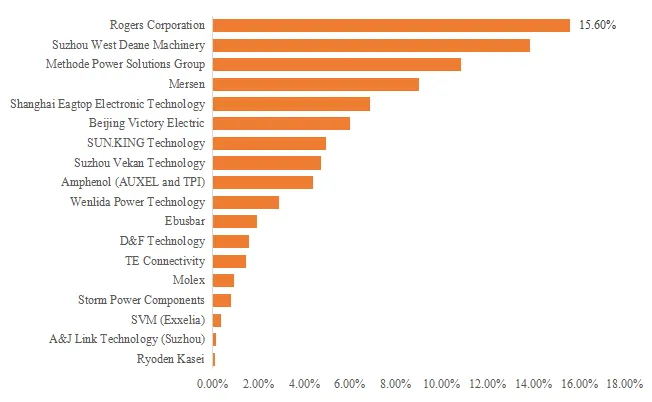

Globally, major manufacturers of laminated bus bars include Rogers, Suzhou West Deane Machinery, Methode Power Solutions Group, Mersen, and Shanghai Yingfeng Electronics Technology, with the top five manufacturers holding approximately 56% of the market share.

Currently, the core manufacturers globally are mainly located in Europe, America, and China.

Figure00003. Laminate Bus Bar, Global Market Size, Split by Product Segment

Based on or includes research from QYResearch: Global Laminate Bus Bar Market Report 2025-2031.

In terms of product type, laminate bus bar are currently the most important sub-product, accounting for approximately 95% of the market share.

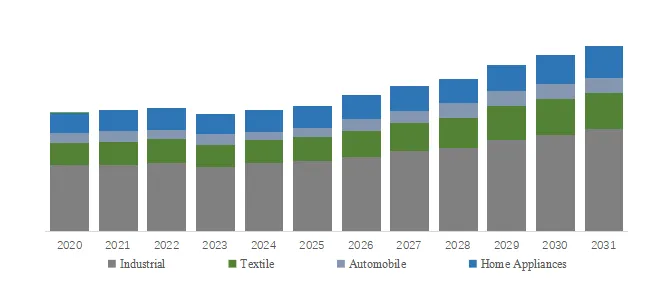

Figure00004. Laminate Bus Bar, Global Market Size, Split by Application Segment

Based on or includes research from QYResearch: Global Laminate Bus Bar Market Report 2025-2031.

In terms of product application, Wind Power, PV & Grid is the largest application, hold a share of 60%.

Laminate Bus Bar Supply Chain Analysis:

Upstream: Primarily includes copper foil or aluminum busbars, insulating materials (such as PET, PI, and epoxy films), thermally conductive/flame-retardant auxiliary materials, and surface treatment materials. Fluctuations in copper and aluminum prices significantly impact costs.

Midstream: Companies produce products through processes such as punching, lamination, bending, riveting/welding, insulation encapsulation, and testing. Core competitiveness lies in electrical design, thermal management, dimensional accuracy, batch consistency, and rapid customization delivery capabilities.

Downstream: Widely used in new energy vehicles, electric drives, electronic controls, charging piles, photovoltaic inverters, energy storage systems, rail transit, and industrial converter equipment. Customers typically have stringent certification requirements and long adoption cycles. Overall, the laminated busbar supply chain is characterized by material cost sensitivity, high technological and process barriers, and strong ties to leading downstream customers. Future upgrades will focus on high-voltage platforms, lightweight design, high integration, and high reliability.

Development Trends in the Laminated Bus Bar Industry:

1. The global laminated busbar market sales are projected to grow from US$421 million in 2024 to US$1.118 billion in 2031, representing a CAGR of 15.16% from 2025 to 2031. In terms of application structure, wind, solar, energy storage, and grid technologies accounted for 57.55% of revenue in 2024, and are expected to further increase to 66.79% by 2031; the corresponding revenue scale will increase from US$388 million in 2026 to US$747 million in 2031. In contrast, new energy vehicles remain an important application direction, but their global revenue share will generally remain at just over 20% during the forecast period, indicating that future industry growth will be more significantly tilted towards energy storage, grid upgrades, and new energy power generation. From a trend perspective, the laminated busbar industry will continue to benefit from the expansion of new energy power electronic systems, but the main growth driver will be the continued expansion of high-power, high-reliability applications.

2. In 2024, China accounted for 89.47% of global laminated busbar production, and this figure is projected to rise further to 92.13% by 2031, indicating continued supply concentration. However, in terms of revenue, China’s share of the global market is expected to decline from 58.50% in 2026 to 53.07% in 2031, while Europe’s share is projected to rise from 19.72% to 22.27%, and North America’s from 12.16% to 13.96% during the same period. This suggests that the industry will not see a significant shift in supply focus overseas in the coming years, with China remaining the world’s core manufacturing and supporting center. However, with increasing demand for new energy equipment, power infrastructure, and localized supporting products overseas, consumption will exhibit a more pronounced multi-regional distribution. In other words, the industry’s regional evolution is more likely to be characterized by “continued manufacturing concentration and gradual expansion of demand,” rather than a simple global equalization of production capacity.

3. From a product type perspective, the revenue share of laminated copper busbars is projected to remain at 94.07% by 2031, indicating that copper-based solutions will remain the dominant approach in current mainstream applications, and no fundamental replacement is expected in the short term. Meanwhile, material and structural optimization has become a clearly stated direction in publicly disclosed information. Beijing Vitonli explicitly stated in its prospectus that electrical connection products are showing a trend towards integration, lightweighting, and intelligence, and proposed exploring the application of insulating materials and composite conductive metal materials in electrical connection products. Xidian New Energy’s prospectus also disclosed that the company applies composite busbar hot-pressing technology to battery connection systems, driving product development towards lightweighting and integration. In summary, the industry is more likely to exhibit an evolutionary characteristic of “stable copper-based main route and parallel material optimization,” meaning the mainstream market will still be based on high-reliability copper-based solutions, while continuous marginal optimization at the structural and material levels will focus on weight reduction, cost reduction, and integration.

4. In 2024, the top five manufacturers globally accounted for 56.09% of revenue, while the top five manufacturers in the Chinese market accounted for 60.36%, indicating a continuous increase in industry concentration. Meanwhile, publicly disclosed information from leading companies suggests that competitive factors are shifting from single busbar manufacturing to stronger system adaptation and manufacturing collaboration capabilities. Shanghai Yingfeng Electronics disclosed in its audit response that its capacitor busbars adopt a stacked busbar structure design to reduce parasitic inductance, improve current sharing performance, and meet the high-frequency requirements of the 800V high-voltage architecture for new energy vehicles. The same company also disclosed that it has developed a multi-functional integrated stacked busbar that integrates low-cost indicator lights and signal transmission functions, and deployed PLM, MES, QMS, ERP, and other information systems. Xidian New Energy disclosed that its battery connection system production line was designed and built in-house. Therefore, the competitive advantage of leading companies in the future will be more reflected in the comprehensive combination of system-level design capabilities, customized development efficiency, process equipment capabilities, and intelligent manufacturing capabilities. The industry competition logic will gradually shift from “making products” to “stable delivery of solutions.”

Key Drivers of the Laminated Bus Bar Industry:

1. The global laminated busbar market sales are projected to grow from $421 million in 2024 to $1.118 billion in 2031, representing a CAGR of 15.16% from 2025 to 2031. In terms of application structure, wind, solar, energy storage, and the power grid are currently the largest downstream sectors, accounting for 57.55% of revenue in 2024 and projected to rise to 66.79% by 2031. While new energy vehicles account for a smaller share than wind, solar, energy storage, and the power grid, they remain the second largest application area, accounting for 25.88% of revenue in 2024. This structure indicates that the core demand for laminated busbars has shifted from traditional industrial power distribution connections to power connection needs in new energy generation, energy storage, power grid upgrades, and electrification. Downstream installed capacity expansion and increased system power density directly drive the synchronous growth of laminated busbar demand.

2. From the production side, China accounted for 89.47% of global laminated busbar production in 2024, and this figure is projected to further increase to 92.13% by 2031. From the consumption side, the Chinese market reached $250 million in 2024, accounting for 59.2% of the global market, and is expected to maintain a global share of around 53% by 2031. These figures reflect that China is not only the world’s largest demand market for laminated busbars but also its core manufacturing and supporting center. For the industry, a complete domestic supply chain, short delivery radius, and high customer collaboration efficiency enable laminated busbars to be more quickly integrated into the iterative development of downstream products such as new energy vehicles, energy storage systems, inverters, and power equipment. This industrial chain agglomeration effect is itself a significant driver of the industry’s continued expansion.

3. Revenue from laminated busbars used in wind, solar, energy storage, and grid applications is projected to grow from $388 million in 2026 to $747 million in 2031, maintaining the fastest growth rate during the forecast period and further increasing its share of total revenue from 57.55% in 2024 to 66.79% in 2031. This change indicates that future industry growth will not solely rely on the electrification of passenger vehicles, but will benefit more from the expanding demand for energy storage converters, photovoltaic inverters, wind power converters, and grid power electronics equipment. Compared to traditional industrial scenarios, these new energy power electronics scenarios typically place higher demands on current carrying capacity, thermal management, low inductance, and spatial integration. Therefore, while demand expands, it also simultaneously increases the value of laminated busbars and their individual unit value, constituting a significant driver of the industry’s medium- to long-term growth.

4. Laminated copper busbars are still expected to account for 94.07% of global revenue by 2031, indicating that the mainstream market will still be dominated by high-reliability copper-based solutions. At the same time, industry growth is not only driven by quantitative expansion but also by increased product value. Based on publicly disclosed information from representative companies, leading manufacturers such as Xidian New Energy, Shanghai Yingfeng Electronics, and Beijing Weitongli have all been promoting customized product development for scenarios such as new energy vehicles, energy storage, and power grids, emphasizing low inductance, high reliability, integration, and lightweight design. This indicates that as downstream systems evolve towards high-voltage platforms, higher power densities, and greater integration, laminated busbars are no longer just traditional conductive connectors, but are gradually becoming key components affecting electrical performance, spatial layout, and system reliability. This upward shift in product functional boundaries is becoming a significant driver of continued industry demand and value enhancement for leading companies.

5. In 2024, the top five global manufacturers held a 56.09% market share, while the top five Chinese manufacturers held a 60.36% market share, indicating a relatively high level of industry concentration. This pattern suggests that downstream mainstream customers are increasingly prioritizing continuous supply capabilities, collaborative development capabilities, and stable batch delivery when selecting laminated busbar suppliers, rather than simply comparing prices. As downstream customers in sectors such as new energy vehicles, wind, solar, and energy storage, as well as power grid equipment, place increasing demands on verification cycles, quality consistency, and project delivery schedules, industry orders are gradually concentrating on leading companies with capabilities in R&D, manufacturing, verification, and customer collaboration. For the industry as a whole, this deepening trend of “leading customers – leading suppliers” helps drive market expansion, improve technical standards, and increase product penetration, serving as a crucial endogenous driving force for the industry’s continued growth.

About The Authors

Meng Yu Lead Author

Email: yumeng@qyresearch.com

QYResearch Nanning Research Center analyst, main research areas include semiconductors, chemical materials, electronics and other fields, some of the sub-research topics include Motor for semiconductor equipment, air bearing stage, low CTE ceramic material, high purity oleic acid, camera soc, intelligent energy management system, etc., also engaged in market segment report development, and participate in the writing of customized projects.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp