Introduction: Addressing DC Component Measurement, High-Precision Current Sensing, and Wide Bandwidth Pain Points

For power electronics engineers, renewable energy system designers, and traction system integrators, accurate current measurement has long faced a fundamental challenge: traditional current transformers (CTs) cannot measure DC components (saturate core), open-loop Hall sensors drift with temperature (2–5% accuracy), and shunt resistors lack galvanic isolation (safety risk). In applications like wind power converters (DC-AC inverter output contains DC offset), rail transit traction drives (regenerative braking DC current), and battery test systems (DC charging/discharging), measuring mixed AC+DC currents with high precision (0.1–0.5%) is critical for control performance and safety. The result: system inefficiencies (uncompensated DC offset saturates transformers), inaccurate state-of-charge (SoC) calculations for batteries, and protection misoperations (DC fault detection failures). Global Leading Market Research Publisher QYResearch announces the release of its latest report “Closed Loop Current Transformer – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Closed Loop Current Transformer market, including market size, share, demand, industry development status, and forecasts for the next few years.

For power converter manufacturers, traction drive OEMs, and renewable energy developers, the core pain points include achieving 0.1% accuracy across DC to 100kHz bandwidth (AC+DC mixed current measurement), ensuring DC immunity (no core saturation from DC offset), and providing galvanic isolation (safety for high-voltage systems up to 10kV). Closed loop current transformers address these challenges as high-precision current measurement devices based on the zero-flux compensation principle—using built-in electronics to detect and compensate core flux in real-time, ensuring accurate proportional current output. Comprising a magnetic modulator, compensation winding, and integrator amplifier, these devices achieve 0.1% accuracy, wide bandwidth (DC-100kHz), and DC immunity, making them widely used in renewable energy, traction systems, battery test equipment, and other dynamic current measurement applications.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6096450/closed-loop-current-transformer

Market Sizing and Recent Trajectory (Q1–Q2 2026 Update)

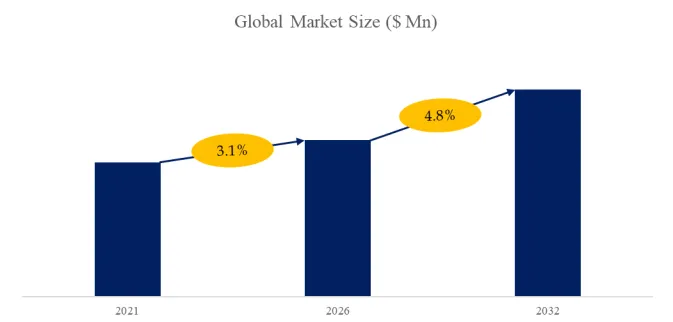

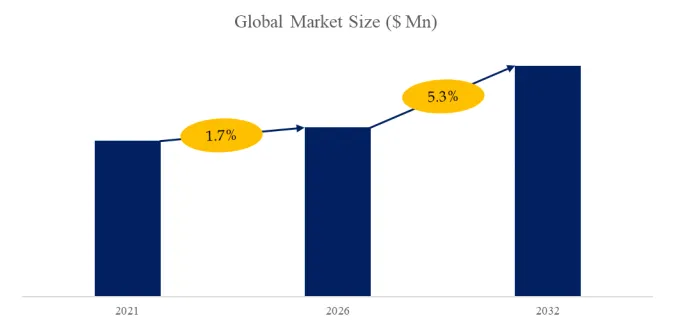

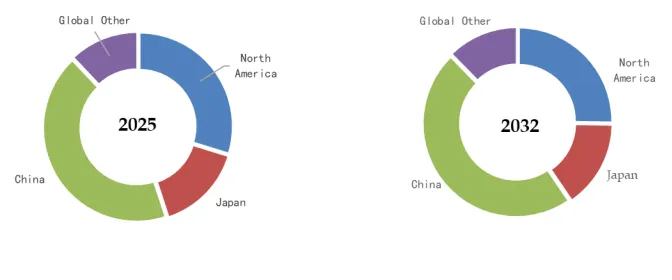

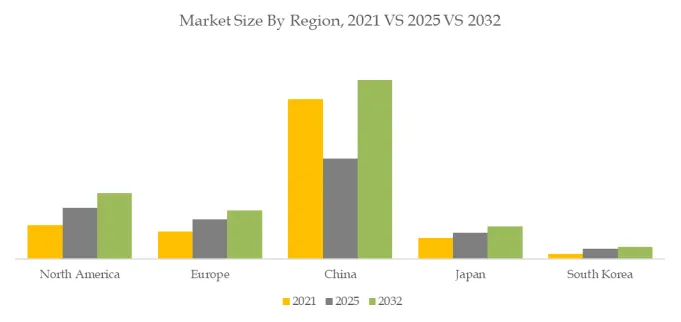

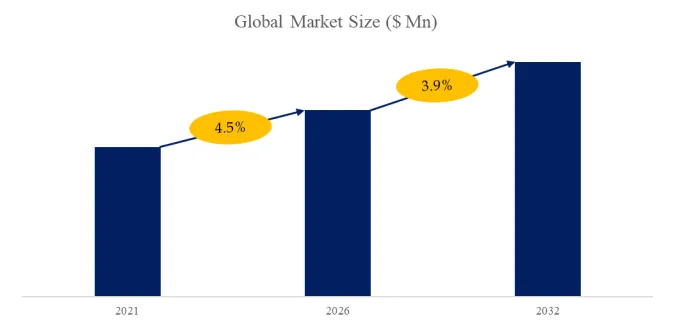

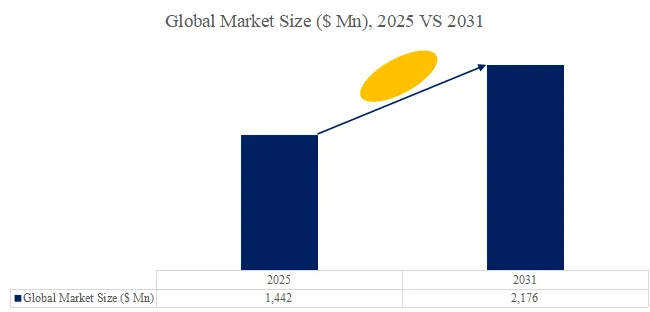

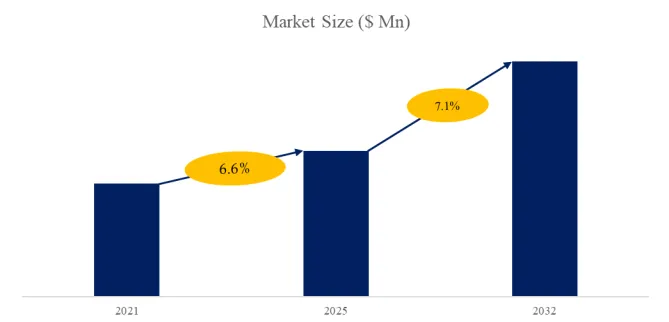

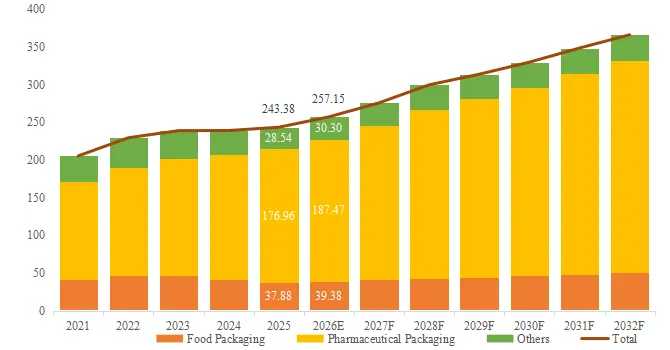

The global market for Closed Loop Current Transformer was estimated to be worth US$ 263 million in 2025 and is projected to reach US$ 383 million, growing at a CAGR of 5.6% from 2026 to 2032. In 2024, global production reached approximately 1,243 k units, with an average global market price of around US$ 200 per unit. Preliminary data for the first half of 2026 indicates accelerating demand in wind power (global wind installations +15% in 2025), rail transit (urban rail expansion in China, India, Europe), and semiconductor equipment (precision power supplies for wafer fabrication). The 500-2000A segment dominates (48% of revenue, fastest-growing at CAGR 6.5%) for wind power converters (2–5MW turbines), traction drives (subway, light rail), and industrial motor drives. The 0-500A segment (32% of revenue, CAGR 4.8%) serves battery test equipment, EV chargers, and smaller converters. The above 2000A segment (20% of revenue, CAGR 5.2%) serves high-power wind turbines (>6MW), electrolysis plants, and large industrial drives. The wind power application segment leads (40% of revenue), followed by rail transit (30%), semiconductors (15%), and others (15%).

Product Mechanism: Zero-Flux Compensation, Magnetic Modulator, and Wide Bandwidth

A Closed Loop Current Transformer (CT) is a high-precision current measurement device based on zero-flux compensation principle. It utilizes built-in electronics to detect and compensate core flux in real-time, ensuring accurate proportional current output. Comprising magnetic modulator, compensation winding, and integrator amplifier, it achieves 0.1% accuracy, wide bandwidth (DC-100kHz), and DC immunity, widely used in renewable energy, traction systems, and other dynamic current measurement applications.

A critical technical differentiator is current range, bandwidth, and accuracy class:

- Operating Principle – Zero-flux (closed loop) compensation: primary current (I_p) generates magnetic flux in core. Secondary compensation winding drives current (I_s) through integrator amplifier to cancel core flux (null detector). Output voltage V_out = I_s × R_m (burden resistor). I_s ∝ I_p (turns ratio). Advantages: DC measurement capability (no core saturation), high accuracy (0.1–0.5%), wide bandwidth (DC-100kHz or higher), low temperature drift (50 ppm/°C). Disadvantages: higher cost (2–5× open-loop Hall), requires power supply (±15V or 24V), more complex electronics.

- Current Range Segmentation – 0-500A: battery test, EV chargers, small inverters. 500-2000A: wind converters (2–5MW), rail traction drives, industrial motor drives. Above 2000A: large wind turbines (>6MW), electrolysis, large industrial drives.

- Accuracy vs. Open-Loop Hall – Closed loop CT: 0.1–0.5% accuracy, ±10–50ppm/°C drift. Open-loop Hall: 1–3% accuracy, ±100–300ppm/°C drift. Closed loop required for precision applications (battery test, metering, protection).

- Bandwidth – DC-100kHz (standard), DC-500kHz (high-speed models). Enables measurement of harmonics up to 100th order (2kHz for 50Hz systems, 10kHz for 400Hz aircraft systems).

Recent technical benchmark (March 2026): LEM’s ITZ series (closed loop CT, 500A, 0.1% accuracy, DC-500kHz, $350) achieved 50ppm/°C drift, 5kV isolation, and -40°C to +85°C operation. Independent testing (IEEE Power Electronics) confirmed 0.05% linearity error over 0–500A range.

Real-World Case Studies: Wind Power, Rail Transit, and Semiconductor Equipment

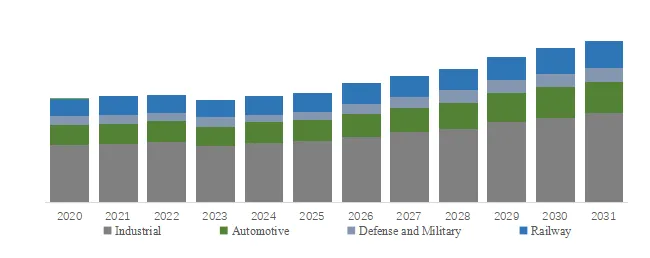

The Closed Loop Current Transformer market is segmented as below by current rating and application:

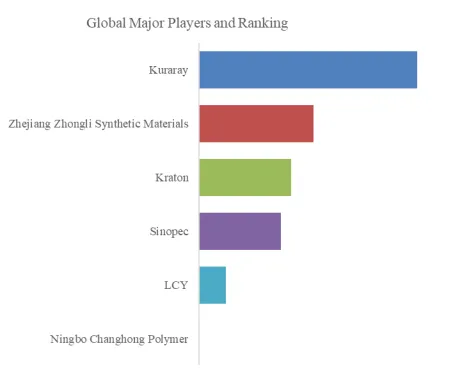

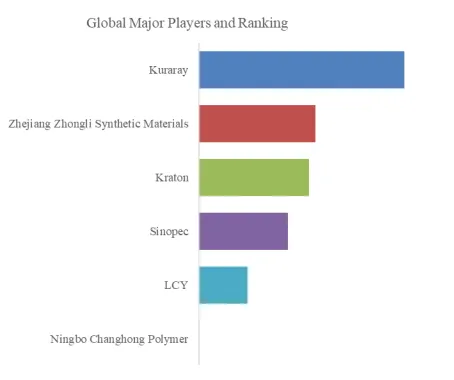

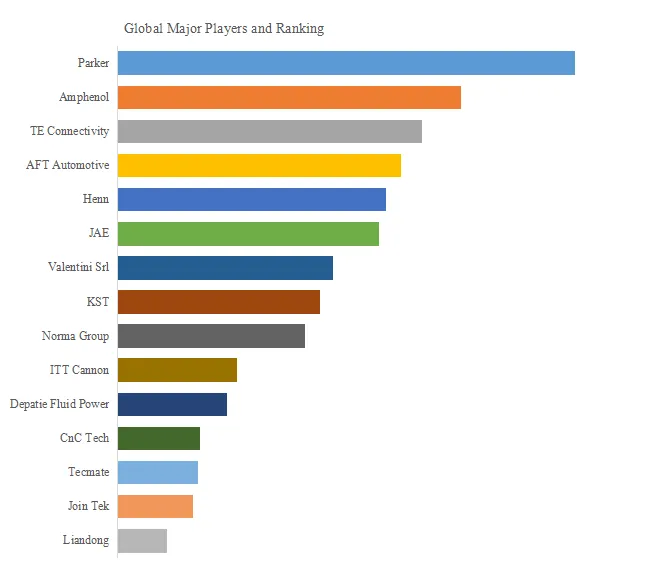

Key Players (Selected):

Schneider Electric, LEM, ABB, Honeywell, Vacuumschmelze, Yokogawa, Hubei Tianrui Electronic

Segment by Type (Current Range):

- 0-500A – Battery test, EV chargers. 32% of revenue (CAGR 4.8%).

- 500-2000A – Wind power, rail transit. 48% of revenue (CAGR 6.5%).

- Above 2000A – Large wind, electrolysis. 20% of revenue (CAGR 5.2%).

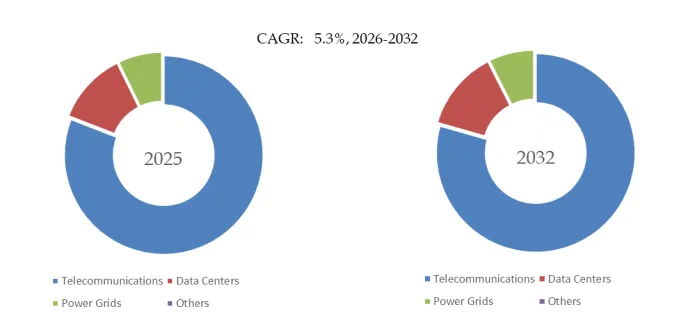

Segment by Application:

- Wind Power – Converter output current monitoring. 40% of revenue.

- Rail Transit – Traction drive current measurement. 30% of revenue.

- Semiconductors – Precision power supplies for wafer fab. 15% of revenue.

- Others – Battery test, EV charging, industrial drives. 15% of revenue.

Case Study 1 (Wind Power – 5MW Turbine Converter): Siemens Gamesa 5MW wind turbine uses LEM closed loop CTs (ITZ 1000-S, 1000A, 0.1% accuracy) for converter output current measurement (AC+DC offset from inverter). Requirements: measure DC offset (grid protection), 0.1% accuracy for power quality (IEC 61400-21), and DC-100kHz bandwidth (capture switching harmonics). Turbine uses 6 CTs (3-phase × 2 converters) → $2,100 per turbine. Global wind installations 100GW in 2025 → 20,000 turbines (5MW) → 120,000 CTs ($24M). Wind power segment (40% of revenue) growing 8% CAGR.

Case Study 2 (Rail Transit – Subway Traction Drive): CRRC (China Railway Rolling Stock) subway train uses ABB closed loop CTs (2000A, 0.5% accuracy) for traction inverter output current measurement. Requirements: DC current measurement (regenerative braking), high vibration tolerance (rail environment), and -25°C to +85°C operation. Train uses 4 CTs (per motor car). CRRC delivered 5,000 subway cars in 2025 → 20,000 CTs ($4M). Rail transit segment (30% of revenue) growing 6% CAGR.

Case Study 3 (Semiconductors – Wafer Fab Power Supply): Applied Materials wafer fabrication power supply (plasma etch, CVD) uses Yokogawa closed loop CTs (100A, 0.1% accuracy, DC-1MHz bandwidth). Requirements: measure DC current (plasma control), high bandwidth (capture fast transients), and low drift (process repeatability). Power supply uses 3 CTs. Applied Materials sold 1,000 power supplies in 2025 → 3,000 CTs ($600,000). Semiconductor segment (15% of revenue) growing 10% CAGR.

Case Study 4 (Battery Test – EV Battery Cyclers): Chroma battery test system (EV battery cycler, 800V, 600A) uses closed loop CTs (600A, 0.1% accuracy) for charge/discharge current measurement. Requirements: DC accuracy (0.1% for SoC calculation), low drift (test repeatability), and galvanic isolation (safety). Battery cycler uses 2 CTs (charge + discharge). Chroma sold 5,000 cycler channels in 2025 → 10,000 CTs ($2M). Battery test segment (subset of others, 15%) growing 12% CAGR.

Industry Segmentation: By Current Range and Application

From an operational standpoint, 500-2000A segment (48% of revenue, fastest-growing) dominates wind power and rail transit—the largest volume applications. 0-500A segment (32% of revenue) dominates semiconductor equipment, battery test, and EV chargers. Above 2000A segment (20%) serves large wind turbines (>6MW) and electrolysis (green hydrogen). Wind power (40% of revenue) largest segment, driven by global wind installations (100GW+ annually). Rail transit (30%) second largest, driven by urban rail expansion (China, India, Europe). Semiconductors (15%) fastest-growing (10% CAGR), driven by wafer fab expansion (US CHIPS Act, EU Chips Act).

Technical Challenges and Recent Policy Developments

Despite strong growth, the industry faces four key technical hurdles:

- High-frequency bandwidth vs. power consumption: High bandwidth (500kHz–1MHz) requires high-drive op-amps, increasing power consumption (5–10W per CT). Solution: low-power precision op-amps (3–5W) and switched-capacitor integrators.

- Core saturation from large DC offset: Zero-flux principle compensates up to rated DC offset (±100% of rated current). Beyond rated offset, core saturates. Solution: larger core (higher saturation flux) or dual-range CTs (switched compensation range).

- Temperature drift of magnetic modulator: Modulator sensitivity drifts ±100ppm/°C, affecting low-current accuracy. Solution: digital compensation (temperature sensor + lookup table) reduces drift to ±20ppm/°C.

- Calibration and traceability: Closed loop CTs require factory calibration (0.1% accuracy traceable to national standards). Calibration cost $20–50 per unit, significant for low-cost (<$100) CTs. Policy update (March 2026): IEC 61869-6 (Low-Power Instrument Transformers) updated to include closed loop CT calibration requirements for grid-tied renewable energy (0.5% accuracy mandatory for power quality compliance).

独家观察: DC-Immune CTs Enabling Renewable Energy Grid Integration

An original observation from this analysis is closed loop CTs enabling renewable energy grid integration by measuring DC offset in inverter output. Wind and solar inverters can inject DC current into the grid (due to switching asymmetry, component mismatch). Grid codes (IEEE 1547, IEC 61727) limit DC injection to <0.5% of rated current (e.g., 2.5A for 500A inverter). Traditional CTs cannot measure DC offset (core saturates). Closed loop CTs measure DC offset with 0.1% accuracy, enabling inverter control to cancel DC injection. All grid-tied wind and solar inverters (>100GW annually) require closed loop CTs for DC offset monitoring. Renewable energy segment driving 65% of closed loop CT demand.

Additionally, wide-bandgap semiconductors (SiC, GaN) driving higher bandwidth requirements. SiC inverters switch at 50–200kHz (vs. 5–20kHz for IGBT). Harmonics extend to 1MHz. Closed loop CTs must have bandwidth DC-500kHz to measure current waveform for control. LEM, Yokogawa offer 1MHz bandwidth CTs (20–30% premium). SiC adoption increasing from 15% of inverters (2025) to 40% (2030). Looking toward 2032, the market will likely bifurcate into standard closed loop CTs (DC-100kHz, 0.5% accuracy) for IGBT-based wind, rail, and industrial drives (cost-driven, 4–5% annual growth) and high-bandwidth closed loop CTs (DC-500kHz, 0.1% accuracy) for SiC-based renewable energy, battery test, and semiconductor equipment (performance-driven, 8–10% annual growth).

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp