Introduction: Addressing Bifacial Module Rear-Side Protection, UV Aging, and Harsh Environment Durability Pain Points

For solar module manufacturers, project developers, and EPC contractors, the transition to bifacial photovoltaic (PV) modules (front and rear sides generate power) has created a critical material challenge. Traditional backsheets (single-sided fluorine coating) protect only the module front; the rear side (now exposed to sunlight, reflected albedo radiation) uses cheaper, less durable materials (polyester, PET alone) that degrade rapidly under UV exposure (yellowing, cracking, delamination within 5–7 years). In bifacial modules, rear-side degradation directly reduces energy yield (5–15% loss over 25-year lifespan) and increases warranty claims (module replacement $200–500 per unit). For projects in extreme environments—deserts (high UV, sand abrasion), floating PV (humidity, water exposure), and agrivoltaics (chemicals, mechanical stress)—standard backsheets fail within 3–5 years. The result: developers face higher LCOE (levelized cost of energy), unexpected replacement costs, and missed production targets. Global Leading Market Research Publisher QYResearch announces the release of its latest report “Solar Double-Sided Fluorine Backsheet – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Solar Double-Sided Fluorine Backsheet market, including market size, share, demand, industry development status, and forecasts for the next few years.

For PV module manufacturers (Longi, JinkoSolar, Trina, JA Solar), backsheet suppliers, and project developers, the core pain points include achieving 25-year UV resistance (both front and rear sides), maintaining high reflectivity (rear-side albedo gain 5–30%), and withstanding harsh environments (desert sand, floating humidity, agricultural chemicals). Solar double-sided fluorine backsheet addresses these challenges as a high-end protective material specifically designed for high-efficiency bifacial PV modules—a composite backsheet composed of a weather-resistant polymer base film (typically PET) coated on both sides with fluorine resin (PVDF, PVF, or FEVE). This symmetrical design ensures identical protection for both front and back sides, particularly the rear side, to withstand harsh environmental challenges of rear-side power generation. As bifacial module market share exceeds 50% of new installations (2025) and projects expand into deserts (Gobi, Sahara), floating PV (China, Southeast Asia), and agrivoltaics (Europe, Japan), double-sided fluorine backsheets are becoming the standard for high-durability applications.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6096821/solar-double-sided-fluorine-backsheet

Market Sizing and Recent Trajectory (Q1–Q2 2026 Update)

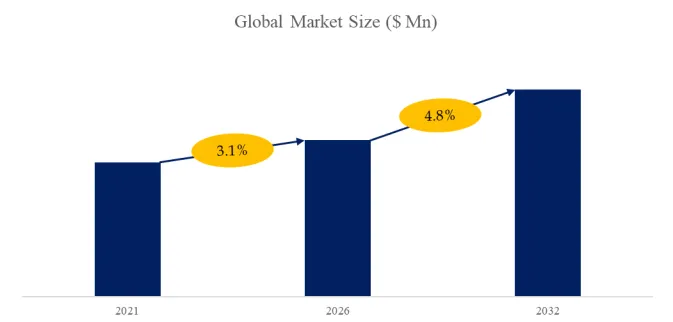

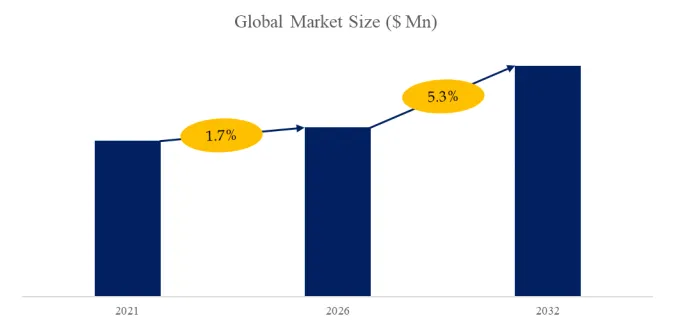

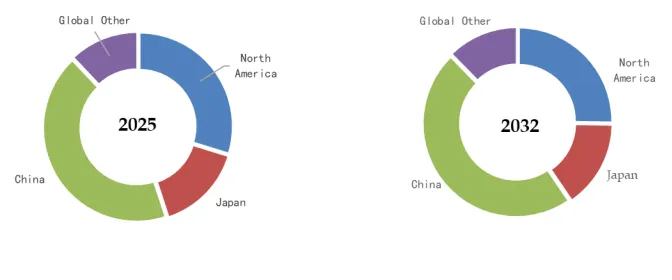

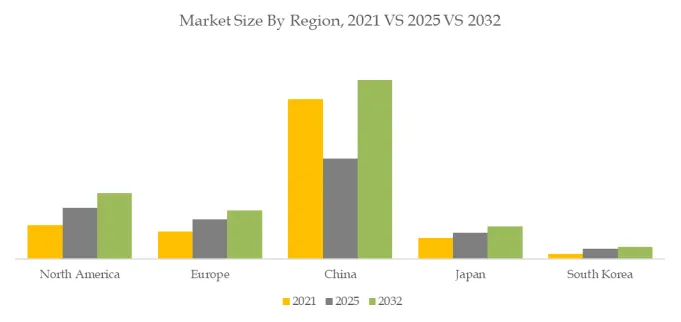

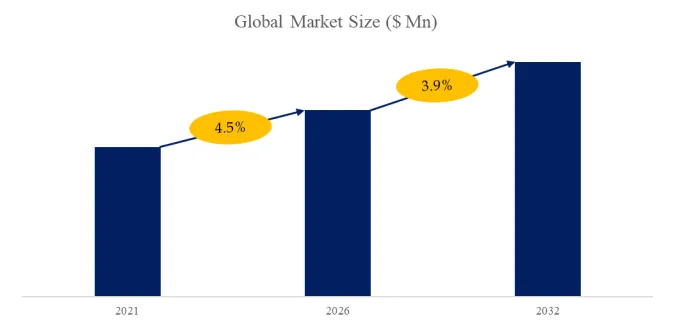

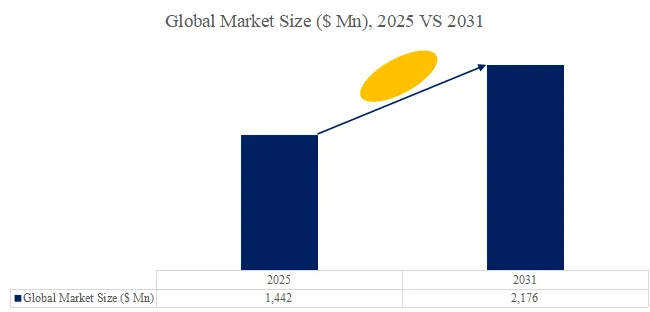

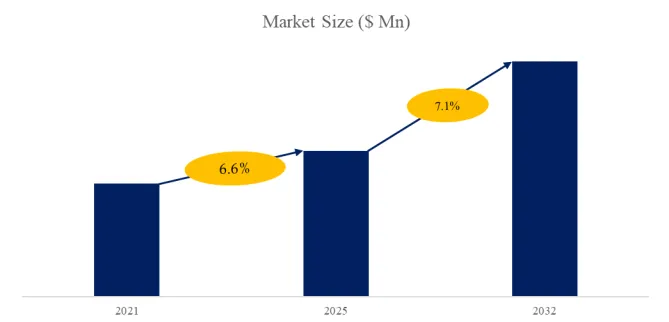

The global market for Solar Double-Sided Fluorine Backsheet was estimated to be worth US$ 834 million in 2025 and is projected to reach US$ 1,583 million, growing at a CAGR of 9.7% from 2026 to 2032. Global production reached 90.61 million square meters in 2024, with an average selling price of US$ 9.62 per square meter. Preliminary data for the first half of 2026 indicates accelerating demand in large-scale ground-mounted power plants (China, India, Middle East, US) and floating PV (China, Southeast Asia, Europe). The double-sided PVDF (polyvinylidene fluoride) coating segment dominates (65% of revenue, fastest-growing at CAGR 10.5%) due to superior UV resistance (25+ years), chemical stability, and cost-effectiveness. The double-sided PVF (polyvinyl fluoride) coating segment (20% of revenue, CAGR 8.2%) offers longer track record (Tedlar, DuPont legacy). The based on other fluorine alloys (FEVE) segment (15% of revenue, CAGR 9.5%) provides higher transparency for certain bifacial designs. The large-scale ground-mounted power plant application segment leads (60% of revenue), followed by floating photovoltaic (20%, fastest-growing at CAGR 14.5%), agriculture and livestock photovoltaic (12%), and others (8%).

Product Mechanism: PVDF vs. PVF vs. FEVE, UV Resistance, and Reflectivity

Solar double-sided fluorine backsheet is a high-end protective material designed specifically for high-efficiency bifacial photovoltaic modules. It is a composite backsheet composed of a weather-resistant polymer base film (usually PET) coated on both sides with a fluorine resin (such as PVDF, PVF, or FEVE). This symmetrical design ensures the same level of protection for both the front and back sides of the module, particularly the back side, to withstand the harsh environmental challenges of rear-side power generation. It is suitable for diverse applications requiring extremely high rear-side weather resistance, such as deserts, water surfaces, high altitudes, and agricultural greenhouses, including large-scale ground-mounted power stations, floating photovoltaics, agricultural photovoltaics, and livestock photovoltaics.

A critical technical differentiator is fluorine coating type, UV resistance (hours to 50% gloss retention), and reflectivity:

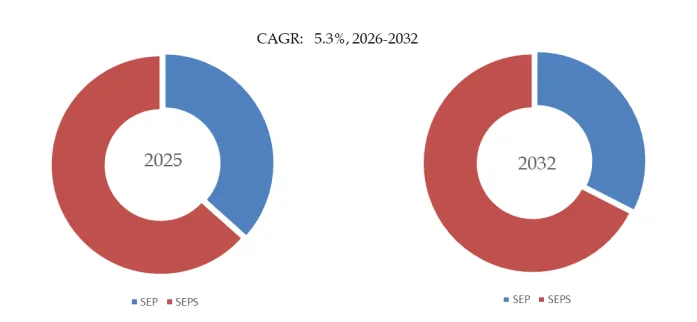

- Double-sided PVDF (Polyvinylidene Fluoride) Coating – Most common for high-efficiency bifacial. Advantages: excellent UV resistance (25+ years, 300kWh/m² UV exposure), high chemical resistance (acids, bases, salt spray), good abrasion resistance (sand), cost-effective ($8–12/m²). Disadvantages: requires primer layer (adhesion to PET), lower reflectivity (70–80% vs. 90% for white PVF). Applications: desert, ground-mounted, floating PV. Market share: 65% of revenue (fastest-growing, CAGR 10.5%).

- Double-sided PVF (Polyvinyl Fluoride) Coating – Tedlar legacy material (DuPont). Advantages: longest track record (30+ years field experience), high reflectivity (90% for white), excellent UV resistance (25+ years). Disadvantages: higher cost ($12–18/m²), limited to white color (colored PVF less common). Applications: premium bifacial modules, high-reflectivity applications. Market share: 20% of revenue (CAGR 8.2%).

- Based on Other Fluorine Alloys (FEVE – Fluoroethylene Vinyl Ether) – Emerging alternative. Advantages: excellent weatherability (25+ years), higher transparency (for certain bifacial designs), good adhesion to PET (no primer needed). Disadvantages: higher cost ($15–25/m²), less field history. Applications: specialty bifacial (high-transparency requirements). Market share: 15% of revenue (CAGR 9.5%).

- Key Performance Metrics – UV resistance: >300kWh/m² (25+ years) for PVDF/PVF, vs. <100kWh/m² for PET-only backsheets (5–7 years). Water vapor transmission rate (WVTR): <1g/m²/day for PVDF/PVF vs. 3–5g/m²/day for PET. Dielectric strength: >20kV for fluorine-coated vs. <15kV for PET.

Recent technical benchmark (March 2026): Cybrid Technologies’ double-sided PVDF backsheet (350μm total thickness, 25μm PVDF each side) achieved 350kWh/m² UV resistance (30-year equivalent), 85% reflectivity (white), and 0.8g/m²/day WVTR. Price: $10.50/m². Independent testing (TÜV Rheinland) confirmed 25-year warranty qualification.

Real-World Case Studies: Desert Ground-Mount, Floating PV, and Agrivoltaics

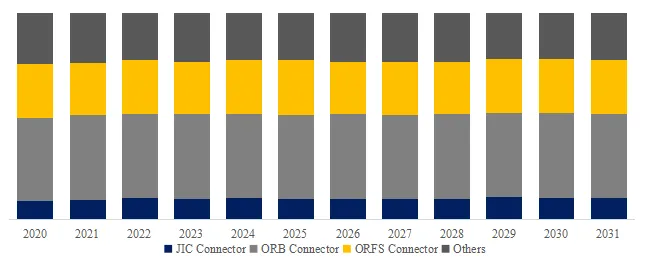

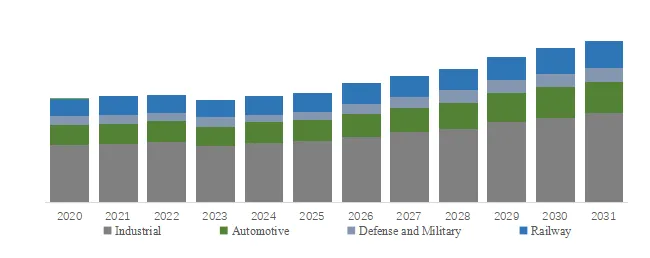

The Solar Double-Sided Fluorine Backsheet market is segmented as below by coating type and application:

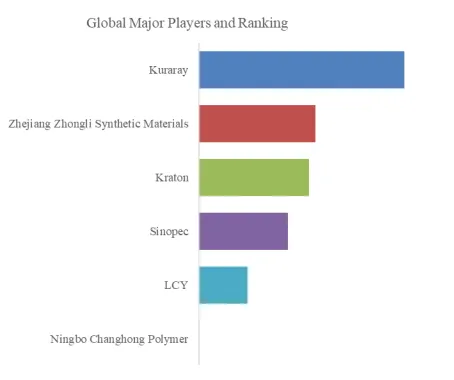

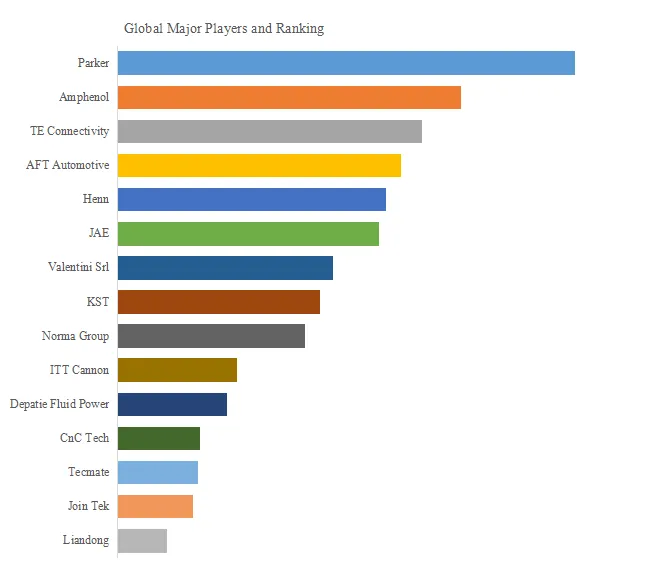

Key Players (Selected):

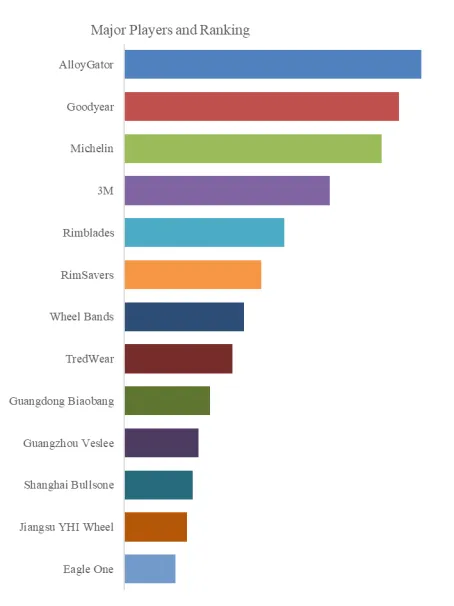

Toppan, Taiflex Scientific, Fujifilm Holdings Corporation, Cybrid Technologies, Lucky Film Co., Ltd., Ningbo Zhongyi New Energy, Hubei Huitian New Materials, Jolywood (Suzhou) Sunwatt, Crown Advanced Material, Hangzhou First Applied Material

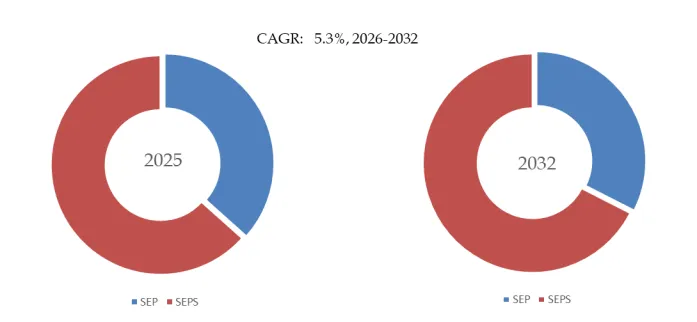

Segment by Type:

- Double-sided PVF Coating – Tedlar legacy. 20% of revenue (CAGR 8.2%).

- Double-sided PVDF Coating – Most common. 65% of revenue (CAGR 10.5%).

- Based on Other Fluorine Alloys (FEVE) – Emerging. 15% of revenue (CAGR 9.5%).

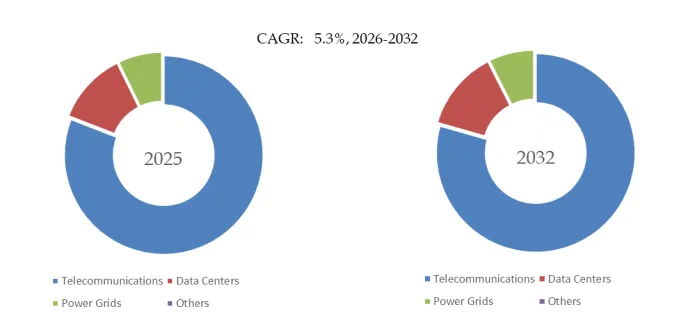

Segment by Application:

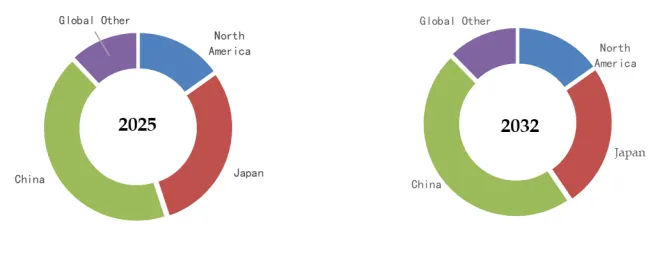

- Large-Scale Ground-Mounted Power Plant – Desert, grassland, rocky terrain. 60% of revenue.

- Floating Photovoltaic – Reservoirs, lakes, coastal. 20% of revenue (CAGR 14.5%).

- Agriculture and Livestock Photovoltaic – Agrivoltaics, grazing. 12% of revenue.

- Others – Rooftop, building-integrated. 8% of revenue.

Case Study 1 (Large-Scale Ground-Mounted – Gobi Desert, China): China’s 2GW Golmud solar park (Gobi Desert, high UV, sand abrasion, -20°C to +50°C) uses double-sided PVDF backsheets (Cybrid, 10.5 million m²). Bifacial modules (540W) achieve 15% rear-side gain (albedo 0.35). Standard backsheet (PET) would degrade in 5–7 years (yellowing, cracking). PVDF backsheet: 25-year warranty, 85% reflectivity retention after 300kWh/m² UV. Project cost: $1.1B. Backsheet cost: $110M (10% of module cost). Ground-mounted segment (60% of revenue) growing 9% CAGR.

Case Study 2 (Floating PV – 150MW Reservoir, China): Anhui Province floating PV project (150MW, on reservoir) uses double-sided PVDF backsheets (Taiflex, high WVTR resistance). Requirements: high humidity (100% RH), water exposure (floating platform), and algae resistance. PVDF provides <0.8g/m²/day WVTR (prevents moisture ingress), UV resistance (water-reflected UV), and chemical resistance (algae treatment). Floating PV segment (20% of revenue) fastest-growing (CAGR 14.5%).

Case Study 3 (Agrivoltaics – Grazing Land, France): French agrivoltaic project (25MW, sheep grazing) uses double-sided PVF backsheets (Toppan, white, high reflectivity). Requirements: mechanical resistance (sheep rubbing), chemical resistance (manure, urine), and high reflectivity (rear-side gain from ground-reflected light). White PVF (90% reflectivity) vs. PVDF (80%) provides 2% additional rear-side gain (0.5MW additional output for 25MW project). Agrivoltaics segment (12% of revenue) growing 11% CAGR.

Case Study 4 (Large-Scale – Sahara Desert, Morocco): Noor Ouarzazate solar complex (Morocco, Sahara Desert) uses double-sided PVDF backsheets (Lucky Film) for 100MW bifacial installation. Requirements: extreme UV (Sahara UV 30% higher than standard test conditions), sand abrasion, and 50°C+ ambient temperatures. PVDF backsheet qualified to 400kWh/m² UV (35-year equivalent). Project backsheet cost: $5M (for 500,000 m²). Ground-mounted segment drives 60% of revenue.

Industry Segmentation: PVDF vs. PVF vs. FEVE and Application Perspectives

From an operational standpoint, double-sided PVDF (65% of revenue, fastest-growing) dominates large-scale ground-mounted and floating PV due to cost-effectiveness ($8–12/m²) and proven 25-year durability. Double-sided PVF (20% of revenue) dominates premium agrivoltaics and high-reflectivity applications (90% vs. 80% for PVDF). FEVE (15% of revenue) serves specialty applications requiring transparency. Large-scale ground-mounted (60% of revenue) drives volume (GW-scale projects in China, India, Middle East, US). Floating PV (20%, fastest-growing at 14.5% CAGR) driven by land constraints (China, Japan, Netherlands, Singapore). Agrivoltaics (12%) driven by Europe and Japan (dual-use land policy).

Technical Challenges and Recent Policy Developments

Despite strong growth, the industry faces four key technical hurdles:

- Adhesion between fluorine coating and PET: PVDF and PVF require primer layer (improves adhesion). Poor adhesion leads to delamination (coating peeling). Solution: plasma treatment of PET surface and optimized primer chemistry (acrylic, polyurethane).

- Reflectivity degradation over time: UV exposure reduces white pigment reflectivity (TiO₂ degradation). PVDF retains 80–85% reflectivity after 25 years; PVF retains 85–90%. Solution: improved TiO₂ dispersion and UV-stabilized pigments.

- Cost pressure from single-sided alternatives: Single-sided fluorine backsheet (PET + one fluorine layer) costs 30–40% less ($6–8/m² vs. $9–12/m²) but lacks rear-side durability. Bifacial modules with rear-side albedo gain >10% justify double-sided premium. Cost-benefit analysis: 2% efficiency gain × 25 years = $50–100 additional revenue per module; double-sided backsheet cost premium $3–5 per module.

- Recycling of fluorine backsheets: PVDF and PVF difficult to recycle (fluorine content, multilayer structure). Policy update (March 2026): EU PV Cycle (voluntary recycling program) extended to include fluorine backsheets; new separation technology (pyrolysis + HF recovery) under development.

独家观察: Bifacial Module Market Share Driving Double-Sided Backsheet Demand

An original observation from this analysis is bifacial module market share (>50% of new installations in 2025) directly driving double-sided fluorine backsheet demand. Bifacial modules generate 5–30% additional power from rear side (albedo-dependent). Rear-side exposure to UV, humidity, and mechanical stress requires same protection as front side. Single-sided backsheet (PET + one fluorine layer) fails on rear side within 5–7 years, voiding 25-year warranty. All major bifacial module manufacturers (Longi, JinkoSolar, Trina, JA Solar, Canadian Solar) now specify double-sided fluorine backsheet for bifacial products. Double-sided backsheet market grew from 10% of backsheet market (2020) to 35% (2025), projected 60% by 2030.

Additionally, floating PV (FPV) and agrivoltaics are fastest-growing application segments (CAGR 14.5% and 11% respectively). FPV requires backsheet with ultra-low WVTR (<0.8g/m²/day) to prevent moisture ingress (floating on water). Agrivoltaics requires chemical resistance (fertilizers, pesticides) and mechanical resistance (animal rubbing). Both segments specify double-sided PVDF (cost-effective, 25-year proven). FPV installed capacity: 5GW (2025), projected 30GW by 2030. Agrivoltaics: 10GW (2025), projected 50GW by 2030. Looking toward 2032, the market will likely bifurcate into double-sided PVDF backsheets for large-scale ground-mounted, floating PV, and agrivoltaics (cost-driven, 25-year durability, 9–11% annual growth) and double-sided PVF backsheets for premium high-reflectivity applications (performance-driven, 7–9% annual growth), with FEVE capturing niche transparency applications.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp