SEPS Thermoplastic Elastomer Market Summary

SEPS thermoplastic elastomer is a hydrogenated styrenic block copolymer containing isoprene segments. After hydrogenation, the copolymer is structured as polystyrene (S) – polyethylene (E) – polypropylene (P) – polystyrene (S), abbreviated as SEPS.

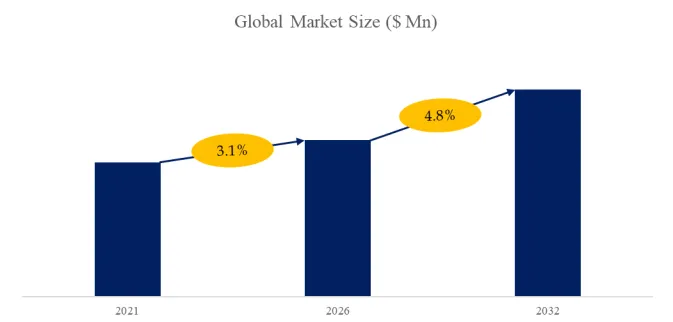

According to the new market research report “Global SEPS Thermoplastic Elastomer Market Report 2026-2032”, published by QYResearch, the global SEPS Thermoplastic Elastomer market size is projected to reach USD 0.49 billion by 2032, at a CAGR of 4.8% during the forecast period.

Figure00001. Global SEPS Thermoplastic Elastomer Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global SEPS Thermoplastic Elastomer Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

1. Market Drivers

Sustained growth in adhesives and sealants demand

SEPS is widely used in hot-melt and pressure-sensitive adhesive systems due to its excellent flexibility, resilience, and compatibility with tackifiers. Demand remains strong in packaging, hygiene products, labels, and electronics assembly. Its low odor, high transparency, and formulation flexibility enable it to gradually replace traditional SIS in high-end adhesive formulations. Meanwhile, the expansion of e-commerce logistics and disposable hygiene products continues to increase adhesive consumption, directly driving SEPS demand and making this the most important growth driver.

Rising demand for high-performance modified materials

SEPS serves as an effective modifier for polyolefins, engineering plastics, and oil-based systems, significantly improving impact resistance, flexibility, and low-temperature performance. Its applications are expanding across automotive interiors, wires and cables, home appliances, and industrial products. With strong weather resistance and thermal stability, SEPS performs well in outdoor and demanding environments. In addition, driven by lightweighting trends, demand for high-performance elastomers in automotive and electronics is increasing, further supporting SEPS penetration.

Upgrading safety standards in medical and consumer applications

As global requirements for material safety and environmental performance become stricter, SEPS is increasingly adopted in medical devices, food-contact materials, and high-end consumer products. Its saturated structure provides high chemical stability, low extractables, and low odor. In applications such as medical tubing, infusion systems, seals, and flexible packaging, SEPS can replace certain PVC and rubber materials to meet more stringent regulatory standards. Aging populations and rising healthcare expenditure also support demand for safer elastomer materials.

2. Market Restraints

High production cost limits large-scale expansion

SEPS is produced via hydrogenation of SIS, involving complex processes and stringent catalyst and process control requirements, resulting in significantly higher costs than conventional SBS and SIS. In price-sensitive applications, such as low-end adhesives and general plastic modification, substitution incentives remain limited. In addition, raw material price fluctuations and rising hydrogenation costs further squeeze downstream margins, restraining rapid demand expansion.

Strong competition from alternative materials

SEPS faces competition from SEBS, TPU, TPO, and modified PVC across multiple applications. For example, in automotive and cable sectors, SEBS dominates due to its mature application base and cost advantages, while TPU offers superior performance in high elasticity or abrasion-resistant applications. This competitive landscape means SEPS often relies on niche advantages, such as superior transparency or soft-touch properties, limiting its broader market share growth.

Long development and certification cycles

Applications in high-requirement sectors such as medical, automotive, and electronics require extensive formulation development, long-term performance validation, and end-use certification, resulting in lengthy adoption cycles. This increases the difficulty of material substitution and raises switching costs for customers. Moreover, varying performance requirements across applications necessitate customized grades, increasing technical service barriers and limiting entry and scale-up for smaller manufacturers.

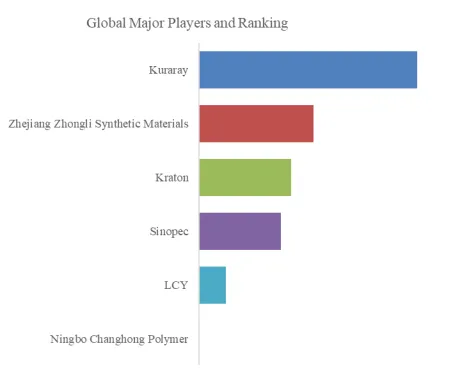

Figure00002. Global SEPS Thermoplastic Elastomer Top 6 Players Ranking and Market Share (Ranking is based on the revenue of 2025, by revenue, continually updated)

Above data is based on report from QYResearch: Global SEPS Thermoplastic Elastomer Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

According to QYResearch Top Players Research Center, the global key manufacturers of SEPS Thermoplastic Elastomer include Kuraray, Zhejiang Zhongli Synthetic Materials, Kraton, Sinopec, LCY, etc. In 2025, the global top five players had a share more than 80% in terms of revenue.

Major Players Profiles:

Kuraray

Kuraray is the global pioneer and undisputed leader in the SEP (Hydrogenated Styrene-Isoprene Copolymer) market, commercializing these advanced elastomers under the renowned brand name SEPTON™. As a Japanese chemical giant with over a century of heritage, Kuraray has mastered the precise hydrogenation of isoprene monomers, resulting in saturated block copolymers that offer exceptional clarity, UV resistance, and thermal stability compared to unsaturated precursors.

The company’s SEP portfolio, particularly the 1000-series, is highly valued for its superior performance as a viscosity index improver in high-end lubricants, where it provides excellent shear stability and low-temperature fluidity. Beyond lubrication, Kuraray’s SEP materials are essential components in clear cable gels, specialty adhesives, and medical-grade compounds.

众立合成材料

Zhejiang Zhongli Synthetic Materials is a premier Chinese high-tech enterprise that has successfully broken the international monopoly in the field of high-end HSBCs, including SEP and SEPS. Located in Zhejiang province, Zhongli has established itself as a critical player in the “import substitution” strategy by developing indigenous technology for the large-scale production of hydrogenated styrenic copolymers. Their SEP product line is specifically engineered to meet the rigorous demands of the domestic and Asian markets, offering high-performance alternatives for specialized industrial applications.

The company’s strength lies in its advanced catalytic hydrogenation technology and flexible manufacturing processes, which allow for the customization of molecular structures to suit specific client needs. Zhongli’s SEP grades are widely adopted in the production of high-stability lubricant additives, fiber optic cable filling compounds, and sophisticated hot-melt adhesives. By combining competitive pricing with technical reliability, Zhongli has become a vital supplier for sectors ranging from automotive engineering to telecommunications. As they expand their global footprint, the company continues to invest in R&D to enhance the sustainability and performance limits of their thermoplastic elastomer portfolio.

Kraton

Kraton, the original inventor of styrenic block copolymers, stands as a global titan in the specialty chemicals industry. Under its flagship Kraton™ G brand, the company provides a sophisticated range of SEP elastomers known for their exceptional purity and performance. Kraton’s SEP technology focuses on delivering maximum oxidative stability and chemical resistance, which are critical for applications requiring long-term durability in challenging environments.

Kraton’s SEP grades are industry standards for formulated products such as clear oil gels, high-performance coatings, and specialty lubricants. Their materials offer a unique combination of high-temperature resilience and excellent compatibility with various plasticizers and resins. Following its acquisition by DL Chemical, Kraton has leveraged a more robust global supply chain to better serve the evolving needs of the automotive and telecommunications industries. Furthermore, Kraton is a leader in sustainable innovation, actively exploring bio-based pathways to reduce the environmental impact of its elastomer production. With a massive intellectual property portfolio and technical centers worldwide, Kraton continues to drive the engineering standards for thermoplastic elastomers globally.

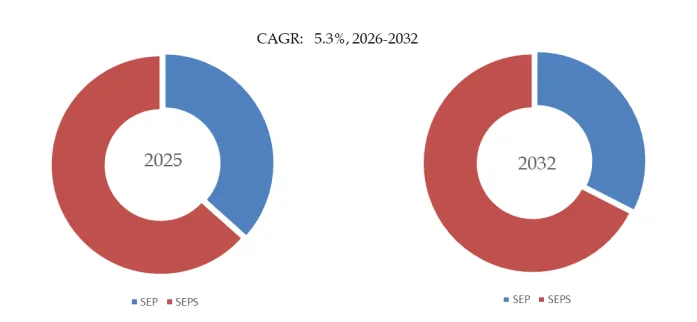

Figure00003. SEPS Thermoplastic Elastomer, Global Market Size, Split by Product Segment

Based on or includes research from QYResearch: Global SEPS Thermoplastic Elastomer Market Report 2026-2032.

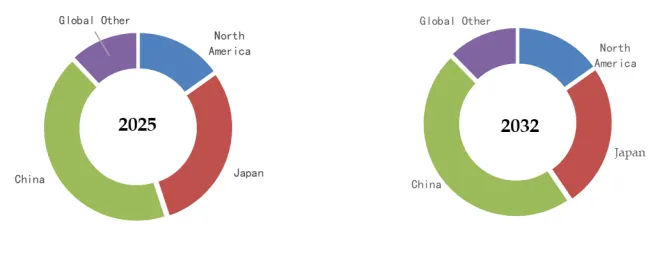

Figure00004. SEPS Thermoplastic Elastomer, Global Market Size, Split by Region (Production Volume)

Based on or includes research from QYResearch: Global SEPS Thermoplastic Elastomer Market Report 2026-2032.

About The Authors

| Zhang Xuelu – Analyst for this report | |

| Email: zhangxuelu@qyresearch.com

|

|

| Website: www.qyresearch.com Hot Line:4006068865

QYResearch focus on Market Survey and Research US: +1-888-365-4458(US) +1-202-499-1434(Int’L) EU: +44-808-111-0143(UK) +44-203-734-8135(EU) Asia: +86-10-8294-5717(CN) +852-30628839(HK) |

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp