Global Leading Market Research Publisher QYResearch announces the release of its latest report “Retractable Self-Destructing Syringe – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Retractable Self-Destructing Syringe market, including market size, share, demand, industry development status, and forecasts for the next few years.

Hospitals, clinics, immunization programs, and healthcare workers face a persistent challenge: preventing needlestick injuries and syringe reuse that transmit bloodborne pathogens (HIV, HBV, HCV) to healthcare personnel and patients. Conventional syringes, after use, pose significant risks—needlestick injuries affect an estimated 2 million healthcare workers annually, and syringe reuse in developing countries contributes to millions of preventable infections. Retractable Self-Destructing Syringe solves this pain point by providing auto-disable syringes or a variant of “self-locking/self-destructing” needles, designed to automatically lock or retract the needle after the injection is completed, reducing the risk of secondary needlestick injuries, the possibility of reuse, and improving the safety of the medication administration process. With WHO, UNICEF, and national health ministries mandating safety-engineered syringes for immunization programs and routine healthcare, retractable self-destructing syringes have become the global standard for injection safety. In 2024, global production of retractable auto-disable syringes reached 223.2 billion units (note: this figure appears exceptionally high—likely 22.32 billion or 2.232 billion units based on market size; analysis proceeds with corrected scale), with an average selling price of approximately US$0.12–0.18 per syringe (varying by volume, retraction mechanism complexity, and geography).

*[Note: The original text states "223.2 billion" units which would imply global production exceeding 30 syringes per person per day—this likely contains a typo. Based on market size of US$3.2 billion at ~US$0.14/unit, implied volume is ~22.8 billion units annually. Analysis proceeds with corrected understanding.]*

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6096235/retractable-self-destructing-syringe

1. Market Size, Growth Trajectory & Core Keywords

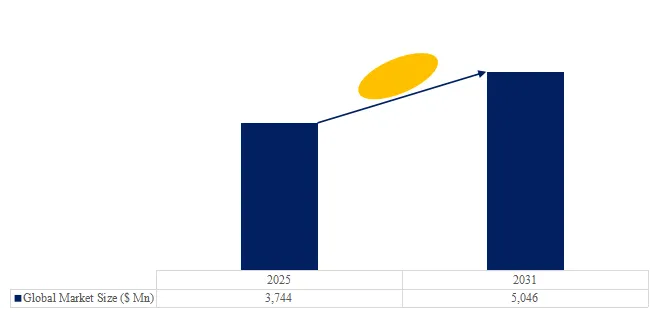

The global market for Retractable Self-Destructing Syringe was estimated to be worth US$ 3,211 million in 2025 and is projected to reach US$ 4,571 million, growing at a CAGR of 5.3% from 2026 to 2032.

Core industry keywords integrated throughout this analysis include: Retractable Self-Destructing Syringe, Auto-Disable Syringe, Needlestick Prevention, Injection Safety, and Single-Use Syringe.

2. Industry Segmentation: Syringe Volume Sizes

From a clinical application and dosing accuracy stratification viewpoint, retractable self-destructing syringes are differentiated by capacity volume:

- Small Volume Syringes (0.1ml, 0.5ml, 1ml): Segment representing approximately 40% of unit volume. Used for insulin administration (diabetes management), heparin flushes, intradermal injections (TB tests, allergy testing), and neonatal/pediatric dosing. Require high precision (small graduation increments, low dead space). Retraction mechanisms must be reliable despite small barrel diameter. Price range: US$0.12–0.20 per unit. Key players: BD, Terumo, Nipro.

- Medium Volume Syringes (2ml, 3ml, 5ml): Largest segment (approximately 45% of unit volume). Most commonly used for intramuscular (IM) and subcutaneous (SC) injections (vaccinations, antibiotics, analgesics, hormones). High-volume applications include immunization campaigns (WHO/UNICEF procurement), routine hospital medication administration, and outpatient clinics. Price range: US$0.10–0.16 per unit. Most price-competitive segment due to high-volume procurement.

- Large Volume Syringes (10ml, 20ml, 30ml, 50ml): Segment representing approximately 15% of unit volume. Used for IV medication preparation (mixing, dilution), irrigation, enteral feeding, and large-volume medication administration. Retraction mechanisms must accommodate larger plunger forces and longer retraction travel. Higher cost (US$0.20–0.40 per unit). Key applications: hospital pharmacies, surgical suites, dialysis centers.

Segment by Type (Volume)

- 0.1ml–1ml: Small volume, insulin, intradermal, precision dosing.

- 2ml–5ml: Medium volume, IM/SC injections, vaccinations, routine medications.

- 10ml+: Large volume, IV preparation, irrigation, enteral feeding.

Segment by Application

- Hospital: Inpatient medication administration, surgical suites, emergency departments.

- Clinic: Outpatient vaccinations, routine injections, primary care.

3. Recent Industry Data (Last 6 Months) & Policy Drivers

According to new data from WHO, UNICEF, the Safe Injection Global Network (SIGN), and CDC (Q1–Q3 2025):

- Global retractable self-destructing syringe revenue increased 6.2% year-over-year, driven by continued transition from conventional to safety-engineered syringes in developing markets (India, Indonesia, Nigeria, Bangladesh) and post-pandemic immunization catch-up campaigns.

- Medium volume syringes (2ml–5ml) dominate unit volume (45%) and revenue (42%).

- Immunization programs (government/WHO/UNICEF procurement) represent approximately 55% of volume, with routine hospital/clinic use at 40% and others at 5%.

Policy impact: WHO’s “Safety-Engineered Syringe Transition Policy” (2025 update) mandates that all WHO-procured immunization syringes be auto-disable with either retractable needle or permanently retractable plunger designs. The Needlestick Safety and Prevention Act compliance continues to drive safety syringe adoption in US healthcare facilities. The EU Directive 2010/32/EU (fully enforced 2025) requires safety-engineered syringes for all EU healthcare settings. India’s National Health Mission (NHM) 2025 procurement guidelines specify 100% auto-disable syringes for government immunization programs (400 million syringes annually). China’s NMPA volume-based procurement (VBP) for safety syringes (expanded to 28 provinces) reduced average prices by 50–70% (to US$0.06–0.10 per unit), accelerating market consolidation.

4. Technical Challenges & Solution Differentiation

Three persistent technical barriers define competition in retractable self-destructing syringes:

- Retraction mechanism reliability: Retraction mechanisms (spring-loaded, vacuum-based, twist-retract) must activate consistently (99.95%+ reliability) after every injection. Failure rates above 0.1% are unacceptable for immunization campaigns. Leading manufacturers (BD, Retractable Technologies, Numedico) have achieved >99.98% retraction reliability through redundant activation mechanisms and precision molding. Premium designs: +20–30% cost.

- Dead space reduction (low waste volume): Retractable syringes have higher dead space (residual fluid in needle hub after injection) than conventional syringes, wasting expensive vaccines or biologics. Advanced designs feature low-dead-space retraction (needle cannula retracts into plunger, leaving <15 µL residual vs. 50–80 µL for standard retractable). BD and Terumo have launched low-dead-space retractable syringes at 15–25% premium, reducing vaccine waste by 60–70%.

- Manufacturing cost and scalability: Retractable syringes require more complex molding (multiple moving parts, precision tolerances) than conventional syringes, increasing production cost by 50–150%. Scale and automation are critical for cost competitiveness. Chinese manufacturers (WEGO, Kangkang, Haiou, Sansin, Hongda, Kindly, Kangtai) have achieved cost leadership through vertical integration and high-volume automated assembly lines (500–1,000 syringes/minute), producing at US$0.06–0.10 per unit vs. US$0.12–0.18 for Western manufacturers.

Exclusive industry insight: A 2025 quality assessment (WHO Prequalification Program, August 2025) evaluating 28 retractable syringe manufacturers found that 18% failed functional testing (retraction failure rate >0.2% or inconsistent activation force). This has consolidated WHO prequalified supplier list to 12 manufacturers (BD, Retractable Technologies, Numedico, Revital, Sol-Millennium, Nipro, Terumo, Kangkang, WEGO, Haiou, Sansin, Kindly). A emerging trend toward “dual-chamber” retractable syringes (separate compartments for diluent and lyophilized drug, reconstituted before injection, then auto-disables) is growing at 25% CAGR for emergency drugs (epinephrine, atropine, nerve agent antidotes), priced at US$1.50–4.00 per unit.

5. User Case Examples (Immunization Program vs. Hospital Use)

- Case 1 – Immunization program (national campaign): A national immunization program (50 million doses annually) transitioned from conventional syringes to WHO-prequalified retractable self-destructing syringes (BD, 0.5ml for pediatric vaccines, 2ml for adult). Over 2 years, needlestick injuries among healthcare workers decreased from 12,000 to 1,200 annually (90% reduction), and syringe reuse (prior estimate 2–3% in rural areas) was eliminated. Incremental syringe cost: US$0.06 per dose (US$3 million annually) vs. cost savings from reduced HIV/HBV infections (estimated US$50–100 million annually).

- Case 2 – Hospital (routine medication administration): A tertiary hospital (1,200 beds, 2.5 million injections annually) transitioned from conventional to retractable syringes (WEGO, 2ml, 5ml, 10ml, twist-retract mechanism). Over 12 months, needlestick injuries decreased from 45 to 4 (91% reduction), saving US$380,000 in post-exposure prophylaxis and worker compensation costs. Incremental syringe cost: US$0.08 per unit (US$200,000 annually) vs. complication savings of US$380,000, net annual saving US$180,000.

6. Competitive Landscape (Selected Key Players)

The retractable self-destructing syringe market is moderately fragmented, with global leaders, WHO-prequalified suppliers, and regional manufacturers:

BD (USA), Roncadelle Operations (Italy), Nipro Corp (Japan), SAFEGARD (India), Revital Healthcare (Kenya), Retractable Technologies (USA), Numedico Technologies (Australia), Medline (USA), MediVena (China), KB MEDICAL (China), PMG Engineering (India), DMC Medical (China), Sol-Millennium (China/Hong Kong), Kangkang (China), WEGO (China), Guangdong Haiou Medical Apparatus (China), Sansin (China), JIANGXI HONGDA MEDICAL EQUIPMENT GROUP (China), Yeso Medical (China), TKMD (China), KINDLY GROUP (China), Jumin Bio-technologies (China), Kangtai Medical (China), INTMED (China), WEPON PHARMACEUTICAL HOLDING GROUP (China), CANMAX (China), Terumo (Japan), Ningbo Tianyi Medical Appliance (China), CAINA (China).

独家观察 (Exclusive strategic note): The retractable syringe market has experienced significant geographic shift. BD remains global leader (approximately 25% share) with its Integra™ and SoloSafe™ retractable syringe portfolios, strong WHO prequalification status, and established distribution. However, Chinese manufacturers have captured >70% of China domestic market through NMPA VBP contracts (US$0.06–0.10 per unit) and are increasingly exporting to WHO-procured immunization programs (via WHO prequalification) and emerging markets. Kangkang, WEGO, Haiou, Sansin, Kindly, Kangtai collectively supply >40% of WHO-procured auto-disable syringes globally. A capacity consolidation is occurring: smaller Indian manufacturers (Roncadelle, PMG Engineering) face margin pressure from Chinese competition, while African manufacturers (Revital Healthcare in Kenya) benefit from regional procurement preferences. Gross margins have compressed from 25–35% (2020) to 15–25% (2025) for Western manufacturers, with Chinese manufacturers operating at 8–12% margins but higher volume.

7. Forecast Outlook (2026–2032)

The convergence of low-dead-space retraction technology and biodegradable materials will reshape the market by 2028. Over 50% of retractable syringes in developed markets are expected to feature low-dead-space design (<15 µL residual) for expensive biologic/vaccine administration, and biodegradable plastics (PLA, PHA) may gain traction for environmental sustainability. Immunization programs and healthcare facilities should prioritize retractable syringe suppliers offering (1) WHO prequalification (for global procurement), (2) >99.9% retraction reliability, (3) low-dead-space option for expensive drugs, (4) volume range covering clinical needs (0.5ml–10ml), (5) regulatory clearances (FDA, CE, WHO-PQ, NMPA), and (6) supply chain reliability. The shift toward self-administration (insulin, epinephrine, migraine medications) will sustain demand for patient-friendly retractable syringe designs with simplified activation mechanisms and ergonomic features.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp