Global Leading Market Research Publisher QYResearch announces the release of its latest report “Elk Meat – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Elk Meat market, including market size, share, demand, industry development status, and forecasts for the next few years.

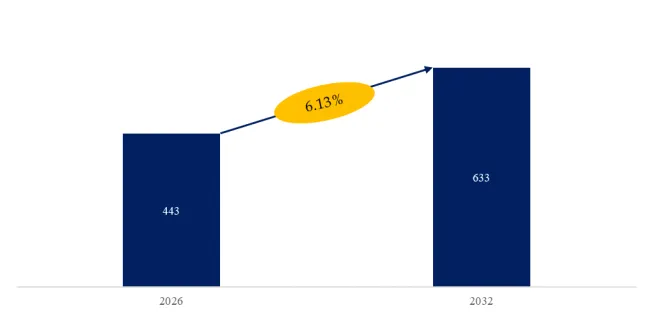

The global market for Elk Meat was estimated to be worth US180millionin2025andisprojectedtoreachUS180millionin2025andisprojectedtoreachUS280 million by 2032, growing at a CAGR of 6.5% from 2026 to 2032. For health-conscious consumers, specialty meat retailers, and restaurant chefs, the core business imperative lies in sourcing elk meat (North American elk, Cervus canadensis, also known as wapiti) that addresses the critical need for extremely lean, nutrient-dense, grass-fed red meat alternative to beef, with lower fat (2-4% vs beef 15-30%), lower calories (130-150 kcal/100g vs beef 250-300), higher protein (22-26g/100g vs beef 18-20g), higher iron, zinc, vitamin B12, and a mild, sweet, non-gamey flavor (more palatable than venison). Elk are raised on pasture (grass-fed), no antibiotics, no growth hormones (USDA grass-fed label), and are not fed grain (unlike feedlot cattle). Elk meat has a fine texture, less marbling than beef, requires careful cooking (medium-rare). Types: frozen meat (export, long shelf life 12-24 months) and chilled meat (domestic, vacuum-packed, 30-45 days shelf life). Applications: retails (specialty butcher shops, farmers markets, online meat delivery (US Wellness Meats), supermarkets (natural food stores)), foodservices (upscale restaurants (elk steak, elk burger, elk medallions, elk tenderloin), lodges, resorts), food processing plants (further processing — elk jerky, elk sausage, elk sticks, elk patties, elk meatballs), others (pet food, zoos). Key players: Jackson Hole Buffalo Meat (US), Northfork Bison (US), Northstar (US), Shaffer Venison Farms (US), Canadian Rangeland Bison & Elk (Canada), Wapiti Ways (US). The market is driven by healthy eating trends (lean protein), grass-fed, paleo/keto diets, and exotic meat consumption.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/releases/5985585/elk-meat

1. Market Drivers: Lean Protein, Grass-Fed, and Exotic Meat Demand

Several powerful forces are driving the elk meat market:

Lean protein advantage (2-4% fat) – Lower fat, lower calories than beef, pork, chicken, bison. Paleo, keto, Whole30.

Grass-fed, no antibiotics, no hormones – Natural, clean label. Pasture-raised.

Exotic meat popularity (elk, bison, venison) – Culinary adventure, chefs feature elk on menus.

Recent market data (December 2025): According to Global Info Research analysis, frozen meat dominates with approximately 75% revenue share (direct-to-consumer shipping, export). Chilled meat 25% share (local retail, foodservice). Retails (specialty online, farmers markets) largest application (55% share). Foodservices (restaurants, lodges) 30% share. Food processing plants (jerky, sausage) 10% share. Others 5% share. North America (US, Canada) largest market (95% share). Europe (import) 5% share. Northstar, Jackson Hole Buffalo Meat, Northfork Bison, Canadian Rangeland Bison & Elk, Shaffer Venison Farms, Wapiti Ways leaders.

2. Meat Types and Key Specifications

| Type | Temp | Shelf Life | Packaging | Cuts | Price (USD/lb) | Share |

|---|---|---|---|---|---|---|

| Frozen Meat | -18°C | 12-24 months | Vacuum pack | Steak, ground, roast, tenderloin, jerky | $20-40 | ~75% |

| Chilled Meat | 0-4°C | 30-45 days | Vacuum pack, MAP | Steak, ground | $30-50 | ~25% |

Key specifications: Species: North American elk (Cervus canadensis), also called wapiti (Shawnee). Raised: pasture-raised, grass-fed (no grain finishing), no feedlots, no antibiotics, no added hormones. USDA grass-fed certified. Flavor: mild, sweet, less gamey than deer (venison). Texture: fine-grained, tender (young elk). Nutrition (3.5 oz / 100g raw): calories 130-150, fat 2-4g, saturated fat 0.5-1g, cholesterol 60-70mg, protein 22-26g, iron 3-4mg (higher than beef), B12. Cuts: steak (ribeye, strip, tenderloin (filet mignon), sirloin, flank), roast (chuck, rump, brisket), ground (95/5, 90/10), burger patty, stew meat, fajita strips, jerky (dried). Cooking: medium-rare (130-135°F) to avoid dryness. Aging: wet-aged 14-21 days. Wild elk (hunted) available but not commercial (game meat restrictions).

Exclusive observation (Global Info Research analysis): Elk meat market is very small, premium (US$20-50/lb), direct-to-consumer (online) niche. Northstar (Minnesota) sells elk (ground, steak, roast). Jackson Hole Buffalo Meat (Wyoming) also elk. Northfork Bison (Washington) elk. Shaffer Venison Farms (Pennsylvania). Canadian Rangeland Bison & Elk (Alberta). Wapiti Ways (Colorado). Elk tenderloin is the most tender cut, comparable to beef filet mignon. Elk ground meat (95/5) extremely lean (2-5% fat). Elk jerky (high protein, low fat, low carb) popular for keto, hiking, camping. Elk meat not available in mainstream supermarkets (limited supply, higher price). Farmed elk (New Zealand, Ireland) exported to Europe.

User case – online elk meat (December 2025): US consumer orders Northstar elk ribeye steak (12 oz, US$35) online. Grass-fed, frozen vacuum pack. Thaws, grills medium-rare (135°F). Mild flavor, tender. Paleo diet.

User case – restaurant elk tenderloin (January 2026): Fine dining restaurant (Colorado) sources elk tenderloin (Northstar, Jackson Hole). Serves as filet mignon (8 oz, US$55). Sautéed in butter, garlic, rosemary. Customers rating excellent.

3. Key Challenges and Technical Difficulties

Limited supply (20,000-30,000 elk farmed in North America) – Much smaller than bison (50,000). Price premium.

Extremely lean (dryness, overcooking) – Less fat than beef or bison. Cook medium-rare (130-135°F) max. Use sous-vide.

Technical difficulty – farmed vs wild (game legality): Wild elk cannot be sold commercially (game meat regulations). Farmed elk inspected (USDA).

Technical development (October 2025): Northstar (Minnesota) launched pre-seasoned elk medallions (garlic herb). Vacuum pack, grilled or pan-seared. 10 minutes to table. Foodservice, retail.

4. Competitive Landscape

Key players include: Jackson Hole Buffalo Meat (US), Northfork Bison (US), Northstar (US), Shaffer Venison Farms (US), Canadian Rangeland Bison & Elk (Canada), Wapiti Ways (US). Small, family-owned farms. No large meat packers.

Regional dynamics: North America (US, Canada) 95%. Europe (New Zealand, Ireland) farmed elk export. Elk raised in US (Minnesota, Colorado, Wyoming, Montana, Washington, Pennsylvania, Texas).

5. Outlook

Elk meat market will grow at 6.5% CAGR to US$280 million by 2032, driven by healthy eating, grass-fed demand, and exotic meat popularity. Technology trends: sous-vide pre-cooked, elk subscription boxes, and jerky diversification. North America dominant. Frozen meat largest segment.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp