Introduction – Core User Needs & Industry Context

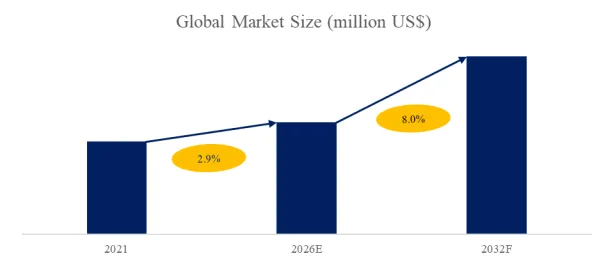

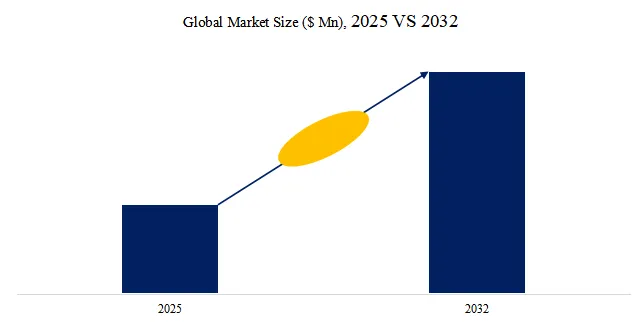

Designers of battery-powered devices (wearables, smart home sensors, portable electronics) require magnetic sensors that detect both north and south pole magnetic fields while consuming minimal power. Traditional unipolar Hall switches detect only one polarity, limiting design flexibility. Micropower omnipolar Hall effect switches — magnetic sensors that output digital signals when detecting any magnetic field polarity, featuring low power consumption, fast response, and compact size — solve these challenges. They are widely used in portable devices, smart homes, wearables, industrial automation, and automotive electronics. According to the latest industry analysis, the global market for Micropower Omnipolar Hall Effect Switches was estimated at US$ 126 million in 2025 and is projected to reach US$ 205 million by 2032, growing at a CAGR of 7.3% from 2026 to 2032. In 2024, global sales reached 650 million units, with an average selling price of approximately US$ 0.18 per unit.

Global Leading Market Research Publisher QYResearch announces the release of its latest report “Micropower Omnipolar Hall Effect Switches – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Micropower Omnipolar Hall Effect Switches market, including market size, share, demand, industry development status, and forecasts for the next few years.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6097115/micropower-omnipolar-hall-effect-switches

1. Core Keyword Integration & Sensitivity Classification

Three key concepts define the micropower omnipolar Hall switch market: Low-Power Magnetic Sensing, Omnipolar Polarity Detection, and Fast-Response Digital Output. Based on operating point (BOP) sensitivity, switches are classified into four types:

- ±3 Gauss: High sensitivity for weak magnets, long sensing distance. ~25% market share.

- ±20 Gauss: Standard sensitivity, most common. ~45% share, largest segment.

- ±60 Gauss: Low sensitivity, noise-immune, for harsh environments. ~20% share.

- Others (custom sensitivity): Specialty applications. ~10% share.

2. Industry Layering: Consumer Electronics vs. Automotive vs. Industrial – Divergent Requirements

| Aspect | Consumer Electronics | Automotive Electronics | Industrial Automation |

|---|---|---|---|

| Primary application | Smartphones, wearables, laptops | Door/window position, seat sensors | Position detection, encoders |

| Key requirement | Ultra-low power (μA), small size | High reliability, wide temp (-40°C to +125°C) | Noise immunity, long life |

| Typical power consumption | 1-5 μA | 5-20 μA | 10-50 μA |

| Preferred BOP | ±20G or ±60G | ±60G (noise-immune) | ±20G or ±60G |

| Market share (2025) | ~50% | ~25% | ~15% |

Exclusive observation: The consumer electronics segment dominates (50% share), driven by high-volume devices. The automotive segment commands highest reliability requirements.

3. Hall Switch Types Comparison

| Feature | Unipolar | Bipolar | Omnipolar |

|---|---|---|---|

| Polarity detection | One only | One with hysteresis | Both |

| Power consumption | Low | Low | Ultra-low (micropower) |

| Magnet orientation | Fixed | Fixed | Flexible |

| Best for | Simple open/close | Speed sensing | Position, lid detection |

4. Recent Data & Technical Developments (Last 6 Months)

Between Q4 2025 and Q1 2026, several advancements have reshaped the micropower omnipolar Hall switch market:

- 1 μA power consumption: New generation switches consume 1 μA (vs. 3-5 μA previously), extending battery life in wearables. This segment grew 20% in 2025.

- Ultra-small packages (DFN1006, 1.0×0.6mm) : For space-constrained devices (TWS earbuds, smart rings). Adoption grew 15% in 2025.

- Integrated latch function: No external pull-up resistors needed, reducing BOM. This segment grew 10% in 2025.

- Policy driver – Energy efficiency standards (2025) : Stricter battery life requirements for portable devices, driving low-power sensor adoption.

User case – Flip smartphone (Samsung Galaxy Z Fold) : Uses micropower omnipolar Hall switches for hinge position detection. Results: <5 μA power consumption, detects magnet regardless of orientation, and enables precise fold angle detection.

Technical challenge – Magnetic interference in dense PCBs: Nearby components create stray fields. Solutions include higher BOP (±60G) and shielding.

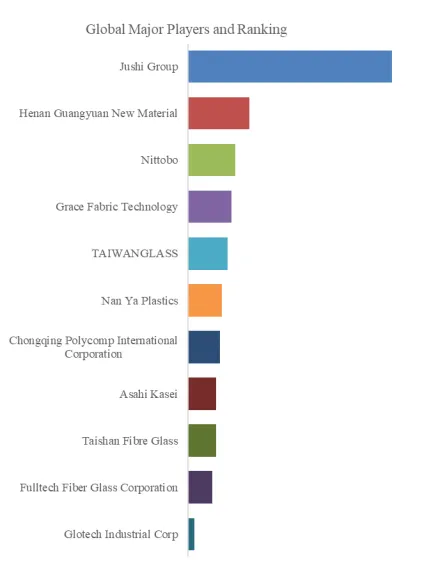

5. Competitive Landscape & Regional Dynamics

| Company | Headquarters | Key Strength |

|---|---|---|

| Melexis | Belgium | Automotive Hall sensors |

| Honeywell | USA | Industrial and aerospace |

| Texas Instruments | USA | Broad portfolio |

| Diodes Incorporated | USA | Consumer electronics |

| ABLIC | Japan | Ultra-low power |

| Rohm Semiconductor | Japan | Automotive and consumer |

| NOVOSENSE | China | Chinese domestic |

Regional dynamics:

- Asia-Pacific largest (55% market share), led by China (consumer electronics manufacturing), Japan, South Korea

- North America second (20%), with US

- Europe third (15%), with Germany, Belgium (Melexis)

- Rest of World (10%), emerging

6. Segment Analysis by Sensitivity and Application

| Segment | Characteristics | 2024 Share | CAGR (2026-2032) |

|---|---|---|---|

| By BOP | |||

| ±3G | High sensitivity | ~25% | 7.5% |

| ±20G | Standard | ~45% | 7% |

| ±60G | Noise-immune | ~20% | 8% |

| Others | Custom | ~10% | 7% |

| By Application | |||

| Consumer Electronics | Largest | ~50% | 7.5% |

| Automotive Electronics | High reliability | ~25% | 7% |

| Industrial Automation | Growing | ~15% | 7.5% |

| Others (medical, smart home) | Niche | ~10% | 8% |

The ±60G segment is fastest-growing (CAGR 8%). The consumer electronics application leads growth (CAGR 7.5%).

7. Exclusive Industry Observation & Future Outlook

Why omnipolar over unipolar/bipolar:

| Advantage | Explanation |

|---|---|

| Polarity flexibility | Works with any magnet orientation |

| Simplified assembly | No magnet polarity alignment needed |

| Lower BOM cost | Fewer design iterations |

| Micropower | 1-5 μA for battery devices |

Power consumption evolution:

| Generation | Typical Current | Application |

|---|---|---|

| 2015 | 10-20 μA | Basic portable |

| 2020 | 3-5 μA | Wearables |

| 2025 | 1-3 μA | TWS, smart rings |

| 2028 (est) | <1 μA | Implantable |

Package size evolution:

| Package | Dimensions | Year | Application |

|---|---|---|---|

| SOT-23 | 3.0 x 1.3 mm | 2010s | General |

| DFN1616 | 1.6 x 1.6 mm | 2015 | Portable |

| DFN1006 | 1.0 x 0.6 mm | 2020 | TWS, wearables |

| WLCSP | 0.8 x 0.6 mm | 2025 | Ultra-compact |

Key applications by device:

| Device | Hall Switches per device | Function |

|---|---|---|

| Smartphone | 3-5 | Flip cover, pen detection |

| Laptop | 2-4 | Lid close, tablet mode |

| TWS earbuds | 2-4 | In-ear detection, case lid |

| Smartwatch | 1-2 | Charger alignment |

| Electric vehicle | 10-20 | Door, window, seat position |

Market drivers:

- Wearables growth: TWS earbuds, smartwatches, smart rings

- Foldable phones: Hinge position detection

- Smart home: Door/window sensors

- Automotive: Contactless switches

Future trends:

- Sub-1 μA operation: For always-on sensing

- Integrated temperature sensing: Multi-function

- AEC-Q100 qualification: Automotive expansion

- Smaller packages: 0.6 x 0.3 mm

By 2032, the micropower omnipolar Hall switch market is expected to exceed US$ 205 million at 7.3% CAGR.

Regional outlook:

- Asia-Pacific largest (55%), with consumer electronics manufacturing

- North America second (20%)

- Europe third (15%)

- Rest of World (10%), emerging

Key barriers:

- Low ASP ($0.10-0.30) limits revenue growth

- Competition from reed switches (lower cost)

- Magnetic interference in dense designs

- Temperature sensitivity (drift over -40°C to +85°C)

- Supply chain concentration (few fabs)

Market nuance: The micropower omnipolar Hall switch market is growing steadily (7.3% CAGR), driven by wearables and foldable phones. ±20G dominates (45% share); ±60G fastest-growing (8% CAGR). Consumer electronics leads (50% share) and grows fastest (7.5% CAGR). Asia-Pacific leads (55%) with China manufacturing. Key trends: (1) 1 μA power consumption, (2) ultra-small packages (DFN1006), (3) integrated latch, (4) foldable phone hinge detection.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666 (US)

JP: https://www.qyresearch.co.jp