Global Leading Market Research Publisher QYResearch announces the release of its latest report “Emery Roller Rice Mill – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Emery Roller Rice Mill market, including market size, share, demand, industry development status, and forecasts for the next few years.

For rice millers and grain processors, achieving high-precision bran removal while maintaining yield and minimizing kernel breakage is a critical operational challenge. Emery roller rice mill addresses this need as a rice milling machine that utilizes a rotating emery roller as its core working component. The emery roller, sintered from abrasive grains (silicon carbide or emery) and bonding agents, features hard, sharp grits with uniform pores on its surface. During operation, paddy or brown rice undergoes grinding action from the high-speed rotating emery roller, combined with friction and extrusion from milling blades and pressure doors, stripping the bran layer (rice bran) from the kernel. Known for strong grinding characteristics, this mill type is particularly suitable for processing long-grain indica rice with high strength and for achieving high-precision milling. While offering high rice yield, the mill produces a slightly rougher milled rice surface with more noticeable temperature increase.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6099477/emery-roller-rice-mill

Market Size and Growth Fundamentals

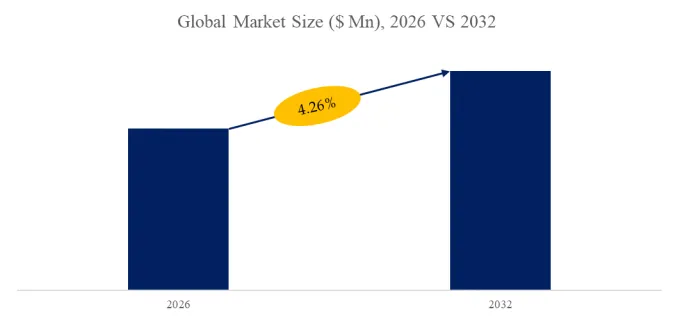

The global emery roller rice mill market was valued at US$ 266 million in 2025 and is projected to reach US$ 346 million by 2032, growing at a CAGR of 3.9% from 2026 to 2032. In 2024, global production reached approximately 7,632 units, with an average market price of US$ 33,500 per unit. Growth is driven by rice consumption growth, modernization of rice milling infrastructure, and demand for high-precision milling in premium rice markets.

Product Overview and Milling Mechanism

Emery roller rice mill employs abrasive grinding for bran removal:

- Core Component: Rotating emery roller sintered from abrasive grains (silicon carbide or emery)

- Surface Characteristics: Hard, sharp grits with uniform pores for consistent abrasion

- Milling Action: High-speed rotation combined with friction and extrusion from milling blades and pressure door

- Application: Long-grain indica rice (high-strength varieties) and high-precision milling of brown rice

Key operational characteristics:

- Strong Grinding: Effective for high-strength rice varieties resistant to conventional milling

- High Rice Yield: Efficient bran removal with minimal kernel loss

- Precision Control: Adjustable pressure and speed for customized milling degree

- Trade-offs: Slightly rougher milled rice surface; noticeable temperature increase during operation

Market Segmentation: Configuration Types and Applications

The emery roller rice mill market is segmented by configuration type into:

- Vertical Sand Roller Rice Mill: Vertically oriented roller for compact footprint; common in smaller mills and retrofit applications. Easier maintenance access.

- Horizontal Sand Roller Rice Mill: Horizontally oriented roller for higher throughput; dominant in large-scale commercial rice mills. Better for continuous operation.

By application, the market spans Rice Processing, Whole Grain Processing, and Other:

- Rice Processing: Largest segment (approximately 80%), including white rice production, parboiled rice milling, and premium rice processing

- Whole Grain Processing: Brown rice and specialty grain applications

- Other: Small-scale and artisanal rice milling

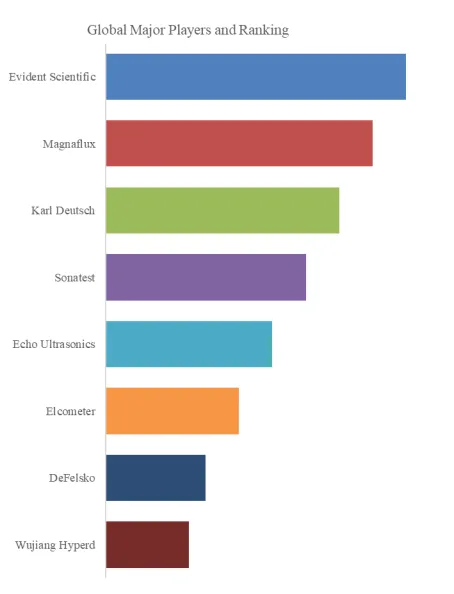

Competitive Landscape: Key Players

The emery roller rice mill market features global grain processing equipment leaders and regional Chinese manufacturers:

| Company | Key Strengths |

|---|---|

| Bühler Group | Global grain processing leader; high-capacity integrated mills |

| Satake Corporation | Japanese rice milling specialist; precision technology |

| Hubei Yongxiang | Chinese manufacturer; domestic market leadership |

| Hubei Fotma, Hunan Chenzhou Grain & Oil Machinery, Hubei Tianhe | Regional Chinese manufacturers; cost-competitive solutions |

| Shandong Jinglianghaiwei, Changzhou Wujin Huanqiu Grain Machinery, Hubei Bishan Machinery, Zhejiang Qili Machinery | Specialized rice milling equipment manufacturers |

Recent Developments (Last 6 Months)

Several developments have shaped the emery roller rice mill market:

- Rice Mill Modernization: December 2025–January 2026 saw continued investment in rice milling infrastructure in major rice-producing countries (India, Vietnam, Thailand, China), driving demand for higher-capacity and higher-precision mills.

- Premium Rice Demand: Growing consumer demand for premium white rice and high-precision milling (90–95% polished) increased adoption of emery roller mills for final polishing stages.

- Energy Efficiency: New mill designs with improved drive systems and reduced power consumption per ton of paddy processed, addressing operating cost concerns.

- Indica Rice Processing: Expansion of long-grain indica rice cultivation and export (India, Vietnam) driving demand for emery roller mills suitable for high-strength rice varieties.

Exclusive Insight: Vertical vs. Horizontal Emery Roller Mills—Space vs. Throughput

A critical market dynamic is the divergence between vertical and horizontal emery roller mill configurations based on facility constraints and throughput requirements.

Vertical Sand Roller Mills (growing segment for smaller facilities) are characterized by:

- Compact Footprint: Smaller floor space requirement

- Easier Maintenance: Vertical orientation simplifies roller access

- Lower Throughput: Typically 0.5–3 tons per hour

- Applications: Small to medium rice mills, retrofit installations, specialty rice processing

Horizontal Sand Roller Mills (larger segment for commercial mills) are characterized by:

- Higher Throughput: 3–15+ tons per hour

- Continuous Operation: Better suited for high-volume commercial milling

- Larger Footprint: Requires more floor space

- Applications: Large-scale commercial rice mills, integrated rice processing plants

A 2026 industry analysis indicated that horizontal mills dominate large-scale commercial installations due to throughput advantages. Vertical mills maintain strong presence in smaller facilities and retrofit markets where space is constrained.

Technical Challenges and Innovation Directions

Key technical considerations in emery roller rice mill development include:

- Temperature Control: Managing rice kernel temperature rise during milling to prevent cracking and quality degradation

- Roller Wear: Emery grit degradation over time affecting milling consistency; replacement intervals typically 500–2,000 operating hours

- Yield Optimization: Balancing bran removal efficiency with kernel breakage prevention

- Energy Consumption: Power requirements for high-speed abrasive milling

Innovation focuses on:

- Improved Abrasive Materials: Longer-lasting emery formulations for extended roller life

- Temperature Management: Integrated cooling systems to reduce kernel temperature rise

- Automated Control: Sensor-based pressure and speed adjustment for consistent milling quality

- Hybrid Mills: Combining emery rollers with rubber roller hullers for optimized processing

Conclusion

The emery roller rice mill market is positioned for steady growth through 2032, driven by rice consumption, milling infrastructure modernization, and demand for high-precision rice products. For manufacturers, success will depend on milling efficiency, durability (roller life), and the ability to serve both vertical and horizontal configuration markets. As global rice consumption rises and consumers demand higher-quality milled rice, emery roller rice mills will remain essential equipment for commercial rice processing.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp