QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Economics of Pet- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Economics of Pet market, including market size, share, demand, industry development status, and forecasts for the next few years.

The global market for Economics of Pet was estimated to be worth US$ million in 2024 and is forecast to a readjusted size of US$ million by 2031 with a CAGR of %during the forecast period 2025-2031.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/4394456/economics-of-pet

1. Economics of Pet Market Summary

The Economics of Pets encompasses all commercial activities related to pets throughout their entire life cycle, including production, sales, and services. Essentially, it’s the industrialization of emotional consumption, driven by the profound shift in pets’ roles in modern society from “functional companions” to “emotional anchors” and “family members.” This economic model covers essential needs and services such as pet food, supplies, veterinary care, grooming, training, insurance, and funeral services, and extends to emerging anthropomorphic consumption areas like pet photography, smart technology, tourism, and social interaction, forming a vast and continuously expanding industrial chain. Because it’s rooted in deep emotional bonds, the pet economy typically exhibits strong consumer rigidity, counter-cyclicality, and high growth potential, while also posing new demands on industry standards, social management, and responsible pet ownership.

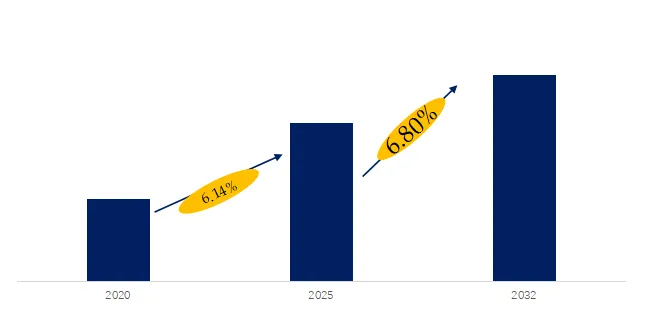

According to the latest research report from QYResearch, in terms of market size, the global Economics of Pet market size is projected to grow from USD 320 billion in 2025 to USD 339 billion by 2032, at a CAGR of 6.80% during the forecast period.

Figure00001. Global Economics of Pet Market Revenue Growth Rate, 2021-2032

Above data is based on report from QYResearch: Global Economics of Pet Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

2 Introduction of Major Manufacturers of Economics of Pet

| Serial Number |

Company |

| 1 |

Mars |

| 2 |

Colgate-Palmolive |

| 3 |

Diamond Pet Foods |

| 4 |

Petplan UK (Allianz) |

| 5 |

Go Pet Club |

| 6 |

North American Pet Products |

| 7 |

Heristo |

| 8 |

Nestle Purina |

| 9 |

Nationwide |

| 10 |

Trupanion |

| 11 |

J.M. Smucker |

| 12 |

Hartville Group |

| 13 |

Pethealth |

| 14 |

Kong |

| 15 |

Nylabone |

| 16 |

Jolly Pets |

| 17 |

JW Pet |

| 18 |

Pfizer |

| 19 |

Wellness |

| 20 |

John Morrell |

Source: Third-party data, QYResearch Research Team

According to a survey by QYResearch’s Leading Enterprise Research Center, global Economics of Pet manufacturers include Mars, Colgate-Palmolive, Diamond Pet Foods, Petplan UK (Allianz), Go Pet Club, etc. By 2025, the top five global manufacturers will hold approximately 25% of the market share.

Introduction to Key Companies

Company 1

| Mars |

Description |

| Company Introduction |

Mars is a leading global food manufacturer and pet care multinational company, founded in the United States in 1911. While known for its candies and chocolates like Dove and M&M’s, it has long built a vast pet empire through continuous acquisitions. Currently, pet care is its largest business segment, contributing approximately 60% of the company’s revenue. It owns over 50 well-known brands, including Royal Canin, Pedigree, Whiskas, Orijen, and Acana, with businesses covering pet food, nutritional supplements, and thousands of animal hospitals worldwide. |

| Product Introduction |

Mars’ pet economy is manifested in its creation of a complete ecological loop covering the needs of pets throughout their entire life cycle. Its core strategy is to meet diverse consumer demands, from mass-market to high-end, through a multi-brand matrix. More importantly, it integrates a full-chain service of “diagnosis-treatment-nutritional management”: it owns chain animal hospitals such as Banfield and VCA for treatment, conducts cutting-edge nutritional science research through the Wilhelm Research Institute, and provides precise nutritional solutions through brands like Royal Canin. In the Chinese market, Mars deeply integrates local insights, such as launching specialized food for Corgis and actively promoting social responsibility projects such as “pet-friendly cities.” |

Source: Third-party data, QYResearch Research Team

Company 2

| Colgate-Palmolive |

Description |

| Company Introduction |

Colgate-Palmolive, a long-established global consumer goods giant founded in 1806 and headquartered in New York City, USA, initially gained fame for its toothpaste and soap production. Over the years, its core business has stabilized and focused on four main categories: oral care, personal care, home care, and pet nutrition. Its products reach consumers through a sales network spanning over 200 countries and regions worldwide, and it owns numerous well-known brands such as Colgate and Palmolive. While traditional consumer goods form the basis of its public image, pet nutrition has become one of the company’s most important and fastest-growing business segments. |

| Product Introduction |

Colgate-Palmolive’s pet economy business is primarily operated through its wholly-owned subsidiary, Hill’s Pet Nutrition. Hill’s is a global leader in the pet food industry, with a core product strategy of “science-driven nutrition,” emphasizing premium, professional formulas. Its product line is primarily led by “Hill’s Science Diet” and “Hill’s Prescription Diet,” the latter requiring veterinary guidance and providing nutritional solutions for specific pet health issues. The company consolidates its scientific authority and high-end market position through continuous R&D investment and strategic acquisitions. Operationally, Hill’s is proactively optimizing its product portfolio, gradually exiting low-profit private-label businesses, and focusing entirely on high-value-added scientifically formulated products, thereby driving a significant improvement in profitability. |

Source: Third-party data, QYResearch Research Team

Company 3

| Diamond Pet Foods |

Description |

| Company Introduction |

Diamond Pet Foods is one of the leading pet food companies in the United States, ranking as the sixth largest pet food manufacturer globally and among the top three in the US. The company’s core business is producing high-quality pet staple food, and it owns several well-known brands. Through strict quality control, a pursuit of natural and high-quality ingredients, and deep cultivation of professional channels, it has established a solid market reputation. Its products have been repeatedly recommended by the authoritative American pet magazine, *Whole Dog Journal* (WDJ). |

| Product Introduction |

The company’s flagship pet economy product is its high-end brand, “Taste of the Wild.” This brand perfectly aligns with the core concepts of “consumption upgrade” and “natural health” in the pet economy. Its products emphasize the use of high-quality animal protein, grain-free formulas, no artificial additives, and mimicking the natural diet of wild carnivores. To meet the demands of the high-end market, “Taste of the Wild” selects ingredients from three continents and the polar regions around the world, using “high meat content” and “staple food-grade nutrition” as its core selling points. It aims to provide pets with a diet closer to nature and richer in nutrients, thus winning the favor of pet owners who value quality. |

Source: Third-party data, QYResearch Research Team

3 Economics of Pet Industry Chain Analysis

| Industry Chain |

Description |

| Upstream |

The upstream of the Economics of Pet industry chain is the foundation and source of the industry, with its core function being to provide the necessary raw materials for the entire industry and transform these raw materials into end products. This link mainly includes two major segments: First, the supply of basic raw materials, involving agricultural products, livestock and poultry meat and by-products, and fish needed for pet food production, as well as chemical raw materials, textile fabrics, and electronic components needed for pet product manufacturing. Second, the research and development and manufacturing of core products, where numerous manufacturers utilize these raw materials to develop formulas, design, and mass-produce various physical goods such as pet staple food, snacks, nutritional supplements, pet toys, bedding, clothing, and cleaning tools. The technological level, scale, cost, quality and safety, and supply chain stability of upstream enterprises directly determine the product strength and market competitiveness of midstream brand owners, and are the starting point of the entire industry chain’s value. |

| Midstream |

The midstream of the Economics of Pet industry chain undertakes the core hub functions of value enhancement, market connection, and commodity circulation. The main players in this segment are various brand owners, agents, wholesalers, and online and offline retail channels. Brand owners occupy a key position, sourcing or outsourcing products from upstream suppliers. Through market research, brand positioning, marketing planning, and packaging design, they transform products into goods with clear consumer recognition and premium pricing, such as international brands like Royal Canin and Mars, or emerging domestic brands. Subsequently, the goods reach final sales touchpoints through distribution networks. The distribution channels are diversified, including specialized pet stores and pet hospital retail areas; large supermarkets and convenience stores; and increasingly important e-commerce platforms, brand-operated online stores, and live-streaming e-commerce. The midstream segment, through brand operation and channel development, directly addresses consumer needs and is crucial in determining market trends and consumer reach efficiency. |

| Downstream |

The downstream of the pet industry chain directly provides end-user services and experiences to pet owners and their pets. Its core characteristics are high professionalism, localization, and emotional interaction. This segment constitutes a comprehensive service support system for pets throughout their lives, mainly including: medical and health services; daily living services; specific industry services; and emerging derivative services. Downstream service providers rely not only on professional equipment and knowledge but also on the emotional bond of trust established with pet owners. Furthermore, social media, content platforms, and review communities that connect consumer communities are also downstream derivatives. They influence consumer decisions and cultivate pet-owning culture, thus contributing back to the entire industry chain. The downstream sector is the final stage of realizing industry value and a major frontier for consumption upgrading and experience innovation. |

Source: Third-party data, QYResearch Research Team

4 Economics of Pet Industry Development Trends, Opportunities, Obstacles and Industry Barriers

Development Trends:

1. The core of consumption has shifted from “basic feeding” to “emotional and family role fulfillment.” The core driver of the pet economy is no longer satisfying the survival needs of animals, but rather fulfilling the emotional projection and identity that pet owners feel when they consider their pets as family members. This has given rise to “anthropomorphic” consumption, with owners willing to pay a premium to improve their pets’ health, happiness, and quality of life. This consumption covers a full range of lifestyle scenarios, from high-end food and fashion items to photography, travel, and pet-friendly restaurants, giving the industry strong counter-cyclical resilience and continuous upgrading momentum.

2. Products and services are evolving towards greater personalization, intelligence, and functionality. On the product side, pet nutrition is moving from life stage and breed segmentation to precise customization based on specific health needs, even including food customized based on pet genetics or health check data. Meanwhile, smart feeders, water fountains, litter boxes, and health monitoring devices are transforming from novelty products into essential pet infrastructure, integrating with the Internet of Things and AI to provide automated care and health alerts. The market for functional snacks and supplements is also expanding rapidly.

3. The industry focus is shifting from products to professional services and full life-cycle management. Pet healthcare has become one of the fastest-growing and highest-value-added sectors, driving the entire industry chain from prescription food and physical examinations to surgery and subsequent rehabilitation. Pet insurance has emerged to mitigate the risk of high medical expenses. Furthermore, service industries covering the entire lifecycle of pets—from birth to death—are becoming increasingly mature and professional, encompassing behavioral training, pet funerals, pet hotels, and even pet psychological counseling, forming new high-value areas in the industry.

Development Opportunities:

1. Emerging markets, particularly in the Asia-Pacific region, are becoming core engines of global growth. Asian markets, represented by China, benefit from a large young pet-owning population, rapidly increasing penetration rates, and a strong desire for consumption upgrades. Their e-commerce penetration rate is already leading globally, providing fertile ground for new product launches. Meanwhile, pet culture is emerging in Southeast Asia and the Middle East, with low initial pet ownership rates but rapid growth, offering a vast blue ocean market for international brands and Chinese companies with supply chain advantages. The competitive landscape is not yet solidified.

2. The deep integration of the online economy and content marketing has created entirely new brand building and sales paths. Social media, short videos, and live streaming platforms are not only product showcases but also key venues for shaping pet-owning knowledge, cultivating consumer culture, and creating visual appeal. The DTC (Direct-to-Consumer) model, leveraging e-commerce platforms and private domain traffic, allows emerging brands to bypass traditional offline channel barriers, quickly understand needs, test products, and build user loyalty, thereby disrupting the traditional market structure dominated by giants.

3. Increased focus on pet health and welfare has opened up huge opportunities in high-end food, insurance, and preventative medicine. With the popularization of scientific pet care concepts, owners’ pursuit of longevity and quality of life for their pets has directly driven the booming market for high-end natural pet food, functional prescription pet food, and nutritional supplements. Correspondingly, pet insurance penetration is already high in Europe and America, but it is still in its infancy in most emerging markets, with huge future growth potential. Preventative medical care is also shifting from an optional consumption to a necessity.

Hindering Factors:

1. Macroeconomic fluctuations and inflation directly weaken consumer willingness and ability to consume. Global economic pressures have led to a contraction in disposable income for consumers in some markets, potentially causing them to turn to more cost-effective options when facing pet-related daily expenses, postponing or canceling non-essential services and high-end product purchases. Rising raw material costs, energy prices, and international logistics costs continue to squeeze the profit margins of manufacturers, forcing them to make difficult choices between raising prices and maintaining market share, impacting the overall profitability of the industry.

2. Intense competition within the industry leads to severe involution, putting pressure on innovation and profits. Especially in the pet food and supplies sector, a large number of new brands have entered the market, resulting in severe product homogenization. Price wars have become a common tactic to compete for traffic and market share, which not only erodes reasonable corporate profits but may also lead to reduced investment in R&D and quality control, creating a potential “bad money drives out good” risk, which is detrimental to the long-term healthy development and technological innovation of the industry.

3. Geopolitical and trade policy uncertainties bring supply chain risks. International trade frictions and changes in tariff policies may suddenly alter cross-border logistics costs and market access conditions, directly impacting companies that rely on global supply chains for raw material procurement or engage in export business. Companies are forced to consider regionalizing their supply chains or relocating production bases, which brings significant additional capital expenditures and operational complexity, increasing the difficulty and uncertainty of operating in global markets.

Barriers:

1. Building lasting brand trust and consumer perception is extremely difficult. Pet products, especially food, are related to the health and safety of companion animals, and consumers make highly cautious decisions based on trust. New brands need to invest significant time and resources to build credibility through consistent product quality, safety records, scientific endorsements, and word-of-mouth marketing. Breaking into the market is a huge challenge given that established giants have firmly established themselves in mainstream channels and consumer mindshare.

2. Strict technical, R&D, and regulatory barriers exist in core areas. The R&D of pet food and pet medications involves complex sciences such as animal nutrition and pathology, requiring substantial R&D investment and clinical validation. Smart hardware involves software and hardware development, data algorithms, and product reliability. Furthermore, various countries have complex registration, certification, and labeling regulations for imported pet food, medications, and appliances. New entrants need expertise and a lengthy process to meet compliance requirements, creating a substantial barrier to entry.

3. Breaking through established offline distribution channels and service networks is difficult. In mature markets such as Europe and the United States, mainstream supermarkets, professional pet chain stores, and veterinary clinics are already dominated by major brands, leaving limited shelf space. New brands face high costs and lengthy negotiation periods to enter the market. Furthermore, building a proprietary professional service system requires substantial capital investment, a pool of professional talent, and long-term operational experience, making it a challenging endeavor for most companies.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading Global market research and consulting company. With over 16 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are Globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Economics of Pet market is segmented as below:

By Company

Mars

Go Pet Club

Diamond Pet Foods

Petplan UK (Allianz)

Colgate-Palmolive

North American Pet Products

Heristo

Nestle Purina

Nationwide

Trupanion

J.M. Smucker

Hartville Group

Pethealth

Kong

Nylabone

Jolly Pets

JW Pet

Pfizer

Wellness

John Morrell

Segment by Type

Food

Toy

Furniture

Health Products

Others

Segment by Application

Dog

Cat

Aquatic

Birds

Rodents

Others

Each chapter of the report provides detailed information for readers to further understand the Economics of Pet market:

Chapter 1: Introduces the report scope of the Economics of Pet report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Economics of Pet manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Economics of Pet market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Economics of Pet in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Economics of Pet in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Economics of Pet competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Economics of Pet comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Economics of Pet market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Economics of Pet Market Outlook, In‑Depth Analysis & Forecast to 2031

Global Economics of Pet Sales Market Report, Competitive Analysis and Regional Opportunities 2025-2031

Global Economics of Pet Market Research Report 2025

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp