Mobile Screening Equipment Market Summary

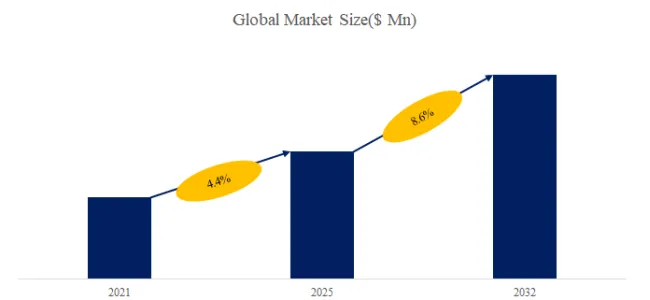

According to the latest report “Global Mobile Screening Equipment Market Report 2025-2031″ by the QYResearch research team, the global Mobile Screening Equipment market size is expected to reach US$218.25 billion in 2031, with a compound annual growth rate (CAGR) of 8.6% in the next few years.

Mobile screening equipment refers to screening machinery endowed with self-propelled capabilities or the capacity for convenient relocation; typically mounted on crawler tracks, wheels, or towable chassis, it integrates feeding, screening, and conveying units into a single cohesive system. Its core essence lies in “mobility” and “integration”—requiring no fixed foundation, it can be rapidly transferred between different work sites and put into immediate operation upon arrival. Compared to traditional stationary screening lines, it eliminates the need for civil engineering works and extensive conveyor belt connections, making it particularly well-suited for projects requiring multi-site operations or involving short construction schedules—such as sand and gravel mining, construction waste processing, and topsoil stripping. Primarily powered by diesel engines, this equipment operates autonomously and is characterized by its operational flexibility, low relocation costs, and rapid deployment capabilities, establishing itself as a pivotal asset in the modern fields of aggregate production and solid waste resource utilization.

The market for mobile screening equipment is currently experiencing a dual-growth phase, driven by both “engineering demand” and “catalytic environmental policies.” The core logic underpinning this growth lies in the equipment’s ability to replace traditional fixed screening models and enhance operational efficiency at job sites. On one hand, global demand for infrastructure construction, mining operations, and sand and aggregate materials continues to expand. Particularly against the backdrop of shortened project cycles and increased requirements for construction flexibility, mobile equipment is rapidly gaining market penetration—capitalizing on its key advantages of being “ready-to-use upon arrival” and requiring no complex civil engineering works. On the other hand, increasingly stringent policies regarding the recycling of construction waste and the treatment of solid waste are driving a significant surge in demand for the screening of recycled aggregates, thereby becoming a major source of incremental growth for the industry.

In terms of technological trends, the equipment is evolving toward electrification (replacing diesel-only propulsion), intelligent control systems (enabling remote monitoring and fault diagnostics), and modular design configurations. Concurrently, the development of integrated solutions—combining mobile screening units with mobile crushing equipment—has emerged as a primary competitive differentiator in the market.

In the short term, industry demand remains highly susceptible to the pace of infrastructure investment and fluctuations within the real estate cycle. However, from a medium-to-long-term perspective—and set against the broader context of green mining initiatives, recycled resource utilization, and global infrastructure modernization—mobile screening equipment demonstrates robust growth resilience. This is particularly evident in emerging markets across Asia, Africa, and Latin America, where there remains significant room for market expansion.

The growth of the mobile screening equipment sector is primarily driven by a confluence of factors, including expanding downstream demand and ongoing industrial upgrades.

First, the continuous advancement of infrastructure construction and mineral resource development—specifically major road, railway, and urban development projects—is fueling a rise in demand for sand and aggregate materials. This trend underscores the critical value of mobile screening equipment in facilitating rapid on-site screening and efficient resource utilization.

Second, increasingly stringent environmental regulations are compelling enterprises to minimize material transport and dust emissions. Mobile equipment addresses this challenge by enabling on-site processing and resource recycling, thereby significantly reducing environmental impact and accelerating the transition away from traditional fixed screening systems.

Third, technological innovation serves as a pivotal growth driver. Advancements such as modular design, diesel-electric hybrid power systems, remote monitoring capabilities, and intelligent control systems have substantially enhanced both the operational efficiency of the equipment and its capacity to adapt to complex working conditions. Furthermore, the broader shift in construction methodologies toward greater flexibility and decentralization has heightened the preference for equipment characterized by high mobility and rapid deployment capabilities.

Additionally, rising labor costs are prompting enterprises to adopt screening equipment with higher levels of automation in order to boost overall efficiency. Finally, the emergence of equipment leasing models has lowered the barriers to entry for equipment usage, enabling small and medium-sized enterprises (SMEs) to participate in the market and thereby further broadening the overall demand base. Overall, demand growth, environmental pressures, technological advancements, and business model innovations are collectively driving the continued development of the mobile screening equipment market.

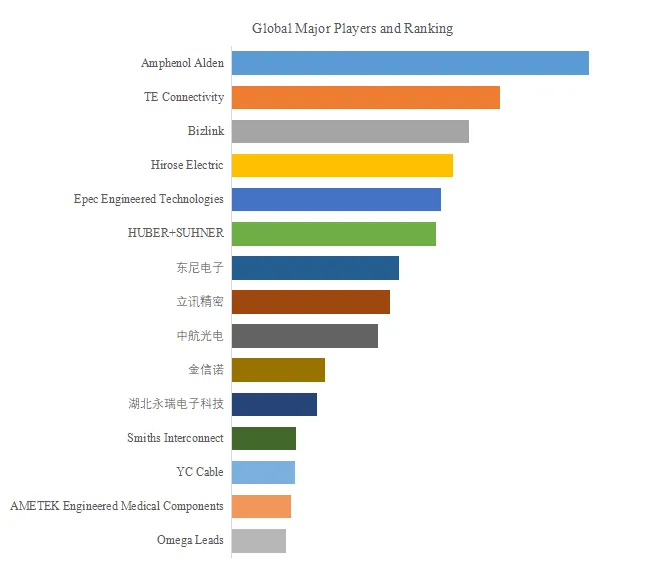

This report profiles key players of Mobile Screening Equipment such as TSX Screen、RoadSky、AIMIX Group、Rubble Master、Fujian South Road Machinery Co., Ltd.、Fabo Company、NM Heilig、MT Royal、MINEVATE、VICKEY、Zhengzhou Anbang Machinery Technology Co., Ltd.、Shanghai Dongmeng ROAD&BRIDGE Machinery Co., Ltd.、Liming Heavy Industry、Baichen Heavy Industry Machinery

The industrial chain for mobile screening equipment constitutes a comprehensive industrial system, commencing with the supply of raw materials, centering on the manufacturing of complete machines, and driven by end-use applications. Each link within this chain is intricately interconnected, collectively underpinning the development of sectors such as mining, construction solid waste processing, and sand and aggregate production. The following discussion elaborates on this structure in detail, examining the upstream, midstream, and downstream segments.

Upstream of the Industrial Chain: Supply of Raw Materials and Core Components.

The upstream segment of the industrial chain primarily supplies various raw materials and core components required for the manufacture of mobile screening equipment. The supply landscape and technological sophistication of this segment directly determine the performance, reliability, and production costs of the complete machines.

Regarding upstream raw materials, high-strength, wear-resistant steel serves as the primary material for the equipment’s main body, screen box, chassis, and structural components; its cost accounts for a significant proportion of the complete machine’s overall cost structure. This type of steel must possess exceptional wear resistance and structural strength to withstand the continuous vibrations and material impacts inherent in screening operations.

Core components constitute the technological heart of the equipment, principally comprising vibrating motors, alloy springs, control systems, and hydraulic systems. Among these, the vibrating motor is the critical component responsible for generating the screening power, directly determining screening efficiency and stability; alloy springs serve to absorb shock and provide structural support; and the control system manages the automated operation and condition monitoring of the entire machine.

Furthermore, the power system represents another vital element of the upstream segment. Depending on the specific equipment type, mobile screening units may be driven by diesel engines, electric motors, or a dual-power hybrid system. Diesel-driven systems are well-suited for field operations in locations lacking access to grid power, while electric-driven systems offer greater environmental friendliness and energy efficiency; dual-power systems combine the operational flexibility of both approaches. The technological level of these upstream power systems directly impacts the equipment’s operational adaptability and energy consumption performance.

Technological barriers within the upstream segment are primarily manifested in areas such as the R&D of high-performance wear-resistant materials, the precision manufacturing of core vibrating components, and the development of intelligent control systems. As screening equipment evolves toward larger scales and greater intelligence, the technological demands placed upon upstream suppliers continue to rise.

Midstream of the Industrial Chain: Complete Machine Manufacturing and Market Competitive Landscape.

The midstream segment of the industrial chain serves as its core, encompassing the design, R&D, manufacturing, sales, after-sales service, and brand management of mobile screening equipment. This segment is home to the world’s—as well as China’s—leading manufacturers, giving rise to a multi-tiered and differentiated competitive landscape. From a global market perspective, the mobile screening equipment industry is characterized by the coexistence of international giants and outstanding domestic enterprises. Leveraging their deep technical expertise, comprehensive global service networks, and powerful brand influence, these companies have long dominated the high-end market segment.

In recent years, domestic Chinese manufacturers have experienced rapid growth and have emerged as a significant force in the global mobile screening equipment market. Through continuous technological innovation and cost advantages, these companies have secured leading positions in the mid-range market while actively expanding into the high-end sector. Furthermore, some enterprises have developed specialized products tailored to domestic market demands—specifically designed to adapt to complex operating conditions and meet stringent environmental protection requirements.

In terms of product types, mobile screening equipment can be broadly categorized into three main types based on their power source: diesel-driven, electric-driven, and dual-power-driven. Diesel-driven models are suitable for off-grid field operations and currently represent the most widely utilized type. Electric-driven models offer lower operating costs and superior environmental performance, making them ideal for job sites with access to a stable power supply. Dual-power-driven models combine the advantages of both systems, allowing for flexible switching based on specific on-site conditions.

In the midstream manufacturing segment, the focus of competition is shifting away from mere price competition toward competition centered on technology and service. Intelligent control systems, remote operation and maintenance capabilities, energy-saving and eco-friendly technologies, and comprehensive lifecycle after-sales services are becoming the key strategic directions for companies seeking to build their core competitiveness.

Downstream of the Value Chain: Application Fields and End Customers.

The downstream segment of the value chain comprises the application market for mobile screening equipment, encompassing various operational scenarios involving material screening, classification, impurity removal, and dewatering. The scale and structural composition of downstream demand directly determine the overall development trajectory of the entire industry value chain.

In terms of application fields, the mining industry constitutes the largest market for mobile screening equipment. These units are primarily utilized for the classification and screening of ore following crushing, preliminary screening prior to mineral processing, and the dewatering of tailings. In mining operations, mobile screening equipment can be flexibly relocated as the mining face advances, thereby significantly reducing ore transportation costs.

The construction sector represents another major application market, primarily encompassing two key areas: the production of sand and gravel aggregates, and the processing of construction solid waste. In the production of sand and gravel aggregates, mobile screening equipment is utilized to classify crushed stone materials, yielding finished aggregates of various particle sizes. In the processing of construction and demolition waste, this equipment screens materials—such as concrete blocks and bricks generated during demolition—into recyclable aggregates, serving as a pivotal tool for the resource-efficient utilization of construction waste.

The environmental protection sector is rapidly emerging as one of the fastest-growing application markets. As national priorities increasingly emphasize the prevention and control of solid waste pollution as well as resource recycling, the application of mobile screening equipment is becoming ever more widespread across scenarios such as municipal waste sorting, renovation waste processing, and soil remediation. Its inherent characteristics—specifically its flexibility in site transfer and rapid deployment capabilities—make it particularly well-suited for decentralized solid waste processing projects.

From the perspective of end-users, downstream customers primarily comprise large-scale mining corporations, cement and building material manufacturers, construction firms, solid waste management operators, and various engineering contractors. These clients place high demands on the equipment regarding reliability, production efficiency, environmental performance, and service support.

Geographically, China, North America, Europe, and Australia constitute the world’s major consumer markets for mobile screening equipment. As the world’s largest producer of sand and gravel aggregates and its largest construction market, China maintains a consistently robust demand for mobile screening equipment, serving as a key driving force behind global market growth.

Looking ahead, the mobile screening equipment industry chain is evolving toward greater intelligence, sustainability, large-scale capacity, and service-oriented integration.

On the technological front, intelligence stands as the core direction of development. By integrating sensors, IoT technologies, and big data analytics, the new generation of mobile screening equipment enables real-time operational monitoring, fault pre-warning systems, remote diagnostics, and automated adjustments—thereby significantly boosting operational efficiency and equipment uptime. Concurrently, energy-saving and eco-friendly technologies are garnering increasing attention; designs featuring low energy consumption, dust suppression and noise reduction technologies, and the application of new energy power sources are becoming key directions for product upgrades.

At the market level, the integration of the industry chain and a transition toward service-oriented models represent the primary trends. Leading manufacturers are shifting their focus from the mere sale of standalone equipment to providing integrated “equipment-plus-service” solutions, offering comprehensive lifecycle services that encompass equipment leasing, outsourced operation and maintenance, spare parts supply, and the buyback of pre-owned equipment. Furthermore, driven by the deepening implementation of national “Dual Carbon” strategies, sectors such as the resource-efficient utilization of construction waste and the development of green mines are expected to generate sustained market growth opportunities for mobile screening equipment.

Overall, the industrial chain for mobile screening equipment is currently undergoing a critical transition—shifting from a phase of scale expansion to one of quality enhancement. Breakthroughs in the localization of key upstream components, intelligent upgrades in midstream manufacturing processes, and the green expansion of downstream application sectors collectively constitute the central theme for the industry chain’s future development.

The competitive landscape for mobile screening equipment is characterized by the following features:

From a segmented perspective, the high-end market is dominated by European and North American enterprises, which leverage their mature capabilities in complete machine design, core component technology, and brand influence. Their products prioritize high processing capacity, operational stability, and advanced intelligence, primarily serving large-scale mining operations, aggregate producers, and multinational engineering projects. The mid-range market consists of regional manufacturers possessing a certain level of technological expertise; these firms strike a balance between performance and cost-effectiveness, with their products widely utilized in medium-sized mines, construction waste processing, and infrastructure projects. Conversely, the low-end market is characterized by a multitude of participants and significant product homogeneity, where players primarily rely on price advantages and rapid delivery capabilities to secure orders.

From a regional standpoint, the European and North American markets exhibit high concentration and distinct brand barriers. In contrast, the Asia-Pacific region—particularly China—features a larger number of enterprises and a more fragmented competitive environment; however, in recent years, companies in this region have made rapid strides in complete machine integration and cost-performance ratios, thereby gradually penetrating the mid-to-high-end markets.

Overall, the industry presents a landscape in which “the high-end market is dominated by international brands, while the mid-to-low-end markets are characterized by fierce competition and the accelerated rise of domestic enterprises.” Looking ahead, as equipment trends toward larger scale, greater intelligence, and eco-friendly energy efficiency, companies possessing core technologies and comprehensive system solution capabilities are poised to further expand their market share, and the overall industry concentration is expected to gradually increase.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp