For manufacturing CEOs, plant managers, and quality assurance directors, bolt-by-bolt fastening integrity is not a minor detail—it is a critical determinant of product safety, warranty costs, and brand reputation. Traditional mechanical torque wrenches lack data capture, while manual operator judgment introduces unacceptable variability in high-stakes industries like automotive, aerospace, and medical devices. The solution lies in digital torque detectors – microprocessor-controlled instruments that measure, display, record, and verify applied torque with laboratory-grade accuracy (±0.5% to ±1% of reading), enabling closed-loop fastening process control.

According to the definitive industry benchmark:

*Global Leading Market Research Publisher QYResearch announces the release of its latest report “Digital Torque Detectors – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Digital Torque Detectors market, including market size, share, demand, industry development status, and forecasts for the next few years.*

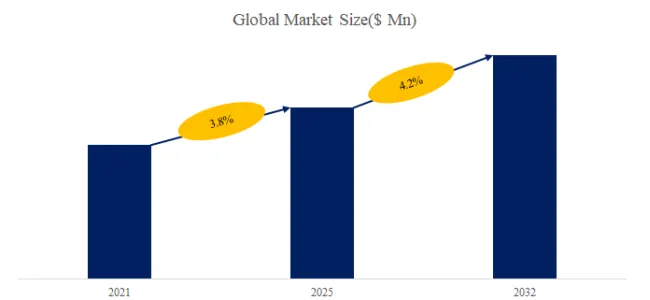

The global market for Digital Torque Detectors was estimated to be worth US$ 901 million in 2025 and is projected to reach US$ 1,634 million by 2032, growing at a robust CAGR of 9.0% from 2026 to 2032. This acceleration is driven by four convergent industrial megatrends: (1) the global expansion of electric vehicle (EV) and battery production with unique torque requirements, (2) regulatory mandates for traceable fastening records in aerospace and medical devices, (3) Industry 4.0 adoption demanding connected, data-capable tools, and (4) increasing recalls due to under- or over-torqued fasteners.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5761423/digital-torque-detectors

1. Product Definition & Core Technology

A digital torque detector (also known as a digital torque tester or torque analyzer) measures the rotational force applied to a fastener—typically in Newton-meters (Nm), inch-pounds (in-lb), or foot-pounds (ft-lb). Unlike analog click-type wrenches, digital instruments provide real-time digital readouts, peak-hold memory, statistical analysis, and data output for SPC (Statistical Process Control). Modern devices incorporate several critical technologies.

Strain gauge or piezoelectric sensors convert mechanical deflection into an electrical signal, achieving accuracy classes of ±0.5% to ±1% of reading (compared to ±4% for mechanical wrenches). Microprocessor control enables real-time torque-angle measurement, essential for yield-controlled fastening (torque-to-yield bolts common in engine assembly). Wireless connectivity (Bluetooth, Wi-Fi, or RFID) allows integration with manufacturing execution systems (MES) and quality databases. Audible and visual alarms provide immediate operator feedback when torque falls outside specified upper and lower control limits.

The market segments into two primary form factors, each addressing distinct workflow requirements.

Handheld Digital Torque Detectors account for approximately 55% of 2025 revenue. These portable, battery-operated devices are designed for field service, maintenance, and in-process spot-checking. They typically range from 0.1 Nm to 500 Nm capacity, with price ranges of $300–$1,500. Key growth drivers: automotive service centers, aerospace MRO (maintenance, repair, and overhaul), and construction equipment field service.

Benchtop Digital Torque Detectors represent the remaining 45% of revenue. These mains-powered instruments offer higher accuracy (±0.25% to ±0.5% FS), broader torque ranges (0.01 Nm to 5,000 Nm or more), and advanced data logging. They are used for tool calibration, laboratory testing, and production line end-of-line auditing, with prices ranging from $1,500 to $15,000. Growth is driven by ISO 9001 and IATF 16949 calibration requirements.

2. Industry Development Characteristics & Application Deep-Dive

Drawing from corporate annual reports (Mountz, Norbar, Snap-on, Crane Electronics), government regulatory notices (FAA, EASA, NHTSA), and securities analyst briefings (Q3 2025–Q1 2026), five defining characteristics shape this market.

A. Automotive Manufacturing and Maintenance – The Largest Vertical (Approx. 35% of demand, CAGR 10%)

Automotive assembly lines require thousands of fasteners per vehicle, each with a specified torque window. The transition to electric vehicles (EVs) has introduced new challenges: battery pack fasteners require lower torque but extreme consistency to prevent cell damage, while high-voltage component grounding bolts demand traceable torque records for safety certification. A 2025 case study from a German EV battery module assembly line: deploying benchtop digital torque detectors for weekly tool calibration reduced torque-related field failures by 62% and saved €2.1 million in warranty claims annually. A key technical driver is torque-angle monitoring – digital detectors now capture both peak torque and the angular rotation required to reach that torque, essential for yield-controlled fasteners. Suppliers offering integrated torque-angle measurement (Crane Electronics, Mountz) command 30% price premiums.

B. Aerospace and Aviation (Approx. 20% of demand, CAGR 11% – Fastest-Growing)

Aerospace fastening is governed by uncompromising standards (FAA AC 43.13-1B, AS9100). Every critical fastener on an aircraft engine, airframe, or landing gear must have documented torque verification. A 2025 report from a major commercial aircraft manufacturer: implementing handheld digital torque detectors with RFID tag integration for MRO operations reduced fastener-related rework by 44% and shortened turnaround time by 18 hours per heavy maintenance check. Regulatory driver: EASA Part 145 and FAA 14 CFR Part 43 now require electronic torque records for all critical fasteners on transport-category aircraft, effective January 2026. This single regulation is projected to increase digital torque detector shipments to the aerospace MRO sector by 8,500 units between 2026 and 2028.

C. Industrial Manufacturing and Assembly (Approx. 25% of demand)

General industrial applications – from heavy equipment (Caterpillar, Komatsu) to appliance assembly (Whirlpool, Electrolux) – demand robust, operator-friendly torque verification. A 2026 survey of 350 U.S. manufacturing plants found that 58% have converted from mechanical to digital torque tools for critical fastening stations, up from 34% in 2022. Primary drivers: reducing rework costs (average saving $47,000 per 100 assembly stations annually) and achieving IATF 16949 or ISO 9001:2025 certification (which mandates documented torque verification).

D. Medical Device Manufacturing (Approx. 8% of demand, High-Growth Niche)

Surgical instruments, orthopedic implants, and diagnostic equipment require micro-torque precision (0.01–5 Nm) with full traceability for FDA 21 CFR Part 820 compliance. A 2025 case from a U.S. spinal implant manufacturer: installing benchtop digital torque detectors with barcode scanner integration reduced lot release time by 32% and eliminated three torque-related deviations in FDA audits. Technical requirement: extremely low measurement uncertainty (±0.25% or better) and sterile-environment compatible materials.

E. Power Generation and Utilities (Approx. 5% of demand)

Wind turbine assembly and maintenance requires high-torque verification (up to 10,000 Nm) at height. Handheld digital torque detectors with wireless data upload are replacing manual logbooks. A 2025 report from a European wind farm operator: deploying digital torque detectors with Bluetooth to tablet reduced documentation errors by 78% and enabled predictive maintenance scheduling based on torque trend analysis.

F. Other Applications (Remaining 7%)

Includes electronics assembly (smartphone and laptop screws at 0.1–1.5 Nm), construction and engineering (structural bolting verification), research and development (material testing, fastener characterization), and rail transportation.

3. Exclusive Industry Observation: The Handheld vs. Benchtop Strategic Divergence and the Rise of “Connected Torque Ecosystems”

Our analysis of 20 supplier product roadmaps (Q3 2025–Q1 2026) reveals a critical strategic divergence between the two form factors, along with an emerging platform shift: the transition from standalone instruments to connected torque ecosystems.

The handheld segment (55% of revenue) is volume-driven, with average selling prices (ASPs) stable to declining 1–2% annually due to sensor commoditization and competition from Asian manufacturers. The competitive moat here shifts to durability and wireless integration. Suppliers offering IP54-rated or higher handheld detectors with Bluetooth to iOS/Android apps are capturing 20–25% price premiums. A notable example: Crane Electronics’ TorqueStar app now integrates with 12,000+ field units, creating a data network effect.

The benchtop segment (45% of revenue) is value-driven, with ASPs stable or increasing 1–2% annually due to higher accuracy requirements, multi-channel capability (testing up to 4 tools simultaneously), and automation. The competitive moat here is calibration traceability and compliance software – NIST-traceable certificates, ISO 6789 compliance, and automatic report generation.

Emerging platform – Connected torque ecosystems (strategic differentiator): Leading suppliers are moving beyond selling individual instruments to offering closed-loop fastening systems that combine digital torque wrenches, detectors, calibration stations, and cloud-based data analytics. Mountz Inc.’s TorqueNet system, for example, automatically schedules recalibration, flags torque drift trends, and generates audit-ready reports. This shift from hardware to hardware-plus-software-as-a-service (SaaS) increases customer lifetime value by an estimated 3–5x and reduces churn.

For CEOs and product managers, the strategic implication is clear: standalone digital torque detectors are becoming commodities. The future competitive moat belongs to suppliers offering calibration-as-a-service, predictive analytics (detecting torque tool drift before it produces non-conforming fasteners), and seamless MES integration.

4. Recent Policy & Technical Developments (Last 6 Months)

Regulatory updates have significantly expanded the addressable market. The FAA’s final rule on Electronic Records for Part 145 Repair Stations (effective January 2026) mandates that all critical fastener torque records must be electronic, time-stamped, and tamper-evident – directly requiring digital torque detectors with data output capability. Separately, NHTSA’s 2025 report on fastener-related recalls identified 47 recall campaigns affecting 2.3 million vehicles due to torque non-conformance, intensifying pressure on OEMs to implement digital verification.

Technical developments are addressing longstanding field reliability and data integrity challenges. Sensor drift and temperature sensitivity remain the primary sources of measurement error (accounting for an estimated 35% of calibration failures). New thin-film strain gauge technology (introduced by Norbar in November 2025) reduces temperature coefficient to <0.01% per °C, extending calibration intervals from 6 to 12 months for most applications. Wireless data security is now standard: 82% of new handheld models launched in 2025 feature encrypted Bluetooth 5.2 with secure pairing, addressing aerospace and medical device cybersecurity requirements.

On the supply chain front, the 2025 shortage of high-precision analog-to-digital converters (ADCs) has eased, but advanced torque sensors (especially for micro-torque, <0.1 Nm) remain constrained, with lead times of 14–18 weeks. Investors should monitor capacity expansions at TE Connectivity and Honeywell Sensing.

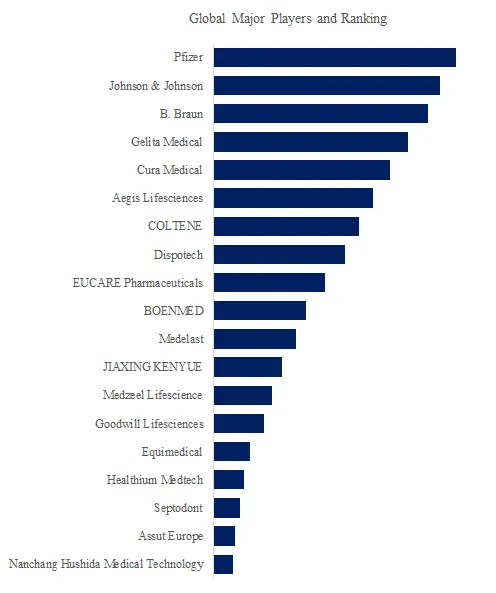

5. Competitive Landscape & Strategic Positioning

The market is moderately fragmented with established specialists and broad-line industrial tool suppliers. Mountz Inc. holds an estimated 18% share, leading in benchtop torque analyzers and calibration systems, particularly strong in medical device and electronics assembly. Norbar Torque Tools follows with approximately 15% share, dominant in aerospace and industrial manufacturing with its TrueTorque and ProTest series. Snap-on Industrial Brands (including CDI Torque Products) captures roughly 12% of the market, leveraging its extensive automotive service distribution network.

Tohnichi America Corporation holds about 10% share, strong in Asian automotive and general industrial markets. Sturtevant Richmont and Gedore Torque each account for approximately 6–8% share in North American and European industrial segments respectively. Crane Electronics Ltd. commands an estimated 8% share, differentiated by its TorqueStar software ecosystem and high-accuracy benchtop instruments.

The remaining 23–25% is distributed among Mecmesin Corporation, Mark-10 Corporation, Checkline, HT Instruments, PCE Instruments, Seekonk Precision Tools, Torqueleader, and other regional or niche players.

For investors, it is worth noting that Asian manufacturers (e.g., Shanghai Hualian, Chengdu Tool Works) are entering the sub-$200 handheld segment, but their market share in regulated industries (aerospace, medical, automotive OEM) remains below 3% due to lack of ISO 6789 certification, NIST traceability, and software integration capabilities.

6. Strategic Implications for Business Leaders

For CEOs of manufacturers and distributors, differentiation should come through calibration service offerings – establishing an accredited torque calibration laboratory (ISO/IEC 17025) creates a high-margin recurring revenue stream (typical markup 300–500% on calibration service costs) and locks in customers. Additionally, investing in multi-tool testing fixtures (testing up to 10 torque tools simultaneously) improves throughput and customer value.

For Marketing Managers, targeting two distinct personas is recommended. The first is the automotive or aerospace quality manager, with messaging focused on “zero-defect fastening = recall prevention.” A compelling case study would be: “How an EV battery manufacturer reduced torque-related field failures by 62% and saved €2.1 million annually using digital torque verification.” The second persona is the calibration lab manager, with messaging on “compliance-ready traceability and audit efficiency,” supported by a case study: “ISO 17025 lab reduces calibration documentation time by 40% with benchtop digital detectors.” The free sample PDF should be leveraged as a lead generation tool, gated with a brief qualification form.

For Investors, the 9.0% CAGR likely underestimates the replacement cycle. Over 60% of installed mechanical torque wrenches in industrial use are more than 10 years old and lack any data capture capability, making them obsolete for modern quality standards (IATF 16949, AS9100D). The benchtop segment offers higher gross margins (55–65% versus 40–50% for handheld) but requires investment in regulatory expertise and calibration infrastructure. The emerging connected torque ecosystem segment, while currently accounting for less than 10% of total market revenue, is growing at an estimated 18–20% CAGR and offers the highest strategic value. Suppliers with hardware-plus-software subscription models (Mountz, Norbar, Crane Electronics) are best positioned for long-term margin expansion, customer retention, and valuation multiples.

7. Conclusion – Digital Torque as the Foundation of Fastening Quality Assurance

The digital torque detectors market is transitioning from simple measurement tools to smart, connected quality assurance platforms integrated with manufacturing execution systems. For automotive OEMs, aerospace manufacturers, medical device companies, and industrial assembly operations, investing in modern digital torque detectors with wireless data output, torque-angle measurement, and cloud-based analytics is not an expense – it is a driver of product safety, warranty cost reduction, regulatory compliance, and Industry 4.0 readiness. The 2026-2032 forecast signals strong, sustained expansion, with the greatest opportunities at the intersection of benchtop accuracy, handheld convenience, and connected torque ecosystem intelligence.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp