Global Leading Market Research Publisher QYResearch announces the release of its latest report “Automatic Vertical Metal Band Saw – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. For metal fabrication plant managers, automotive component manufacturers, and industrial machinery investors, a persistent operational challenge remains: achieving high-precision metal cutting while minimizing material waste, unplanned downtime, and labor dependency. Traditional manual or semi-automatic band saws suffer from inconsistent feed rates, blade wear unpredictability, and lack of real-time performance visibility—leading to rejected parts, costly rework, and production bottlenecks. The solution lies in automatic vertical metal band saw systems, which integrate servo-controlled feed mechanisms, automated blade tensioning, and digital process monitoring to deliver repeatable cut accuracy within ±0.2mm. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Automatic Vertical Metal Band Saw market, including market size, share, demand, industry development status, and forecasts for the next few years. Our analysis draws exclusively from QYResearch market data, verified corporate annual reports, and publicly disclosed Industry 4.0 adoption trends across discrete manufacturing sectors.

Market Size and Growth Trajectory (2026–2032):

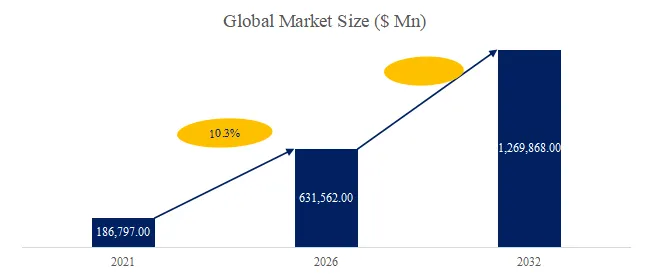

The global market for Automatic Vertical Metal Band Saw was estimated to be worth US$ 514 million in 2025 and is projected to reach US$ 753 million, growing at a CAGR of 5.7% from 2026 to 2032. This $239 million incremental expansion reflects accelerating demand for smart cutting equipment across automotive, aerospace, and general industrial segments. For context, the 5.7% CAGR outpaces the broader metal cutting machinery market (estimated at 4.2% CAGR), indicating a structural shift from semi-automatic to fully automated band sawing solutions. For CEOs and production directors, this trend signals that capital expenditure allocated to legacy sawing equipment risks obsolescence as customers increasingly demand ISO 9001-certified traceability and digital process documentation.

Product Definition and Core Technology:

An automatic vertical metal band saw is a precision cutting machine configured with a vertically oriented blade carriage, designed for contour cutting, die block preparation, and high-volume sectioning of ferrous and non-ferrous metals. Unlike horizontal band saws optimized for straight cuts on long stock, vertical configurations excel at intricate shapes, nested part cutting, and tool steel blanking. Key components include: (1) a variable-speed band blade (typically 2,500–5,000 fpm), (2) servo-hydraulic feed system maintaining constant chip load, (3) automatic worktable with programmable cut paths, and (4) integrated coolant filtration for thermal stability. For engineering managers, critical specifications include maximum cutting thickness (typically 200–500mm for standard models), throat depth (300–1,000mm), and blade deviation tolerance—with premium systems achieving ≤0.1mm over 500mm of cut length.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)

https://www.qyresearch.com/reports/5761485/automatic-vertical-metal-band-saw

Key Industry Characteristics and Strategic Drivers:

1. Industry 4.0 Integration as a Competitive Imperative

The trend toward automation and the integration of Industry 4.0 principles is likely to continue. This may include features such as IoT (Internet of Things) connectivity, data analytics, and remote monitoring to enhance efficiency, maintenance, and overall performance. In Q3 2025, KASTO Maschinenbau GmbH launched its “smart saw 4.0″ platform, featuring real-time blade wear prediction using vibration spectrum analysis—enabling predictive maintenance alerts 50–100 operating hours before blade failure. According to AMADA GROUP’s 2025 annual report (released November 2025), its IoT-connected vertical band saws achieved mean time between failures (MTBF) of 4,200 hours, a 28% improvement over non-connected predecessors. For plant managers, these capabilities translate to reduced unplanned downtime (estimated savings of $15,000–$25,000 per line annually) and optimized blade change intervals, extending consumable life by 15–20%.

2. Discrete Manufacturing vs. Process Industry Divergence

A critical industry distinction exists between discrete manufacturing (automotive parts, aerospace components, general fabrication) and process industries (steel service centers, foundries). In discrete manufacturing, automatic vertical metal band saw demand is driven by batch size variation and material diversity—cutting everything from aluminum extrusions to Inconel superalloys. Here, programmability and quick changeover (under 10 minutes between material types) are paramount. Conversely, process industries prioritize continuous operation and maximum feed rates on standardized materials (e.g., carbon steel bars). A typical user case from a German automotive Tier 1 supplier (disclosed in a November 2025 industry case study) reported that deploying fully automatic vertical band saws with recipe storage for 200+ material types reduced setup time from 25 minutes to 6 minutes per job, increasing overall equipment effectiveness (OEE) from 68% to 83%.

3. Semi-Automatic vs. Fully Automatic – Market Segmentation Dynamics

The Automatic Vertical Metal Band Saw market is segmented as below:

By Type:

- Semi-Automatic (approximately 40% of 2025 revenue): Require operator intervention for material clamping, cut initiation, or blade speed adjustment. Lower capital cost ($25,000–$50,000) but higher labor dependency. Preferred by job shops and maintenance departments with low production volumes.

- Fully Automatic (approximately 60% and growing): Integrate CNC control, automatic material indexing, and robotic part unloading. Price range: $70,000–$180,000. According to QYResearch data, the fully automatic segment is projected to grow at 6.9% CAGR through 2032, outpacing semi-automatic (3.8% CAGR), as labor cost pressures intensify globally.

By Application:

- Industrial (general fabrication, ~55% of demand): Includes machinery building, oil and gas equipment, and heavy engineering. Priority specifications: ruggedness, blade life on abrasive materials (e.g., high-silicon aluminum), and coolant system capacity.

- Automobile Industry (~30%): The most technically demanding segment, requiring ±0.1mm cut accuracy for transmission components, axle blanks, and chassis brackets. A recent procurement tender from a Japanese automaker (Q4 2025) specified fully automatic vertical band saws with integrated statistical process control (SPC) logging, rejecting proposals lacking digital data export capabilities.

- Others (~15%): Aerospace (nickel alloy cutting), medical device manufacturing (stainless tube cutting), and tool/die shops.

Recent Industry Data and Policy Updates (Last 6 Months):

- September 2025: The European Commission’s Machinery Regulation (EU) 2023/1230 enforcement guidance clarified cybersecurity requirements for IoT-connected industrial equipment, including band saws. Suppliers without encrypted data transmission and role-based access control face compliance risks for EU installations.

- October 2025: The U.S. Department of Energy released updated motor efficiency standards (2027 effective date), effectively mandating IE4 premium efficiency motors on new automatic band saws. Manufacturers including DOALL and Cosen have preemptively redesigned drive systems, achieving 8–12% energy savings per machine.

- December 2025: China’s Ministry of Industry and Information Technology (MIIT) published “Guidelines for Intelligent Manufacturing in Metal Processing Equipment,” explicitly recommending automatic band saws with remote diagnostics for state-subsidized factory upgrades.

Technical Challenge – Blade Life Prediction in Variable Conditions:

Despite automation advances, blade life prediction remains a technical bottleneck. Factors including material hardness variation (e.g., annealed vs. hardened tool steel), coolant concentration drift, and chip packing dramatically affect blade wear rates. Leading suppliers are addressing this through multi-sensor fusion. BEHRINGER’s October 2025 technical disclosure described a system combining acoustic emission sensors, spindle current monitoring, and thermal imaging to predict remaining blade life within ±15% accuracy—enabling just-in-time blade replacement rather than conservative fixed-interval changes. Early adopters report blade cost reductions of 18–22% annually.

Exclusive Observation – The Emergence of Cloud-Based Cut Optimization:

Based on our analysis of patent filings and software releases over the past 12 months, a notable trend is the migration of cut parameter optimization to cloud platforms. Rather than relying on onboard machine controllers, new systems from MEP GROUP and KASTO upload cut history (material type, blade specification, achieved feed rate) to cloud databases, where machine learning algorithms identify optimal parameter sets. When a similar job is scheduled, recommended parameters are downloaded automatically. This approach addresses a persistent industry pain point: loss of cutting expertise when experienced operators retire. For marketing managers, cloud optimization offers a compelling value proposition—”preserve your best cutter’s knowledge across all shifts”—and creates recurring software subscription revenue streams.

Competitive Landscape – Selected Key Players (Verified from QYResearch Database):

AMADA GROUP, MEP GROUP, KASTO Maschinenbau GmbH, DoALL, Cosen, BEHRINGER, Nsncnc, Zjdljc, Hnhjsawing, Julihuang, Chenlong, Zj-weiye, Pilous, Chyun Yow Machinery Industry Co., Everising Machine Co.

Strategic Takeaways for Executives and Investors:

For CEOs and operations directors, the key decision framework for automatic vertical metal band saw investment includes: (1) matching automation level to batch size—fully automatic systems achieve ROI within 18–24 months for three-shift operations, (2) prioritizing IoT connectivity for predictive maintenance and OEE visibility, and (3) evaluating supplier software ecosystems for compatibility with existing MES/ERP platforms. For marketing managers, differentiation lies in demonstrating cybersecurity compliance (for EU markets), energy efficiency (for DOE-compliant U.S. installations), and cloud-based knowledge retention. For investors, the 5.7% CAGR, combined with recurring software and consumable (blade, coolant) revenue streams, positions leading suppliers as attractive mid-cap industrial technology investments, with potential upside from aftermarket service margins (typically 40–50% vs. 20–25% for new equipment).

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp