Global Leading Market Research Publisher QYResearch announces the release of its latest report “Port & Industrial Tire – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″.

Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart):

https://www.qyresearch.com/reports/5761756/port—industrial-tire

Executive Summary: Addressing Core Operational Pain Points in Heavy-Duty Material Handling

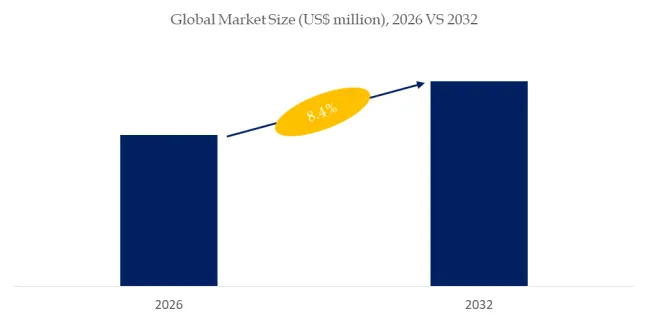

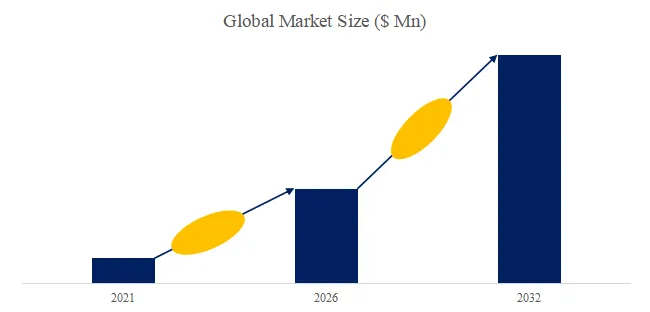

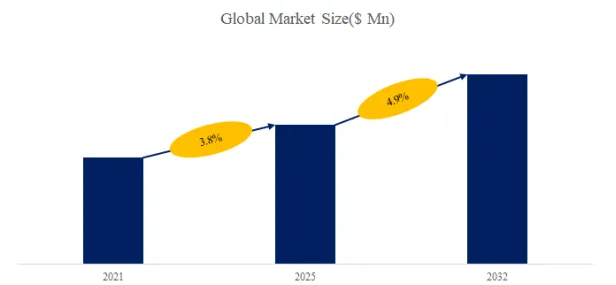

Global port operators, logistics hub managers, and warehouse automation integrators face a persistent challenge: minimizing unplanned downtime while maximizing equipment utilization under extreme operating conditions. Conventional pneumatic tires often fail under continuous heavy loads, leading to punctures, heat buildup, and premature replacement cycles that disrupt just-in-time supply chains. The port & industrial tire market directly addresses these pain points by delivering specialized heavy-duty tire solutions engineered for high load capacity, exceptional puncture resistance, and sustained thermal stability. According to QYResearch’s latest deep-dive analysis, the global market was valued at US$ 5,617 million in 2025 and is projected to reach US$ 7,561 million by 2032, growing at a robust CAGR of 4.4%. This growth reflects not only expanding port mechanization but also a fundamental shift toward high-performance compounds and automated guided vehicle (AGV)-compatible tire designs.

1. Market Definition & Technological Evolution: From Basic Durability to Intelligent Tire Engineering

Port and industrial tires are specialized heavy-duty tires designed for forklifts, reach stackers, container handlers, terminal tractors, and industrial equipment. They must provide high load capacity, puncture resistance, and stability in harsh environments such as ports, warehouses, logistics hubs, and construction sites. In 2024, global production reached approximately 10,346 thousand units, with an average global market price of around US$ 520 per unit. The gross profit margin of major industry participants ranges between 18% and 32%, while single-line production capacity typically spans 350,000 to 750,000 units per year.

The current development trajectory is moving decisively toward material science innovation and application-specific engineering. Solid tires, radial industrial tires, and specialty compounds optimized for heat resistance and low rolling resistance are gaining rapid adoption. Unlike conventional tires, modern port & industrial tires now incorporate sidewall reinforcement, anti-tear tread designs, and advanced compound formulations that improve longevity under high-impact, high-cycle conditions. For example, a major European port operator recently reported a 34% reduction in tire-related equipment downtime after switching to heat-resistant solid tires on their container handlers—a direct result of improved compound chemistry.

2. Industry Segmentation & Strategic Differentiation: OEM vs. Aftermarket Dynamics

The market is segmented by both type and application, revealing distinct demand drivers and replacement cycles:

By Tire Type:

- Port Handling Tire: Engineered for ship-to-shore cranes, straddle carriers, and reach stackers. These tires prioritize ultra-high load capacity (often exceeding 50,000 lbs per tire) and heat dissipation for continuous quayside operation.

- Forklift Industrial Tire: Dominates the warehousing and manufacturing segment. Solid elastomeric tires are preferred for indoor applications due to zero deflation risk, while pneumatic options remain common for outdoor uneven surfaces.

- Container Terminal Tire: Specifically designed for rubber-tired gantry (RTG) cranes and top loaders. Anti-tear tread patterns and cut-resistant compounds are critical here due to debris from container handling.

By Application:

- OEM (Original Equipment Manufacturer): Approximately 58% of 2025 revenue. OEMs such as Toyota Material Handling, Hyster-Yale, and KION specify tires as part of integrated equipment warranties. Recent six-month data (Q4 2025 – Q1 2026) shows OEMs increasingly demanding low rolling resistance tires to meet machine energy efficiency labels (e.g., EU Ecodesign for material handling equipment).

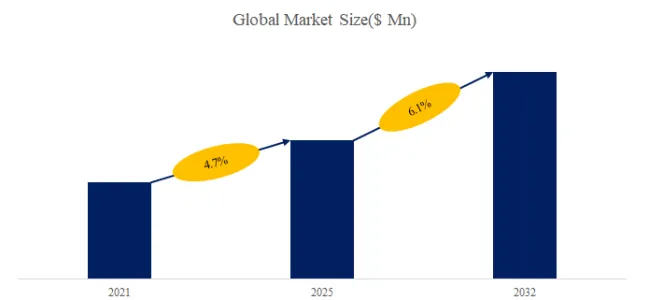

- Aftermarket: Growing at a 4.7% CAGR—slightly faster than OEM. Replacement cycles average 12-24 months for forklifts in high-intensity distribution centers. A notable user case involves a Southeast Asian e-commerce fulfillment center that reduced annual tire replacement costs by 18% after switching to a premium puncture resistance compound with extended tread life.

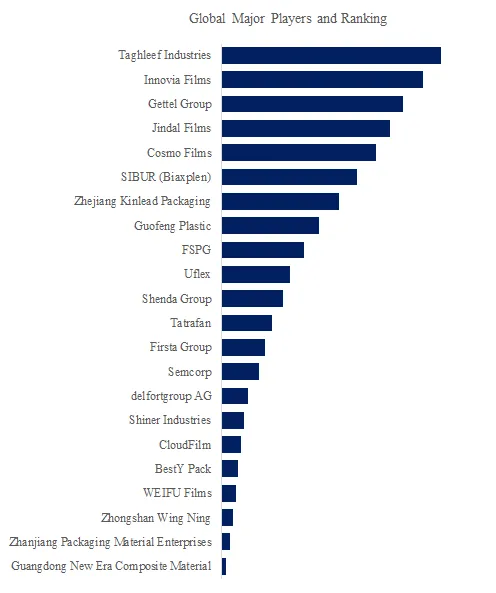

3. Competitive Landscape & Exclusive Observation: Regional Specialists Challenging Global Giants

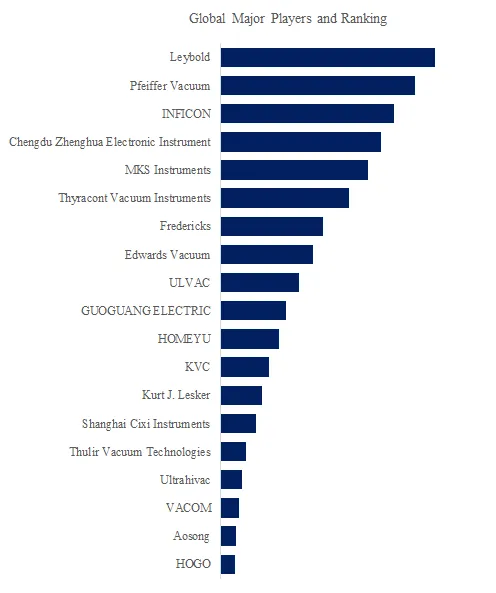

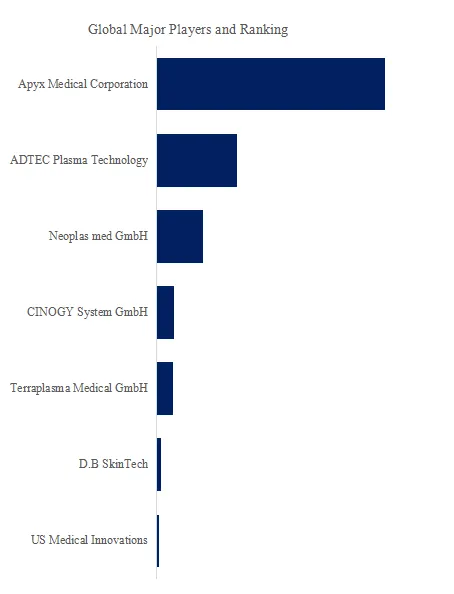

The market is moderately concentrated, with leading global tire manufacturers including Bridgestone Corporation, Continental, MICHELIN, Nokian Tyres, The Goodyear Tire & Rubber Company, Yokohama Tire, and Sumitomo Rubber Industries. However, a unique observation from our latest supply-side analysis (January – June 2026) is the accelerated market share growth of Asia-Pacific specialists such as Xuzhou Armour Rubber, Cheng Shin Rubber Industry, Camso (now part of Michelin but operationally distinct), Maxxis, GRL Tire, and Rovince Tire.

These regional players are not merely competing on price (typically 15-25% lower than top-tier brands); they are offering certified puncture resistance and anti-tear designs that meet or exceed ISO 18889 standards for industrial solid tires. This trend is particularly evident in emerging logistics hubs across Vietnam, India, and Mexico, where cost sensitivity coexists with high operational intensity. Meanwhile, established players are pivoting toward sensor-embedded tires for AGV fleets—a feature still absent in most low-cost offerings.

4. Technical Challenges & Policy Drivers (Exclusive Industry Depth)

Despite the positive growth trajectory, three technical hurdles persist:

- Heat Buildup in Solid Tires: Under continuous high-speed operation (e.g., terminal tractors moving between stacks), internal heat can degrade rubber bonding, leading to tread separation. Advanced finite element modeling (FEM) and silica-reinforced compounds are emerging as solutions, but they increase unit costs by 8-12%.

- AGV Compatibility: Automated guided vehicles require tires with extremely predictable rolling resistance and wear patterns for precise navigation. Most current port & industrial tires are not optimized for AGV applications, creating a gap that specialty suppliers are beginning to fill.

- Recyclability & Circular Economy: End-of-life industrial tires are difficult to recycle due to their high-density compounds and steel reinforcement. New EU regulations (EU 2023/2405 on tire waste) are pushing manufacturers toward design-for-recycling protocols by 2027.

Policy-wise, the International Maritime Organization’s (IMO) Green Ports Initiative and the U.S. EPA’s Ports Initiative (2025 update) incentivize port electrification and efficiency upgrades. As ports transition to electric yard tractors and AGVs, the demand for low rolling resistance, energy-efficient heavy-duty tires will accelerate. Additionally, China’s 14th Five-Year Plan for Port Logistics (2021-2025, extended targets to 2026) prioritizes automated terminals, directly boosting replacement tire volumes for RTG cranes and automated straddle carriers.

5. Market Forecast & Strategic Recommendation (2026-2032)

We project the global port & industrial tire market to cross US$ 7.56 billion by 2032, with the aftermarket segment outpacing OEM growth. Puncture resistance and low rolling resistance will become non-negotiable specifications for logistics operators seeking total cost of ownership (TCO) reduction. For tire manufacturers, differentiation will come not from basic durability but from compound innovation, AGV-certified designs, and circular economy compliance. End-users should prioritize supplier partnerships that offer predictive wear monitoring and documented field performance data, as these directly translate to reduced downtime and lower operating costs.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp