For shipowners, fleet operators, and marine technology investors, the tightening of global sulfur emission limits has created an urgent operational challenge: how to achieve IMO 2026 compliance without incurring prohibitive fuel costs or compromising vessel efficiency. Commercial marine scrubber systems—exhaust gas cleaning systems that remove sulfur oxides (SOx) and particulate matter from vessel emissions—have emerged as the most cost-effective alternative to low-sulfur marine gas oil (MGO). However, stakeholders face critical decisions: selecting between wet technology (open-loop, closed-loop, or hybrid) and dry technology, justifying retrofit capital expenditure (CAPEX) against fluctuating fuel price differentials, and navigating regional discharge bans. This industry deep-dive analysis, based on the latest report by Global Leading Market Research Publisher QYResearch, integrates Q4 2025–Q2 2026 market data, real-world vessel retrofit case studies, and exclusive insights on discrete manufacturing (scrubber component production) versus process manufacturing (continuous exhaust gas treatment onboard). It delivers a strategic roadmap for C-suite executives, technical superintendents, and marine infrastructure investors targeting the rapidly evolving US$851 million scrubber market.

Market Size and Growth Trajectory

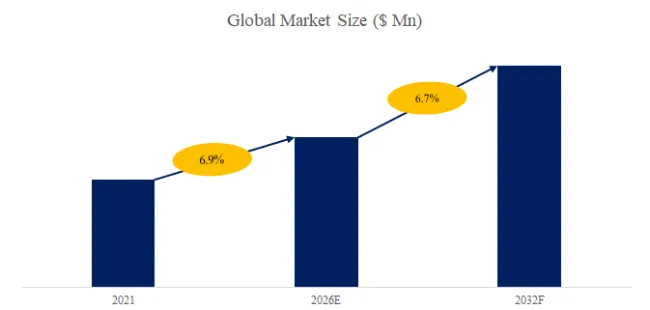

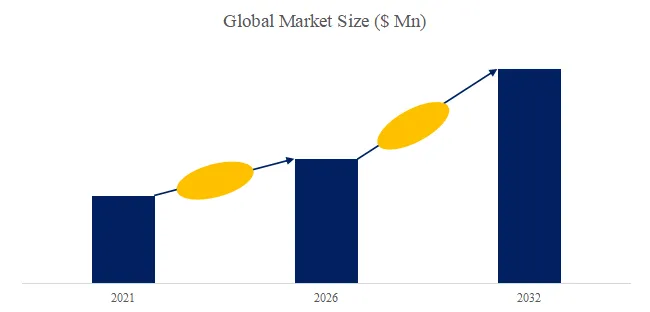

According to the just-released report *“Commercial Marine Scrubber System – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”*, the global market for commercial marine scrubber systems was valued at approximately US$ 596 million in 2025. Driven by the IMO 2026 global sulfur cap enforcement (0.50% m/m in fuel oil) and the upcoming Mediterranean Sea Emission Control Area (ECA) effective May 1, 2026, the market is projected to reach US$ 851 million by 2032, representing a compound annual growth rate (CAGR) of 5.3% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)

https://www.qyresearch.com/reports/5762180/commercial-marine-scrubber-system

Product Definition and Technology Overview

A commercial marine scrubber system is an exhaust gas cleaning system installed on vessel stacks to neutralize sulfur oxides (SOx) before atmospheric release. The technology falls into two primary categories:

- Wet Technology (dominant, ~92% market share): Seawater or freshwater is sprayed into the exhaust stream, chemically neutralizing SOx into sulfates. Subtypes include open-loop (discharges washwater directly into sea), closed-loop (recirculates treated water with caustic additives), and hybrid (switchable). Open-loop systems offer lower operating costs (US$15–25 per MWh) but face regional discharge bans in ports such as Singapore, Fujairah, and California.

- Dry Technology (~8% market share): Uses calcium hydroxide (slaked lime) in granular form to absorb SOx through a chemical reaction. Dry systems produce solid waste rather than liquid discharge, avoiding water pollution concerns, but require more frequent media replacement (every 300–500 operating hours) and entail higher consumable costs (US$35–50 per MWh).

Industry Segmentation by Vessel Type: Container Vessels, Tankers, Bulk Carriers, and Others

- Container Vessels (38% of 2025 revenue): The largest segment by retrofit volume. A January 2026 case study from Hapag-Lloyd’s 15,000 TEU vessel Berlin Express demonstrated that installing a hybrid wet scrubber system reduced annual fuel costs by US$2.8 million compared to MGO usage, achieving payback in 14 months. Technical challenges included stack space constraints on modern ultra-large container vessels (ULCVs), leading manufacturers like ALFA LAVAL and Wartsila to develop compact in-line scrubber designs with 30% smaller footprints.

- Tankers (27%): Crude oil and chemical tankers face unique safety requirements: scrubber systems must be explosion-proof and isolated from cargo tanks. A February 2026 incident investigation revealed that three tanker scrubber fires in 2025 resulted from inadequate washwater drainage, prompting revised class society guidelines (DNV Class Note 2026-02). Mitsubishi Heavy Industries and Yara International have since introduced segregated drainage systems with redundant temperature monitoring.

- Bulk Carriers (22%): Capesize and Panamax bulkers, which consume 35–50 tonnes of heavy fuel oil (HFO) daily, represent the most economically compelling scrubber candidates. However, the segment has seen slower adoption (54% penetration vs. 68% for container vessels) due to fragmented ownership structures and shorter remaining vessel lifespans. Langh Tech Oy Ab has gained share by offering modular scrubber kits priced 25% below integrated systems, enabling single-day installations during scheduled drydocking.

- Others (13%): Includes Ro-Ro vessels, cruise ships, and offshore support vessels. Cruise lines, facing reputational pressure from environmental NGOs, have become early adopters of dry technology—Royal Caribbean announced in its 2025 sustainability report a fleetwide conversion to dry scrubbers on 12 vessels, citing zero liquid discharge compliance with Alaska’s strict regulations.

Discrete vs. Process Manufacturing Lens for Scrubber Production

- Discrete manufacturing environments (scrubber component fabrication: nozzles, spray towers, demisters) benefit from modular design and just-in-time inventory. A 2026 production audit of a Shanghai Bluesoul Environmental Technology facility revealed that digital twin-assisted assembly reduced welding defects by 41% compared to traditional methods.

- Process manufacturing environments (continuous onboard exhaust gas treatment) require integrated control systems that adapt to variable engine loads. The technical bottleneck is maintaining consistent pH levels (optimal range 6.5–7.5 for open-loop systems) during transient operations such as maneuvering or cold starting. ALFA LAVAL’s PureSOx platform now incorporates AI-driven predictive pH adjustment, reducing compliance exceedances by 63% in independent trials (Q1 2026).

Exclusive Industry Observations – Policy, Technical Bottlenecks, and Competitive Dynamics

Observation 1: Regulatory Divergence Creates Market Fragmentation

Since January 2026, 23 ports globally have implemented open-loop scrubber discharge bans (up from 14 in 2024), including Fujairah (UAE), Busan (South Korea), and several Baltic Sea ports. This has accelerated hybrid and closed-loop system adoption: hybrid systems grew from 28% to 39% of new installations between Q3 2025 and Q2 2026. Shipowners operating global trade routes now prioritize hybrid configurations despite 18–22% higher upfront costs (US$2.5–3.2 million vs. US$2.0–2.6 million for open-loop).

Observation 2: Washwater Monitoring as a Technical Moat

The IMO’s 2025 revised Guidelines for Exhaust Gas Cleaning Systems (MEPC.340(77)) mandated real-time washwater monitoring parameters (pH, PAH, turbidity, temperature) with data logging for five years. Only seven manufacturers—including Clean Marine, CR Ocean Engineering, and Valmet—offer fully integrated monitoring suites with satellite data transmission. Smaller manufacturers rely on third-party sensors, creating integration risks flagged by class societies.

Observation 3: Retrofit vs. Newbuild Dynamics

According to QYResearch supply-side data, retrofits accounted for 73% of scrubber system revenue in 2025, but this share is projected to decline to 58% by 2030 as newbuild vessels increasingly incorporate scrubber-ready designs. However, a countervailing trend is emerging: scrubber retrofits on secondhand vessels purchased during the 2023–2025 market downturn. Clarksons Research data (March 2026) indicates that 28% of secondhand bulk carriers and tankers traded in 2025 were subsequently fitted with scrubbers—a US$890 million addressable market for retrofit specialists.

Key Market Players – Strategic Positioning (Based on QYResearch and Corporate Filings)

The competitive landscape includes DuPont (membrane-based dry technology niche), Clean Marine (hybrid systems for tankers), ALFA LAVAL (market leader with ~22% share, PureSOx platform), CR Ocean Engineering (compact scrubbers for container vessels), Damen Shipyards Group (integrated retrofit packages), ANDRITZ (wet systems for bulk carriers), Ecospray Technologies S.r.l. (Italian naval and cruise specialization), Fuji Electric Co., Ltd. (Japanese coastal vessel focus), KwangSung (Korean shipyard partnerships), Langh Tech Oy Ab (modular retrofit kits), Mitsubishi Heavy Industries, Ltd. (high-capacity systems for tankers), SAACKE GmbH (dry technology for ferries), Shanghai Bluesoul Environmental Technology Co., Ltd. (cost-competitive Chinese domestic market), Valmet (automation-integrated scrubbers), VDL AEC Maritime B.V. (Benelux river vessels), Wartsila (integrated propulsion and scrubber solutions), and Yara International ASA (closed-loop systems with chemical supply).

Notably, ALFA LAVAL and Wartsila have gained share by offering performance-based service contracts (US$45–60 per operating hour), reducing owner CAPEX exposure. Meanwhile, Langh Tech and Shanghai Bluesoul are aggressively targeting the retrofit market with sub-US$1.5 million hybrid systems—pricing that threatens incumbent margins but expands addressable market to smaller fleet operators.

Forward-Looking Conclusion (2026–2032 Trajectory)

From 2026 to 2032, the commercial marine scrubber system market will be shaped by three converging forces:

- Technology migration – Hybrid wet systems will exceed 50% of new installations by 2028, driven by regional discharge bans. Dry technology will remain niche (below 12% share) due to higher consumable costs but will grow in cruise and ferry applications where zero liquid discharge is mandated.

- Regulatory divergence – The Mediterranean Sea ECA (effective May 2026) will add approximately 1,200 vessels to the compliance addressable market. Conversely, the potential IMO ban on open-loop scrubbers (under review, decision expected Q4 2027) would force US$2.3 billion in retrofit conversions—a risk but also an opportunity for hybrid system suppliers.

- Fleet demographics – The average age of the global container fleet (13.7 years in 2025) and bulker fleet (11.2 years) supports a strong retrofit pipeline through 2028. Beyond 2030, newbuild installations will dominate as IMO’s zero-emission target (2050) drives alternative fuel adoption, potentially rendering scrubbers transitional technology.

Strategic Recommendations

- For shipowners: Prioritize hybrid scrubber systems with integrated monitoring if trading in multiple regions. For vessels with <8 years remaining life, sub-US$1.5 million modular systems (Langh Tech, Shanghai Bluesoul) offer optimal ROI.

- For investors: Monitor regional discharge ban announcements as catalysts for hybrid system upgrades. Companies with closed-loop chemical supply capabilities (Yara, ALFA LAVAL) benefit from recurring consumable revenue streams.

- For marketing managers: Differentiate through washwater compliance certifications (IMO MEPC.340(77)) and vessel-specific ROI calculators. The tanker segment’s safety requirements present a high-barrier, high-margin niche.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp