For road and highway contractors, demolition specialists, mining operators, and construction materials producers, the ability to process raw materials and recycled aggregates directly at the job site represents a critical competitive advantage. Traditional fixed crushing and screening installations require significant civil works, lengthy permitting processes, and substantial capital investment. When projects move or material sources change, fixed plants become stranded assets. The solution is the Construction Crushing and Screening Machine—a class of mobile and semi-mobile crushing equipment designed for frequent relocation. A complete mobile crushing and screening line typically consists of raw material bins, vibrating feeders, coarse crushing equipment, multi-layer vibrating screens, secondary crushing equipment, fine crushing equipment, mobile belt conveyors, sand washing machines, and electrical control systems—all placed on one or several tractor-trailer configurations. These systems are primarily deployed in industries requiring frequent movement and relocation, including highway construction, railways, metallurgy, chemical processing, and building materials production. This report delivers a comprehensive analysis of this dynamic construction machinery segment, incorporating recent infrastructure spending data, mobility segmentation, and regional competitive dynamics.

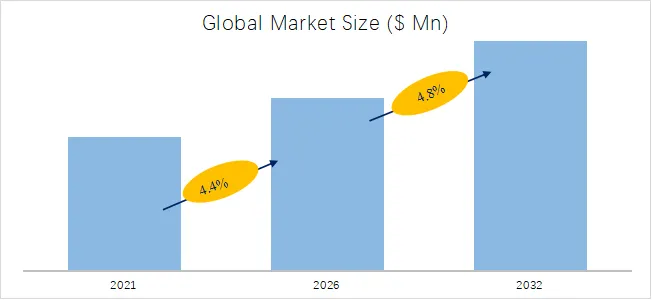

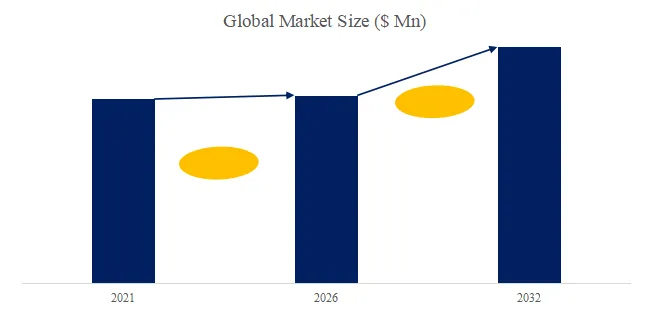

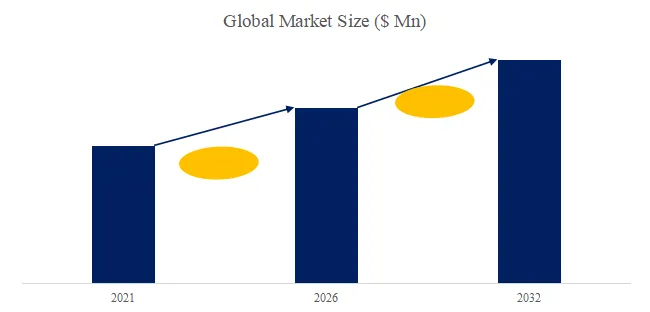

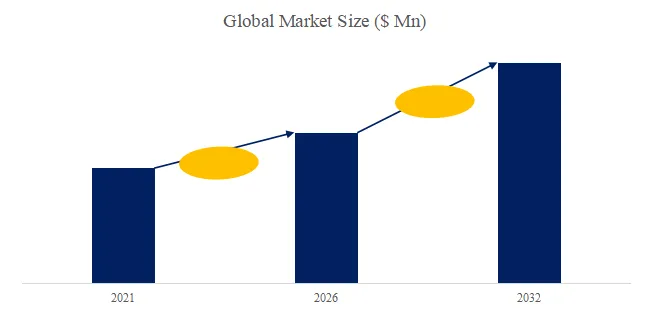

According to the latest release from global leading market research publisher QYResearch, *”Construction Crushing and Screening Machine – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032,”* the global market for Construction Crushing and Screening Machine was valued at US$ 2,718 million in 2025 and is projected to reach US$ 4,198 million by 2032, representing a compound annual growth rate (CAGR) of 6.5% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)

https://www.qyresearch.com/reports/5762498/construction-crushing-and-screening-machine

Product Definition – Technical Architecture and Configurations

A construction crushing and screening machine is an integrated material processing system designed to reduce large rocks, concrete rubble, asphalt millings, and other construction materials into specified aggregate sizes while separating materials by particle dimension. The complete mobile crushing and screening line comprises several core components:

- Raw material bins – Receiving hoppers with optional vibrating feeders for controlled material flow

- Coarse crushing equipment – Typically jaw crushers for primary reduction of feed material up to 1,000 mm

- Multi-layer vibrating screens – For size classification, typically with 2–4 deck configurations

- Secondary crushing equipment – Cone crushers or impact crushers for further size reduction

- Fine crushing equipment – For producing manufactured sand or fine aggregates (0–5 mm)

- Mobile belt conveyors – For material transfer between processing stages

- Sand washing machines – For removing fines and achieving specified cleanliness

- Electrical control systems – Centralized controls for coordinated operation

These components are mounted on one or several tractor-trailer chassis, enabling rapid deployment, on-site mobility, and efficient relocation between projects. The primary applications span highway construction, railway ballast production, metallurgical flux preparation, chemical industry raw material processing, and building materials manufacturing.

Market Context – Global Construction Machinery Landscape

To understand the Construction Crushing and Screening Machine market, it is essential to position it within the broader construction machinery industry. According to research data from the company’s “Construction Machinery Research Center,” total sales of the top 50 global construction machinery manufacturers reached US$ 230 billion in 2022 (industry standard reference). Regional dynamics reveal important patterns:

- Asian companies hold an absolute advantage, accounting for 50% of sales revenue among the top 50 manufacturers.

- Europe follows with 26% of sales revenue.

- North America accounts for 23% of sales revenue.

The world’s top 50 construction machinery OEMs sold approximately 1.2 million units of construction machinery and equipment in 2021, representing a 9% year-over-year sales increase.

China’s dominant position: China is currently the world’s largest construction machinery market. In 2022, Chinese construction machinery companies accounted for 24% of total global sales among the top 50 manufacturers, making it the country with the highest proportional representation.

However, according to data from the China Machinery Industry Federation, the operating income of China’s construction machinery industry declined by more than 12% in 2022, totaling 797.7 billion RMB (approximately US$ 110 billion at 2022 exchange rates). Despite this domestic slowdown, China’s annual export volume reached US$ 44.3 billion, with a net increase in export volume over two years amounting to US$ 13.3 billion. This export growth indicates that Chinese crushing and screening equipment manufacturers are increasingly competitive in international markets, particularly in Southeast Asia, Africa, and South America where infrastructure development is accelerating.

Exclusive Analyst Observation – Recycling as a Growth Accelerator: The 6.5% CAGR for crushing and screening equipment is notably higher than the broader construction machinery market (approximately 4–5% during the same period). This differential is driven by the rapid expansion of construction and demolition (C&D) recycling. According to the Global Construction and Demolition Waste Management Report (January 2026), C&D waste generation reached 3.3 billion tons annually in 2025, with recycling rates in advanced economies targeting 70–90% by 2030. Mobile crushing and screening plants are the primary technology for on-site C&D waste processing, creating a significant tailwind for this equipment category.

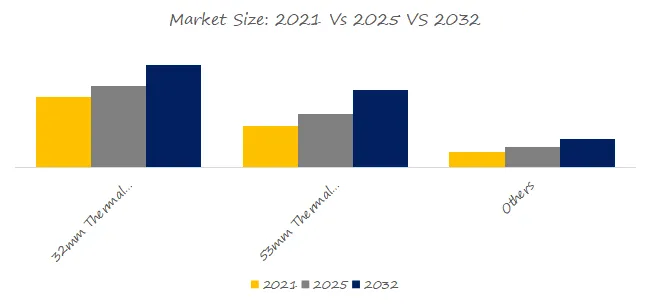

Segmentation Deep Dive – Mobility Classifications

The market segments crushing and screening equipment by mobility level, reflecting different operational requirements and capital investment profiles.

Fully Fixed Crushing and Screening Stations are permanent installations with foundations, civil structures, and material handling systems designed for decades of operation at a single site. These systems are used at major quarries, mines, and port facilities where material sources are stable and production volumes justify the capital expenditure (typically US$ 5–20 million). Fully fixed stations represent approximately 25–30% of the market by value, but the lowest growth rate (3–4% CAGR) as operators shift toward more flexible configurations.

Semi-Fixed Crushing and Screening Stations feature some components mounted on structural steel skids rather than concrete foundations, allowing relocation over periods of 1–5 years. These systems are common at medium-term construction projects and smaller quarries. They represent approximately 20–25% of the market.

Semi-Mobile Crushing and Screening Stations are designed for relocation every 6–24 months, with major components mounted on transport frames that can be moved by heavy haul trailers. These systems require some site preparation (leveled pads, minimal foundations) but offer significant flexibility compared to fixed stations. They represent approximately 20–25% of the market and are growing at 6–7% CAGR.

Fully Mobile Crushing and Screening Plants are self-contained units mounted on tracked or wheeled chassis that can move within a job site without disassembly. These systems can relocate daily or weekly as the working face advances. Fully mobile plants represent the fastest-growing segment (9–10% CAGR) and are projected to increase from approximately 15% of market value in 2025 to 22–25% by 2032. Key drivers include urban demolition projects (where space is constrained), road recycling operations (where the plant moves with the paving train), and natural disaster debris clearance.

Others includes modular systems and custom configurations that do not fit standard classifications.

Technical Pain Points and Recent Innovations

Dust Suppression in Mobile Configurations: Mobile crushing and screening plants operate close to populated areas on demolition and road projects, making dust control a critical regulatory and community relations issue. Recent innovations (commercialized 2024–2025) include:

- Enclosed conveyor systems with negative pressure dust extraction

- Water spray systems with automated activation based on material moisture sensors

- Dry fog dust suppression (ultrasonic atomization) that captures sub-10-micron particles

A user case from a major infrastructure project in London (Crossrail 2 enabling works, 2025) deployed fully mobile crushing plants with advanced dust suppression, achieving 95% dust capture and enabling on-site processing of 450,000 tons of excavated material, avoiding 30,000 truck trips through central London.

Wear Parts Management: Crushing equipment experiences significant wear from abrasive materials. Modern systems now incorporate:

- Wear part monitoring sensors that predict remaining life (commercialized by Metso Outotec in 2025)

- Quick-change cartridge systems reducing liner replacement time from 8 hours to 90 minutes

- High-chrome and ceramic composite wear materials extending life by 30–50%

Electrical Control Systems for Coordinated Operation: Mobile plants require sophisticated control systems to manage multiple conveyors, crushers, and screens operating in sequence. Recent advancements include:

- PLC-based centralized control with remote monitoring capabilities

- Automated feed rate control to prevent crusher overload

- Real-time production reporting and predictive maintenance alerts

Industry Layering – Discrete vs. Process Manufacturing in Crushing Equipment

The crushing and screening equipment industry exhibits characteristics of both discrete manufacturing (equipment fabrication and assembly) and process manufacturing (material flow optimization).

Discrete manufacturing focus: The production of individual crushers, screens, and conveyors involves discrete part fabrication—steel plate cutting, welding, machining of shafts and bearings, assembly of hydraulic systems. Key challenges include managing SKU proliferation (different crusher types, sizes, and configurations) and ensuring quality control across fabricated components.

Process manufacturing perspective: Once deployed, crushing and screening plants operate as continuous process systems—material flows from bin to crusher to screen to conveyor. Optimization requires understanding of material properties (hardness, abrasiveness, moisture content), flow rates, and size reduction curves. Leading equipment manufacturers now offer process simulation software that models entire crushing circuits, allowing operators to predict performance before purchasing equipment.

Exclusive Analyst Observation: The most successful manufacturers in this market are those that bridge discrete and process manufacturing competencies—producing robust, reliable machines (discrete excellence) while offering process optimization expertise that helps customers maximize throughput and minimize operating costs (process knowledge). This dual capability commands premium pricing and customer loyalty.

Application Segmentation – Beyond Traditional Construction

While Construction Industry applications (highway aggregates, railway ballast, concrete production) remain the largest segment (approximately 55–60% of demand), three additional applications are driving growth:

Garbage Collection (C&D Waste Processing): As landfill space diminishes and recycling mandates expand, crushing and screening equipment is increasingly deployed at transfer stations and recycling facilities. This segment is growing at 8–9% CAGR, significantly above market average. A specific case: The City of San Francisco’s C&D recycling ordinance (updated January 2026) requires 90% diversion from landfills, driving municipal investment in mobile crushing equipment for processing concrete, asphalt, and mixed debris.

Environmental Friendly (Natural Aggregate Conservation): Regulations restricting river sand extraction and mountain quarrying are driving adoption of manufactured sand production using crushing equipment. The European Union’s Critical Raw Materials Act (fully implemented January 2026) includes aggregates as a strategic resource, promoting on-site crushing of excavated rock for reuse.

Others includes metallurgical flux production, chemical industry raw material processing, and agricultural limestone application.

Recent Policy Drivers (2025–2026)

Several regulatory developments are shaping the crushing and screening equipment market:

- US Infrastructure Investment and Jobs Act (IIJA): US$ 1.2 trillion over 10 years, with significant funding for highway reconstruction and bridge replacement—both applications generating substantial recycled asphalt pavement (RAP) and concrete requiring mobile crushing.

- EU Circular Economy Action Plan 2.0 (effective March 2026): Mandates that 70% of C&D waste be recycled by 2030, up from 50% in 2020. This directly drives demand for mobile crushing and screening equipment.

- China’s 14th Five-Year Plan for Green Development (2026–2030): Includes targets for construction waste recycling rates of 60% in major cities by 2028, creating significant domestic demand for crushing equipment.

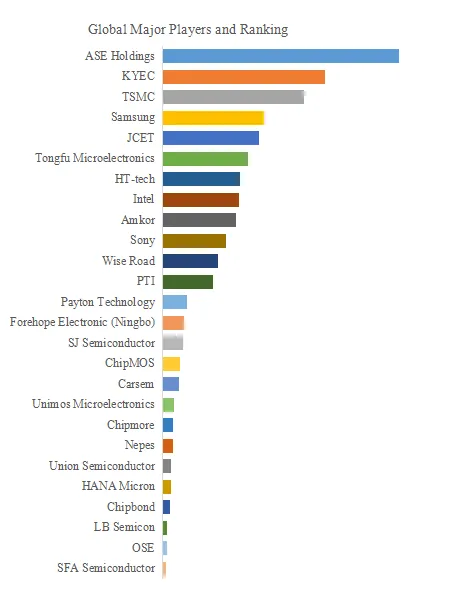

Competitive Landscape Summary

The market includes global crushing equipment specialists, diversified construction machinery manufacturers, and numerous regional Chinese players.

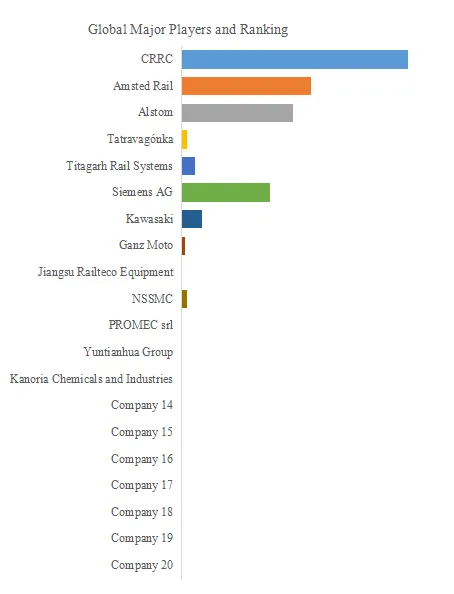

Global leaders: Metso Outotec Corporation (Finland/US) – comprehensive portfolio from fixed to fully mobile systems; EDGE Innovate (Ireland) – specializing in mobile screening and crushing; Ecoverse (US) – industrial shredding and screening; ARJES (Germany) – heavy-duty mobile shredders; Rotochopper (US) – grinding equipment; SSI SHREDDING SYSTEMS (US) – primary shredders; Van Dyk Recycling Solutions (US/Netherlands) – recycling system integrators; EC Papé (France) – crushing and screening equipment.

Chinese manufacturers with strong domestic and export presence: Luoyang Dahua Heavy Industry, SHIBANG INDUSTRY & TECHNOLOGY GROUP CO., LTD. (SBM), Hongxing Machinery, Shanmei, Shisheng Jixie, Hengyang Industry, Zhengzhou Danxing Jixie, Wuxi Haoding, Henan Lanji Machinery, Wenxian Zhenke Machinery, Hunan Rongchang Mechanical, HENAN LIMING HEAVY INDUSTRY.

Chinese manufacturers typically offer price advantages of 25–40% compared to Western brands but face challenges in aftermarket support and parts availability in distant markets. Several are addressing this through distributor networks in Southeast Asia, Africa, and South America.

Segment Summary (Based on QYResearch Data)

Segment by Type (Mobility Classification)

- Fully Fixed Crushing and Screening Station – Permanent installation; foundations required; lowest growth rate (3–4% CAGR).

- Semi-Fixed Crushing and Screening Station – Skid-mounted; relocation every 1–5 years.

- Semi-Mobile Crushing and Screening Station – Transport frame mounted; relocation every 6–24 months.

- Fully Mobile Crushing and Screening Plant – Tracked or wheeled; moves daily/weekly; fastest-growing segment (9–10% CAGR).

- Others – Modular and custom configurations.

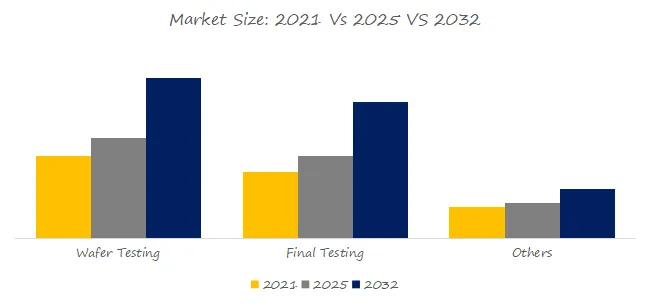

Segment by Application

- Construction Industry – Highway aggregates, railway ballast, concrete production (largest segment, 55–60%).

- Garbage Collection – Construction and demolition waste processing (fastest-growing, 8–9% CAGR).

- Environmental Friendly – Manufactured sand production, natural aggregate conservation.

- Others – Metallurgical flux, chemical processing, agricultural applications.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp