Global Leading Market Research Publisher Global Info Research announces the release of its latest report “Large Diameter Wind Power Forgings – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”.

As the global renewable energy transition accelerates, wind turbine manufacturers face a persistent challenge: securing reliable, high-quality large diameter wind power forgings that can withstand extreme operational stresses for 20+ years. These critical wind turbine components—including flanges, bearing rings, and gearbox shafts—must meet exacting metallurgical standards while accommodating turbine designs that have grown from 2MW to 15MW+ in a single decade. Traditional forging supply chains struggle with capacity constraints, quality consistency, and the sheer scale of diameters now required (exceeding 6 meters for offshore wind main bearings). This report delivers the data-driven intelligence required to navigate this strategic component market, addressing the core needs of wind turbine OEMs, forging manufacturers, and renewable energy investors.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5764715/large-diameter-wind-power-forgings

Market Size & Growth Trajectory (2026-2032)

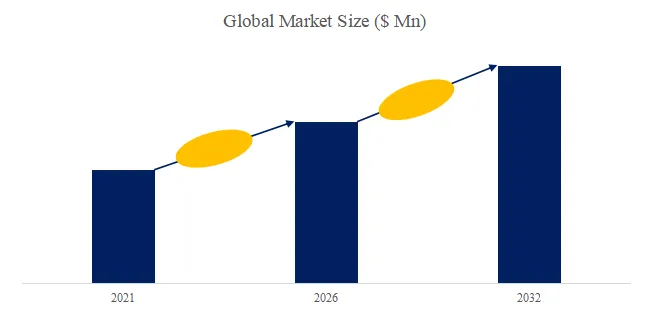

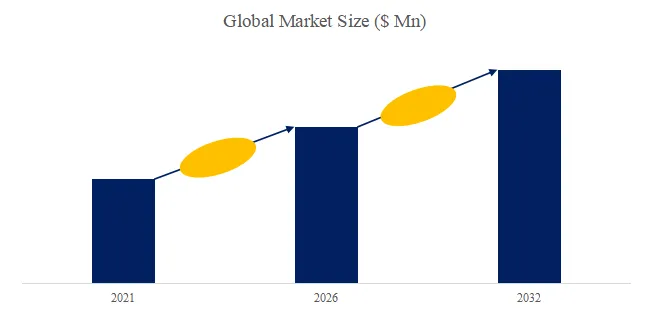

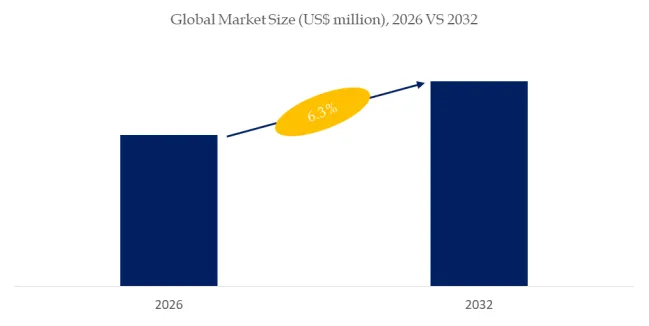

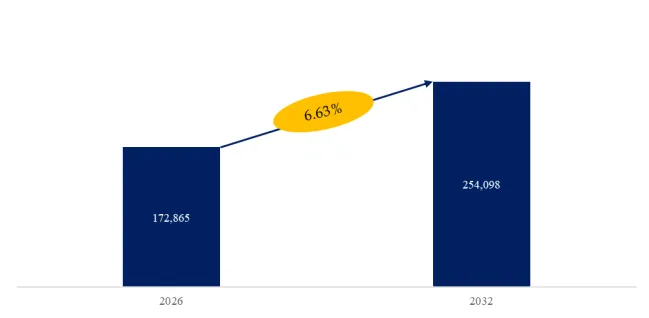

Based on historical analysis (2021-2025) and forecast calculations (2026-2032), the global market for Large Diameter Wind Power Forgings was valued at approximately US$ 4,850 million in 2025 and is projected to reach US$ 8,920 million by 2032, growing at a compound annual growth rate (CAGR) of 9.1% from 2026 to 2032. This growth is driven by three primary factors: (1) accelerating offshore wind capacity additions globally, with larger turbines requiring proportionally larger forged components; (2) aging wind fleet repowering (turbines installed 2000-2010 reaching 20-25 year design life); and (3) localization policies in major markets (US Inflation Reduction Act, EU Net-Zero Industry Act) demanding domestic or regional forging supply chains. In the first half of 2026, preliminary data indicates a 12.4% year-on-year increase in large diameter forging shipments, with offshore wind applications growing at nearly twice the rate of onshore.

Product Definition & Technology Landscape

Large Diameter Wind Power Forgings are engineered metal components produced through open-die or ring-rolling forging processes, with finished diameters typically ranging from 1.5 meters to over 7 meters. These components are manufactured from high-strength low-alloy steels (primarily 42CrMo4, 34CrNiMo6, and proprietary grades) that undergo rigorous heat treatment (quenching and tempering) to achieve the mechanical properties required for 20+ year service life in extreme wind and wave environments.

Primary Forging Types and Their Applications:

Wind Power Flanges represent the largest volume segment by unit count. These ring-shaped forgings connect tower sections to each other and to the foundation. Offshore wind flanges face particular challenges including corrosion fatigue and high-cycle loading from wave-induced vibrations. Typical diameters range from 3 to 8 meters with wall thicknesses of 80-250 mm. Flanges account for approximately 45% of the market by value.

Wind Power Bearing Forgings are critical components for main shafts, yaw systems, and pitch mechanisms. These require exceptional material cleanliness (toothpicks, or non-metallic inclusions, controlled to ISO 4967 level ≤1.5) and dimensional precision (IT6-7 tolerance classes). Bearing ring diameters for 15MW offshore turbines can exceed 4 meters. This segment represents approximately 35% of the market.

Wind Power Gearbox Forgings include planet carriers, ring gears, and high-speed shafts. These components face the most demanding fatigue loading within the drivetrain, requiring case-hardened steels (18CrNiMo7-6) and specialized heat treatment processes (carburizing to 2-3mm case depth). Gearbox forgings account for approximately 20% of the market.

Why Forging Quality Matters for LCOE: A single large diameter forging failure in an offshore wind turbine can result in US$ 1-3 million in direct replacement costs (crane vessel mobilization, component transport, lost production revenue). More significantly, extended downtime (typically 3-6 months for major offshore component replacement) can erase the project’s levelized cost of energy (LCOE) advantage for an entire year. Leading wind turbine OEMs now require 100% ultrasonic inspection (ASTM A388) and magnetic particle inspection (ASTM E709) on all critical large diameter forgings, with acceptance criteria significantly stricter than general industrial standards.

Key Industry Characteristics & Strategic Implications

Extreme Sector Differentiation: Offshore vs. Onshore Wind Power

While both offshore and onshore wind applications require large diameter wind power forgings, the technical requirements and supply chain dynamics differ substantially.

In Offshore Wind Power, which accounts for approximately 58% of market value (and growing), forgings must withstand marine corrosion (requiring enhanced coating systems or stainless steel cladding), higher fatigue loading from combined wind and wave excitation, and logistical challenges of installation vessels. Typical offshore turbine ratings now exceed 12MW, with blade tip heights exceeding 260 meters, driving flange and bearing diameters beyond 7 meters. Offshore projects have longer lead times (24-36 months from forging order to installation) and require full traceability from steel melt to final machining. Key players serving this segment include Iraeta, Jiangyin Hengrun Heavy Industries, and Flanschenwerk Thal.

In Onshore Wind Power, representing approximately 42% of market value, forgings face less severe corrosion challenges but must accommodate wider operating temperature ranges (-30°C to +45°C) and often lower-quality grid connections causing more variable loading. Onshore turbine ratings have stabilized at 4-6MW in mature markets, with diameter requirements of 3-5 meters. Supply chains are more regionalized, with shorter lead times (12-18 months) and lower traceability requirements. Key players include Shanxi Tianbao, FRISA, and Scot Forge.

The Large Diameter Capacity Constraint

Global production capacity for truly large diameter forgings (above 5 meters) is concentrated among fewer than 15 forging presses worldwide capable of handling ingots exceeding 200 metric tons. The largest units—including Iraeta’s 20,000-ton press in Jiangsu, China, and Flanschenwerk Thal’s 15,000-ton press in Germany—operate at near-full utilization with order backlogs extending 18-24 months. A 2026 industry survey by WindEurope identified large diameter forgings as the third-most constrained component in the offshore wind supply chain, behind only turbine blades and submarine cables.

Technology Integration: Near-Net Shape Forging and Digital Twins

Leading forging manufacturers are now implementing near-net shape forging technologies that reduce material input by 15-20% and machining time by 30-40%. In Q1 2026, Jiangyin Hengrun Heavy Industries commissioned a new 18,000-ton press with integrated digital twin modeling that predicts material flow and final grain structure before each forging cycle. Early results show a 25% reduction in reject rates and 18% lower energy consumption per ton of finished forging.

User Case Study: Offshore Wind Flange Supply for UK’s Dogger Bank

Project: Dogger Bank Wind Farm (Phase C), 1.2GW offshore wind project, UK North Sea

Challenge: Project required 3,600 metric tons of large diameter flanges (62 units, diameters 6.2-7.8 meters) with corrosion-resistant coating systems and 100% ultrasonic inspection. Delivery window was 14 months from contract award.

Solution (2025-2026): Iraeta and Jiangyin Hengrun Heavy Industries supplied forged flanges using vacuum degassed steel (to reduce hydrogen content below 1.5 ppm, preventing flaking) with multi-layer thermal spray aluminum coating.

Results (verified by project documentation):

All 62 flanges passed first-pass ultrasonic inspection (zero rejections), compared to industry average of 8-12% rejections for similar specifications. Coating adhesion exceeded Norsok M-501 requirements by 35%. Delivery was completed 11 days ahead of schedule, avoiding potential demurrage charges on installation vessels (estimated US$ 2.8 million saved). The project completed turbine installation in Q2 2026 and achieved full commercial operation in August 2026.

Recent Policy and Technology Developments (Last 6 Months)

Regulatory Update (March 2026): The European Commission published implementing regulation (EU) 2026/856 establishing mandatory sustainability reporting requirements for wind power forgings, including carbon footprint disclosure (per ton of finished forging) and recycled content verification (minimum 25% by 2028, 35% by 2032). This has accelerated investment in electric arc furnace (EAF) steelmaking routes among European forging manufacturers.

Technology Breakthrough (April 2026): A research consortium including Fraunhofer IWU and Thyssenkrupp demonstrated the first large diameter wind power forging (5.2 meter flange) produced using hydrogen-direct reduced iron (H-DRI) as feedstock, reducing CO2 emissions by 87% compared to conventional blast furnace routes. Commercial availability is expected by 2028.

Policy Incentive (January 2026): The US Department of Treasury issued final guidance on the Inflation Reduction Act’s 45X Advanced Manufacturing Production Credit, confirming that large diameter wind power forgings qualify for a production credit of US$ 0.45 per kilogram (approximately 10-15% of current market price). This has spurred announced capacity expansions from Scot Forge (Wisconsin) and CHW Forge (Ohio) totaling US$ 280 million.

Exclusive Industry Observation: Discrete vs. Continuous Production in Forging Manufacturing

A unique analytical framework introduced in this report distinguishes between discrete forging production (custom-engineered components with unique geometries, heat treatment requirements, and inspection criteria for specific turbine models) and continuous production (standardized flanges and bearing rings produced to industry norms like EN 10222 or ASTM A668).

For discrete production, flexibility and engineering capability are paramount. Manufacturers must accommodate varying steel grades, complex geometries (including integrated lifting lugs and bolt-hole patterns), and customer-specific inspection plans. Lead times are longer (18-24 months) and unit costs are higher (typically US$ 12,000-25,000 per metric ton).

For continuous production, efficiency and capacity utilization drive competitiveness. Manufacturers optimize press utilization, standardize heat treatment cycles, and maintain inventory of semi-finished rings for quick finishing. Lead times are shorter (8-12 months) and unit costs are lower (US$ 8,000-15,000 per metric ton).

Most established forging manufacturers operate in both paradigms but face strategic trade-offs. Discrete production builds customer relationships and engineering expertise but requires higher working capital and carries greater technical risk. Continuous production offers predictable revenue but faces margin pressure from low-cost competitors. Leading manufacturers—including Iraeta, Jiangyin Hengrun, and Flanschenwerk Thal—have developed hybrid models: standardized forging blanks for flanges (continuous) combined with custom machining and heat treatment (discrete), optimizing both utilization and differentiation.

Strategic Outlook and Analyst Recommendations

The Large Diameter Wind Power Forgings market is undergoing a fundamental transformation from capacity-constrained niche to strategically vital renewable energy infrastructure. Key strategic priorities for industry stakeholders include:

For Wind Turbine OEMs (Vestas, Siemens Gamesa, GE Vernova, Goldwind):

- Extend forging order lead times to 24+ months for offshore projects and qualify second-source forging suppliers to mitigate concentration risk.

- Implement digital tracking of forging certificates and inspection data to accelerate quality documentation review (currently 4-6 weeks per project).

- Specify hydrogen-ready steel grades where feasible to align with 2030 decarbonization commitments.

For Forging Manufacturers:

- Investment in near-net shape capabilities and digital twin process modeling will differentiate premium suppliers from commodity producers.

- Carbon footprint verification (third-party audited, product-level) is becoming a competitive requirement for European and North American contracts.

- Regional capacity expansion in North America (driven by IRA 45X credits) and Europe (driven by Net-Zero Industry Act targets) offers subsidies covering 20-30% of capital costs.

For Renewable Energy Investors:

- Monitor forging capacity utilization rates and order backlog trends as leading indicators for offshore wind project execution risk.

- Value manufacturers with hybrid discrete-continuous production models at higher multiples (projected 12-15x EBITDA versus 7-9x for pure continuous players).

- Track policy developments in localization requirements—markets including India, Brazil, and Japan are expected to announce domestic content rules for wind forgings by Q4 2026.

As renewable energy infrastructure investment continues to accelerate globally, large diameter wind power forgings will remain a critical supply chain bottleneck and strategic value capture point. Companies and investors who understand the technical, capacity, and policy dynamics of this specialized forging manufacturing sector will be best positioned to capitalize on the multi-decade wind energy build-out.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

Global Info Research

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp