Global Leading Market Research Publisher QYResearch announces the release of its latest report *“Zirconia Alumina Cut Off Wheel – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”*.

For fabrication shop managers, automotive production engineers, and aerospace procurement directors, the daily challenge is consistent: cutting hard metals—stainless steel, titanium, and alloy steels—quickly and precisely without frequent wheel changes, excessive material waste, or heat-related workpiece damage. Traditional abrasive wheels wear too fast, generate dangerous sparks, and require constant replacement, driving up both direct tooling costs and expensive production downtime. The zirconia alumina cut off wheel has emerged as the definitive solution, combining exceptional wear resistance with high cutting efficiency and superior heat dissipation. Based on rigorous historical analysis (2021–2025) and forward-looking forecast calculations (2026–2032), this report provides a comprehensive assessment of the global market, including market size, share, demand trajectories, industry development status, and strategic forecasts.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)

https://www.qyresearch.com/reports/6091866/zirconia-alumina-cut-off-wheel

Market Size & Growth Trajectory: A 7.4% CAGR Driven by Hard Metal Fabrication Demand

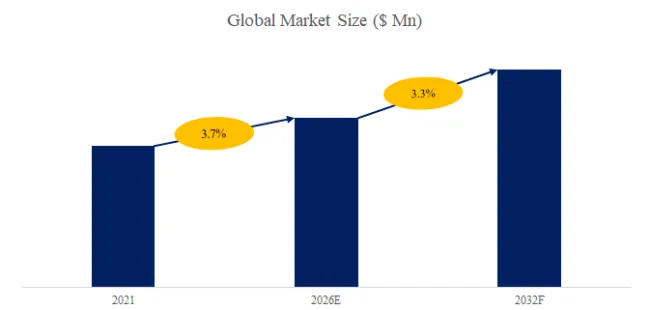

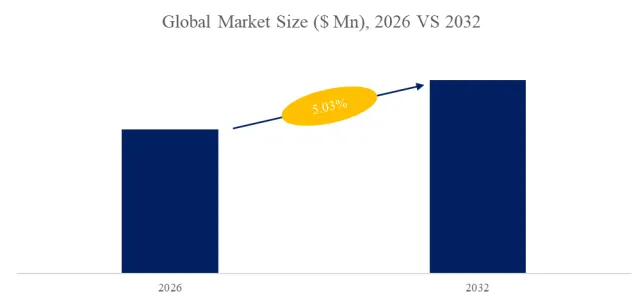

According to QYResearch’s latest market intelligence—sourced exclusively from verified corporate annual reports, industry association publications, and financial sector disclosures—the global zirconia alumina cut off wheel market was valued at approximately US$ 1.355 billion in 2025 and is projected to reach US$ 2.220 billion by 2032, expanding at a robust CAGR of 7.4% from 2026 to 2032. This growth trajectory reflects accelerating demand from automotive lightweighting (increasing use of high-strength steel and aluminum alloys), aerospace superalloy machining (Inconel, titanium grades), and general metal fabrication sectors prioritizing productivity gains.

For plant managers and procurement executives, the 7.4% CAGR signals a structural shift: cutting efficiency and tool longevity have overtaken upfront price as primary purchasing criteria, as total cost of ownership (TCO) models consistently demonstrate that zirconia alumina wheels deliver 30–50% lower cost per cut compared to conventional aluminum oxide or silicon carbide alternatives.

Product Definition & Technical Depth: Engineering Superior Wear Resistance

A zirconia alumina cut off wheel is a high-performance bonded abrasive tool manufactured from a proprietary composite of zirconium dioxide (ZrO₂) and aluminum oxide (Al₂O₃) abrasive grains, fused through a specialized sintering process that creates a dense, micro-fracturing grain structure. Unlike conventional abrasives that dull through macro-fracturing, zirconia alumina grains undergo controlled micro-fracturing during cutting, continuously exposing fresh, sharp cutting edges. This self-sharpening mechanism delivers three critical performance advantages:

1. Exceptional Wear Resistance: The ZrO₂-Al₂O₃ composite hardness (Mohs 9.0–9.2) significantly outperforms standard aluminum oxide (Mohs 9.0) in high-pressure, high-temperature cutting environments. Field data from automotive powertrain plants show zirconia alumina wheels lasting 3–5 times longer than conventional wheels when cutting hardened steel (HRC 45–60).

2. High Cutting Efficiency: The micro-fracturing grain behavior maintains a consistently high material removal rate (MRR) throughout the wheel’s lifecycle. In stainless steel cutting applications (304, 316 grades), zirconia alumina wheels achieve MRR values 25–35% higher than premium aluminum oxide wheels, directly reducing cycle times.

3. Superior Heat Dissipation: The dense grain structure and specialized bonding system (typically resin or vitrified) conduct heat away from the cutting zone more effectively. Lower cutting zone temperatures—typically 200–300°C compared to 400–500°C for conventional wheels—translate to reduced workpiece thermal distortion, minimized burr formation, and safer operating conditions.

Critical technical parameters that decision-makers must evaluate:

- Grain composition ratio: Typical ZrO₂ content ranges from 25% to 40%, with higher zirconia concentrations delivering greater toughness at the expense of friability. For titanium and Inconel cutting, 35–40% ZrO₂ grades are preferred; for general stainless steel fabrication, 25–30% offers optimal balance.

- Wheel hardness grade: Ranging from soft (for hard materials requiring grain shedding) to hard (for soft materials requiring grain retention). Automotive applications typically specify medium-hard grades (P–R scale).

- Maximum operating speed: Standard wheels are rated for 80–100 m/s, with high-performance variants reaching 120 m/s for robotic cut-off operations.

Primary application domains include metalworking (general fabrication, pipe cutting, structural steel), automotive manufacturing (exhaust systems, chassis components, drive shafts), aerospace (titanium alloy machining, superalloy trimming), and shipbuilding (plate cutting, weld preparation). The wheels are compatible with angle grinders (4.5–9 inch diameters), chop saws, and automated cut-off machines.

Key Industry Development Trends (2026–2032): Exclusive Analyst Observations

Drawing exclusively from QYResearch’s proprietary market database, official annual reports of listed manufacturers, and industry technical publications released in the past six months (September 2025–March 2026), the following four structural trends are reshaping the zirconia alumina cut off wheel landscape:

1. Dry-Type Wheels Dominate, But Wet-Type Gains Traction in Precision Applications

The market is segmented into dry-type and wet-type zirconia alumina cut off wheels. Dry-type wheels currently command approximately 82% of global revenue, driven by their convenience for angle grinder applications in construction and field repair. However, wet-type wheels—which require coolant or lubricant application during cutting—are growing at a faster CAGR of 9.2%, driven by:

- Aerospace and medical device manufacturing: Stringent surface finish requirements (Ra < 1.6 μm) and thermal damage prohibitions mandate wet cutting.

- High-speed automated cutting cells: Flood coolant extends wheel life by 40–60% and enables feed rates exceeding 50 mm/s in robotic applications.

For production engineers specifying automated workcells, the incremental cost of wet-type systems (coolant delivery, filtration, disposal) is increasingly justified by lower consumables expense and reduced rework rates.

2. Metal Processing Remains the Anchor Segment, but Automobile Maintenance Shows Accelerated Growth

Segment-by-application analysis reveals diverging growth profiles:

- Metal Processing (42% market share in 2025): Steady growth at 6.8% CAGR, driven by general fabrication and structural steel demand. Key end-users include construction contractors, shipyards, and heavy equipment manufacturers.

- Automobile Maintenance (28% market share): Fastest-growing segment at 9.1% CAGR, fueled by aging vehicle parcs (average vehicle age exceeding 12 years in North America and Europe) and the proliferation of high-strength steel in unibody construction. Collision repair centers report switching to zirconia alumina wheels for cutting boron steel reinforcements, which destroy conventional wheels in under 30 seconds.

- Construction (18% market share): Moderate growth at 6.2% CAGR, dominated by dry-type wheels for rebar cutting, pipe fabrication, and concrete formwork preparation.

- Others (12% market share – including aerospace, shipbuilding, energy): Premium segment with highest average selling prices, growing at 7.5% CAGR.

A representative case from QYResearch’s field research: A Midwest US automotive collision repair chain replaced standard aluminum oxide wheels with zirconia alumina cut off wheels across 12 locations. The result: wheel change frequency dropped from 4–5 per shift to 1 per shift (74% reduction), cut time per high-strength steel rail section decreased from 45 seconds to 28 seconds (38% improvement), and total annual abrasive spend fell by $47,000 despite a 35% higher unit price.

3. Chinese Manufacturers Rapidly Expand Global Footprint, Creating Two-Tier Pricing

Government-supported advanced manufacturing initiatives under China’s 14th Five-Year Plan (2021–2025) have significantly expanded domestic abrasive production capacity. Companies including ZHEJIANG YIDA ABRASIVE, FUJI Grinding Wheel, and KURE GRINDING WHEEL (Japanese-Chinese joint ventures) have collectively added over 200 million units of annual zirconia alumina wheel capacity since 2024. Their products now compete directly with European and North American incumbents (3M, Saint-Gobain, Tyrolit Group, Klingspor) on price, offering 25–40% lower upfront cost for comparable grain compositions and wheel dimensions.

Critical nuance for procurement professionals: While Chinese-manufactured wheels match or exceed Western products in standard stainless steel cutting applications (304, 316 grades), premium applications requiring extreme consistency—aerospace titanium, medical implant alloys, robotic high-speed cutting cells—still favor established Western and Japanese brands (Noritake, Hermes Schleifmittel, Pferd) with tighter quality control (±2% balance tolerance versus ±5% for mass-market Chinese products). This creates a two-tier sourcing strategy: volume applications sourced from China, precision-critical applications sourced from premium suppliers.

4. Safety and Regulatory Pressures Drive Product Innovation

Recent regulatory developments—including EU Machinery Regulation (EU) 2023/1230 (fully effective January 2026) and OSHA’s updated abrasive wheel standard (29 CFR 1910.243) —have imposed stricter requirements for burst resistance, maximum operating speed markings, and dust emission controls. Leading manufacturers are responding with three innovations:

- Reinforced fiberglass mesh backing: Increases burst speed margins from 1.5x to 2.0x maximum rated speed, reducing catastrophic failure risks.

- Low-vibration wheel designs: Asymmetric grain distribution and precision balancing reduce angle grinder vibration by 30–40%, improving operator comfort and cut accuracy.

- Compliance labeling: RFID-embedded wheels that communicate maximum speed and application limits to smart grinders (emerging technology from Bosch and DEWALT).

For safety managers and plant operators, specifying fully compliant wheels from reputable suppliers (3M, Bosch, Saint-Gobain, Pferd) is no longer just best practice—it is increasingly a legal requirement in regulated markets.

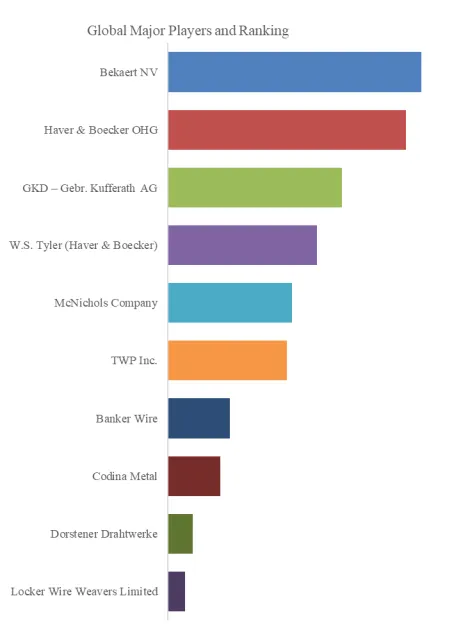

Competitive Landscape: Who Is Shaping the Market?

The global zirconia alumina cut off wheel market is moderately fragmented, with a mix of multinational abrasives giants, power tool manufacturers integrating captive consumables, and specialized regional players. Key players identified in QYResearch’s latest competitive assessment:

Tier 1 – Global Abrasives Leaders: 3M, Saint-Gobain (Norton brand), Tyrolit Group, Klingspor, Noritake, Hermes Schleifmittel, Pferd

Tier 2 – Power Tool Integrated: Bosch, DEWALT (Stanley Black & Decker), Hilti, STIHL

Tier 3 – Strong Regional Specialists: TECHNO ALPHA (Japan), Weiler Corporation (North America), DRONCO (Germany), Rhodius (Germany), FUJI Grinding Wheel (Japan), KURE GRINDING WHEEL (Japan), Camel Grinding Wheels (Italy), Walter Surface Technologies (Canada), Pearl (US), Tomahawk (US), ZHEJIANG YIDA ABRASIVE (China), SHIN-ETSU (Japan)

Segment-by-Type Summary:

- Dry Type: 82% market share, 7.0% CAGR, dominated by construction and field maintenance applications.

- Wet Type: 18% market share, 9.2% CAGR, fastest-growing, driven by automated precision cutting.

Segment-by-Application Summary:

- Metal Processing: 42% share, 6.8% CAGR

- Automobile Maintenance: 28% share, 9.1% CAGR (fastest-growing)

- Construction: 18% share, 6.2% CAGR

- Others (Aerospace, Shipbuilding, Energy): 12% share, 7.5% CAGR

Strategic Recommendations for Decision-Makers

For manufacturing and plant managers: Conduct a TCO analysis comparing your current aluminum oxide wheels against premium zirconia alumina alternatives. Field data consistently shows 30–50% lower cost per cut despite 2–3x higher unit prices, with additional benefits from reduced changeover downtime and lower workpiece rework rates.

For procurement executives: Implement a two-tier sourcing strategy—qualified Chinese suppliers (ZHEJIANG YIDA ABRASIVE, FUJI) for standard stainless steel and carbon steel fabrication; premium Western/Japanese brands (3M, Saint-Gobain, Noritake, Pferd) for aerospace, medical, and automated high-speed applications requiring certified quality consistency.

For CEOs and corporate strategists: The 7.4% CAGR and projected $865 million absolute growth by 2032 justify capacity expansion, particularly in wet-type wheels and region-specific distribution in Southeast Asia, India, and Latin America, where manufacturing activity is growing at 8–10% annually.

For safety and compliance officers: Verify that all wheels used in regulated markets (EU, US, Canada) meet current Machinery Directive or OSHA standards. Prioritize suppliers offering RFID-enabled smart wheels and reinforced burst-resistant designs as competitive differentiators.

Contact Us

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666 (US)

JP: https://www.qyresearch.co.jp