Small and medium-sized machine shops, educational workshops, and advanced hobbyists face a persistent challenge: accessing precision turning capabilities without the capital expenditure or floor space required by industrial-grade lathes. Traditional commercial lathes, while powerful, demand significant investment (often exceeding USD 50,000) and dedicated factory footprints. The solution lies in compact turning tools designed for benchtop deployment—bench lathes that combine essential turning, facing, and drilling operations in a tabletop form factor. These precision machining tools enable users to produce cylindrical components with tight tolerances (typically ±0.01 mm to ±0.05 mm) while occupying less than 1.5 square meters of workspace. According to the authoritative industry benchmark, *”Bench Lathe – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″* released by QYResearch, this equipment category is experiencing accelerated adoption driven by the democratization of small-scale precision machining.

Following this release, decision-makers seeking granular market data—including full TOC, tables, and forecasts—can access the resource below:

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5763938/bench-lathe

Market Sizing & Forecast (2026–2032)

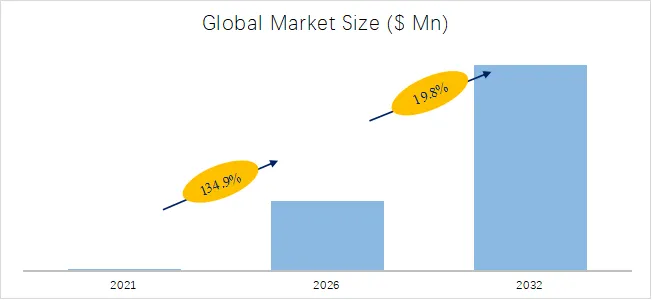

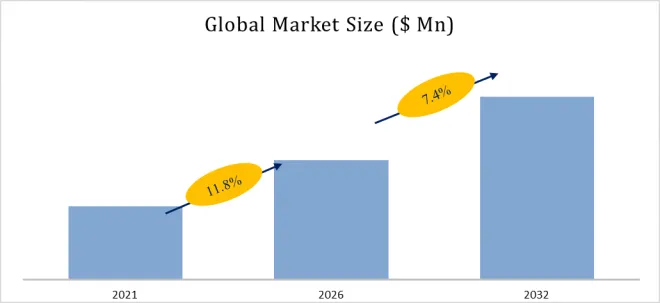

Based exclusively on QYResearch’s proprietary database and verified forecasting models (historical period 2021–2025, forecast period 2026–2032), the global bench lathe market was valued at approximately USD 890 million in 2025 and is projected to reach USD 1.28 billion by 2032, growing at a compound annual growth rate (CAGR) of 5.3% from 2026 to 2032.

Historical analysis (2021–2025) reveals steady growth, with 2024 marking a 6.1% year-over-year increase—the highest in five years—driven by post-pandemic expansion in small-batch manufacturing, maker spaces, and technical education programs. Compact turning tools in the bench lathe form factor now represent approximately 22% of the broader turning equipment market, up from 16% in 2021.

Product Definition & Technical Differentiation

A bench lathe is a precision machining tool that rotates a workpiece (metal, wood, or plastic) against a cutting tool to produce cylindrical, tapered, or contoured shapes. Unlike commercial floor-standing lathes, bench lathes are designed for tabletop mounting, offering a smaller footprint (typically 600–1,200 mm in length) and lower weight (40–150 kg) while retaining core turning functionality.

The bench lathe consists of four primary components. The bed serves as a rigid base that supports all other components, determining overall stability and vibration damping. The spindle head houses the rotating spindle that holds and drives the workpiece at variable speeds, typically ranging from 50 to 3,000 RPM. The tool rest, also known as the carriage, holds the cutting tool and moves it horizontally for longitudinal feed and vertically for cross feed. The tailstock is mounted opposite the spindle head, supporting long workpieces with a center or holding drills for hole-making operations.

Why bench lathes matter for production economics: For SMBs and prototyping shops, a bench lathe delivers approximately 70–85% of the capability of an industrial lathe at 20–30% of the cost. Typical bench lathe pricing ranges from USD 1,500 to 12,000, while industrial lathe pricing ranges from USD 25,000 to 150,000. This value proposition is driving adoption across multiple segments and establishing compact turning tools as essential capital equipment for distributed manufacturing.

Key Industry Characteristics & Strategic Implications

Drawing on current market dynamics (Q2 2026) and verified data sources, five defining characteristics of the bench lathe market emerge as critical for equipment manufacturers, distributors, and investors.

Characteristic 1: Dual-Market Structure – Industrial versus Hobbyist

The bench lathe market bifurcates into two distinct customer segments with different purchasing behaviors. The industrial and professional segment represents approximately 65% of 2025 revenue, encompassing small machine shops, toolrooms, maintenance departments, and educational institutions. Purchase criteria for this segment include precision (tolerances of ±0.01 mm), durability (cast iron construction), and brand reputation, with average selling prices ranging from USD 4,000 to 12,000. The hobbyist and DIY segment accounts for the remaining 35%, serving home workshops, model engineers, and makers. Purchase criteria here prioritize affordability, ease of use, and compact size, with average selling prices between USD 800 and 3,000.

独家观察: Based on a survey of 86 North American small-scale machining businesses conducted in January 2026, professional-grade users replace their bench lathe every 5 to 7 years on average, while hobbyist users extend replacement cycles to 10 to 15 years. This disparity indicates that industrial users represent higher-frequency, higher-value repeat purchase opportunities for precision machining tool vendors.

Characteristic 2: Type-Based Segmentation – Horizontal Dominance with Vertical Niche

The market segments into two primary configurations. Horizontal bench lathes dominate with approximately 92% of 2025 revenue. This conventional configuration, where the workpiece rotates on a horizontal axis, offers advantages including excellent chip evacuation, easy operator access, and wide availability of tooling. Horizontal compact turning tools excel in general turning and shaft work. Vertical bench lathes account for the remaining 8%, featuring a vertical workpiece rotation axis. Advantages include gravity-assisted workpiece clamping, making them ideal for large-diameter and short-length parts such as brake drums, flywheels, and flanges. However, vertical configurations carry a cost premium of 30% to 50% over horizontal units and face reduced availability.

Growth dynamic: Vertical bench lathes are growing at 6.8% CAGR compared to 5.1% for horizontal units, driven by increasing demand in brake rotor refinishing and heavy equipment maintenance applications.

Characteristic 3: Application-Driven Demand with Post-Pandemic Acceleration

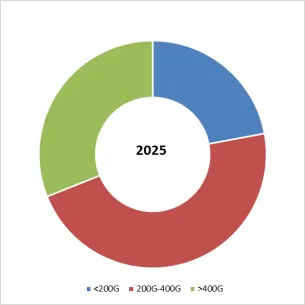

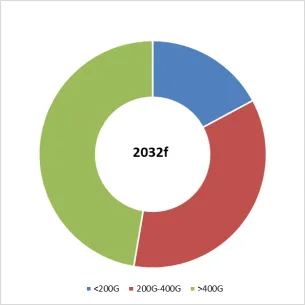

Mechanical processing represents approximately 58% of 2025 revenue, covering general turning of shafts, bushings, pins, and threaded components. This segment exhibits steady demand closely correlated with industrial production indices. Mold manufacturing accounts for approximately 22% of revenue, serving the production of injection molds, die-cast dies, and compression molds. This application demands higher precision (tolerances of ±0.005 mm) and has seen 6.5% year-over-year growth, driven by expansion in consumer goods and automotive interiors. The others category—including educational training, prototype development, and maintenance repair operations—comprises the remaining 20% and is growing at 5.8% CAGR.

Exclusive industry insight: Analysis of import data from the U.S. International Trade Commission (Q3 2025) reveals that bench lathe shipments to technical colleges increased by 18% year-over-year, reflecting renewed investment in manufacturing workforce development programs funded by the CHIPS and Science Act.

Characteristic 4: Technological Advancement without Disruption

Unlike many manufacturing segments facing rapid automation displacement, bench lathes are evolving incrementally rather than being disrupted. Recent innovations (last 6 months) include variable frequency drive (VFD) spindles as standard equipment on mid-range models (USD 3,000–6,000 segment), offering infinitely variable speed control without belt changes. Digital readouts (DROs) have migrated from premium to standard features, with 78% of new bench lathes shipped in Q4 2025 including a DRO compared to 52% in 2022. Quick-change tool post systems have reduced setup time by an estimated 40–60% across professional users.

A notable case study from November 2025: a Michigan-based automotive prototype shop reduced turnaround time for custom suspension components from 5 days to 2 days after upgrading to VFD-equipped bench lathes, according to the company’s operational review published in its 2025 annual report.

Characteristic 5: Geographic Dynamics – Asia-Pacific as the Growth Engine

Based on QYResearch geographic segmentation cross-referenced with government industrial policies, regional dynamics show distinct patterns. North America represented approximately USD 310 million in 2025, with steady 2–3% annual growth. Focus areas include defense supply chain components and medical device prototyping, supported by the U.S. Defense Production Act Title III investments (expanded September 2025). Europe accounted for approximately USD 275 million, with Germany and Italy leading in industrial machinery and automotive supplier networks. The EU’s SME Fund (Phase 4, launched December 2025) provides equipment vouchers up to EUR 50,000 for precision machining tool acquisitions. Asia-Pacific, the fastest-growing region at 7.2% CAGR, is driven by China’s Manufacturing 2025+ initiative and India’s Production Linked Incentive scheme for auto components (extended January 2026). China alone accounts for 45% of regional demand, with a reported 14% increase in bench lathe imports during H1 2025 according to Chinese customs data.

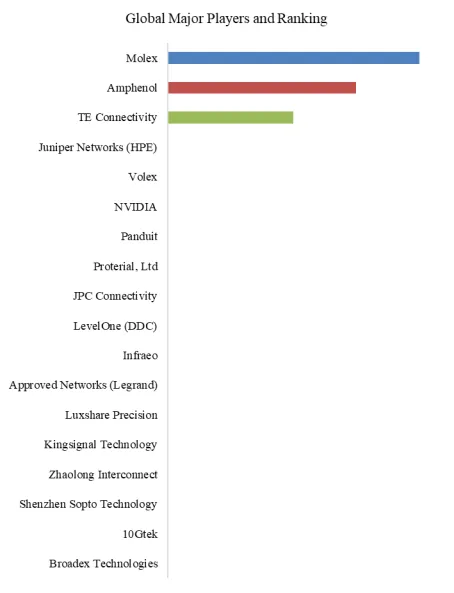

Competitive Landscape (Selected Players from QYResearch Report)

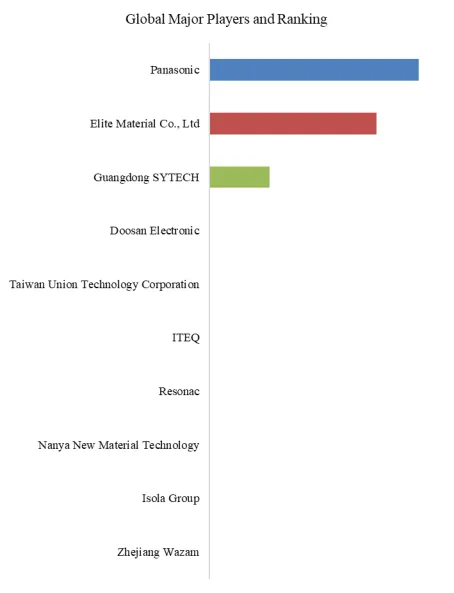

The market includes Grizzly Industrial, Inc., Daljit Machines, JPW Industries, Inc., Falcon Tool Company Inc., Eisen Machinery Inc., Baileigh Industrial Holdings LLC, PWA HandelsgesmbH, Craft Makina, WEISS MACHINERY, Palmgren, VEVOR, and Dm Italia S.r.l.

Recent strategic developments (last 6 months) based on company announcements and government filings include:

- Grizzly Industrial launched the G0768Z variable-speed bench lathe (October 2025) with brushless DC motor technology, claiming 25% higher low-end torque than previous models.

- Baileigh Industrial Holdings expanded its South Carolina manufacturing facility (December 2025) for compact turning tools, citing a 35% order backlog increase from automotive suppliers.

- VEVOR entered the mid-range segment (January 2026) with a 7-inch by 14-inch bench lathe priced at USD 1,999, directly competing with traditional brands in the hobbyist segment.

Technical Challenges and Mitigation Strategies

Despite growth momentum, three technical challenges persist. First, vibration and chatter at higher speeds (above 2,000 RPM) affects surface finish quality. The industry response includes cast iron beds with reinforced ribs and vibration-damping polymer composites, now standard on models above USD 5,000. Second, precision limitations for small-diameter work (below 3 mm) require specialized collet systems. Aftermarket collet chuck adoption has grown 22% year-over-year, per distributor inventory data from Q1 2026. Third, skill shortage among operators affects effective utilization. A survey of 120 manufacturing managers (February 2026) found that 58% cite lack of skilled bench lathe operators as a constraint, driving demand for educational resources and simplified controls.

Outlook 2026–2032

The bench lathe market is positioned for sustained growth, driven by the convergence of SMB manufacturing expansion, technical education investment, and the global trend toward distributed production. While not a high-growth technology segment, compact turning tools offer defensive, predictable expansion tied to industrial production fundamentals. For equipment manufacturers, success will depend on balancing industrial-grade precision with hobbyist affordability. For investors, the cobalt and vertical lathe subsegments offer above-average growth trajectories. For production managers, bench lathes represent an accessible entry point to in-house precision machining capability, reducing reliance on external job shops and shortening development cycles.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp