QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “300kW Fuel Cell Stack- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global 300kW Fuel Cell Stack market, including market size, share, demand, industry development status, and forecasts for the next few years.

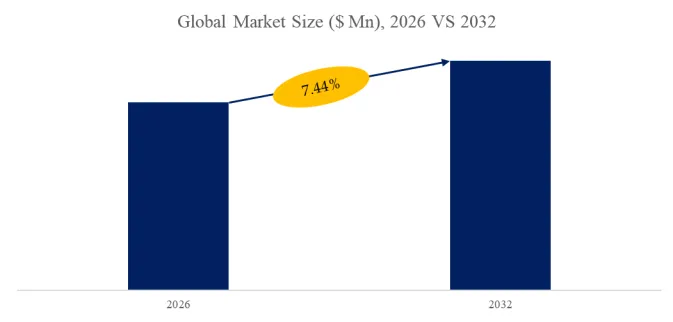

The global market for 300kW Fuel Cell Stack was estimated to be worth US$ 78.00 million in 2025 and is projected to reach US$ 207 million, growing at a CAGR of 15.0% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5772191/300kw-fuel-cell-stack

1. 300kW Fuel Cell Stack Introduction

The 300kW fuel cell stack, as a high-end product within the hydrogen fuel cell technology system, refers to the core component of a proton exchange membrane fuel cell or solid oxide fuel cell that achieves a rated power of 300 kilowatts per stack. This product is characterized by significant features including high power density, excellent system efficiency, and environmental friendliness, with a rated power typically ranging from 300 to 310 kilowatts, a peak power reaching 340 to 380 kilowatts, a volumetric power density exceeding 4.6 to 6.4 kilowatts per liter, and a gravimetric power density surpassing 900 watts per kilogram. The 300kW stack primarily adopts the technical route of metal or carbon composite bipolar plates, wherein the metal plate stack utilizes ultra-thin metal material measuring 0.075 millimeters, which is over 25 percent thinner than a sheet of A4 paper, achieving high power density through precision stamping and surface treatment processes. This product holds broad application prospects in fields such as heavy-duty commercial vehicles, marine propulsion, and distributed power generation, serving as a key technological enabler for scaling the hydrogen energy industry.

2. 300kW Fuel Cell Stack Development Factors

2.1. Differentiated Development Paths of 300kW-class and Above Fuel Cell Systems under the Multi-Technology Route Competition Landscape

In the development process of 300kW and above fuel cell systems, competition from multiple technology routes such as battery electrification, traditional internal combustion engines, and hydrogen fuel internal combustion engines will continue to shape their future technological positioning and application boundaries. From the perspective of battery electrification, according to the New Energy Vehicle Industry Development Plan (2021-2035) and public statements from multiple vehicle manufacturers, lithium battery technology has formed mature advantages in the passenger vehicle and medium-short distance transportation fields. However, in heavy-duty, long-distance, and high-frequency operation scenarios, constrained by energy replenishment efficiency and vehicle load limitations, the industry generally regards fuel cells as an important complementary pathway, especially in trunk logistics and high-intensity operation vehicles, where 300kW and above systems are more suitable for actual needs. This “scenario division” trend is also reflected in the policies of the Ministry of Transport and local demonstration policies, promoting the two types of technologies to form a synergistic rather than substitutive relationship. In terms of traditional internal combustion engines and gas turbines, although they still hold advantages in cost, industrial chain maturity, and maintenance systems, the carbon peaking and carbon neutrality policy system continuously advanced by the Ministry of Ecology and Environment, as well as the construction of the national carbon emission trading market, are gradually increasing the usage costs of high-emission technologies. Multiple energy and equipment enterprises have clearly included hydrogen energy and fuel cells in their medium- and long-term transformation directions in their annual reports and announcements, which will provide clearer substitution space for 300kW-class fuel cell systems in heavy-duty equipment and stationary power fields. At the same time, some enterprises are also exploring hybrid systems of fuel cells and traditional power to balance economic viability and emission reduction needs in the transition phase. For the hydrogen fuel internal combustion engine route, the Ministry of Industry and Information Technology has listed it as one of the hydrogen energy utilization pathways in relevant technology advancement documents, and multiple commercial vehicle enterprises have released hydrogen internal combustion engine prototypes or test projects. However, according to enterprise technical descriptions and publicly released information, this route still has gaps with fuel cells in thermal efficiency and emission control, so it is more likely to be applied in subdivided scenarios that are cost-sensitive and have relatively relaxed emission requirements. In fields with stricter requirements for high efficiency and zero emissions, such as port transportation, urban logistics, and stationary power generation, 300kW and above fuel cell systems still possess clearer policy and technological advantages. Overall, under the pattern of parallel development of multiple pathways, policy guidance, carbon constraint mechanisms, and enterprise technology choices will jointly drive fuel cells toward high power, high efficiency, and high reliability, and establish a differentiated competitive position with 300kW and above systems as the core in heavy-duty and long-cycle operation scenarios.

2.2. Key Development Drivers for Large-Scale Application of 300kW-class Fuel Cell Stack under the Traction of Multi-Scenario Demands

Focusing on the three core application scenarios of heavy truck transportation, marine propulsion, and distributed power generation, the development factors of 300kW fuel cell stack present a comprehensive characteristic of “high-power adaptation to rigid-demand scenarios, system efficiency advantages driving substitution, and infrastructure and policy synergy amplifying application scale.” In the heavy truck transportation field, the transportation industry’s evolution toward long-distance, high-load, and high attendance rates requires the power system to balance continuous power output and rapid energy replenishment capabilities. The 300kW-class stack has been able to benchmark traditional large-displacement diesel engines in power performance, meeting the mainstream operating conditions of trunk logistics. At the same time, the hybrid architecture of fuel cells and power batteries achieves the optimal efficiency operating range. This technical pathway has been repeatedly verified by domestic mainstream vehicle manufacturers in product releases and announcements. Combined with policies such as highway toll exemptions and demonstration operation subsidies in various regions, it significantly enhances its commercial viability in heavy-duty transportation. In the marine field, the International Maritime Organization’s emission reduction targets and relevant specifications of the China Classification Society continue to tighten emission requirements, driving ship power toward zero-emission and low-noise transformation. The 300kW stack has the capability to serve directly as the main power in small and medium-sized ships and, in large ships, assumes auxiliary power or power generation units in a modular form. Multiple international shipping enterprises and shipyards have verified its engineering feasibility through demonstration projects. At the same time, the high-standard requirements for system reliability, environmental adaptability, and safety in complex ship operating environments have conversely driven continuous improvements in stack technology in terms of lifetime, sealing, and system integration. In the distributed power generation field, the national “dual carbon” goals and the green transformation requirements of data centers have made zero-emission, high-reliability backup and primary power sources a rigid demand. The 300kW-class system, due to its modular deployment capability and high power generation efficiency, has been incorporated into actual application solutions by multiple energy enterprises and internet companies, playing a key role in the integrated model of “renewable energy hydrogen production—hydrogen storage—fuel cell power generation.” At the same time, its combined heat and power capability gives it comprehensive energy utilization advantages in industrial parks and commercial buildings. Overall, the demand for high power density and endurance in heavy-duty transportation, the institutional constraints on zero-emission power in the shipping industry, and the practical dependence of distributed energy systems on stable and clean power sources together constitute the most direct driving factors for the development of 300kW fuel cell stack, while policy support, demonstration projects, and energy system transformation further amplify its large-scale application trend.

2.3. Analysis of the Two Engines Driving the Development of 300kW Fuel Cell Stack: Technological Depth Breakthrough and Commercialization Horizontal Expansion

The development of 300kW fuel cell stack presents a pattern of parallel vertical advancement and horizontal expansion in the two dimensions of technology development and commercialization landing. From the perspective of technology development, its evolution has always revolved around the three main lines of power density improvement, durability enhancement, and system integration optimization. In terms of power density, material innovation and structural design form a dual force: the thickness of ultra-thin metal bipolar plates has broken through to 0.075 mm, and platinum loading has been reduced to below 0.15 mg/cm², laying the foundation for lightweighting and cost control; structural optimizations such as nested three-dimensional flow fields have pushed the volumetric power density from the mainstream 4.6–6.4 kW/L toward the laboratory peak of 9.8 kW/L. In terms of durability, catalyst stability has become the core breakthrough point. New designs such as mixed-phase catalysts can extend lifetime to 200,000 hours, far exceeding the current commercial target of 30,000 hours. At the same time, membrane electrode improvement schemes such as gradient catalyst layers and cross-linked proton exchange membranes, in synergy with intelligent water and thermal management strategies, significantly suppress performance degradation. At the system integration level, the focus is on the collaborative optimization of thermal management, hydrogen supply, and power electronics. Low-temperature self-heating technology enables -35°C cold start, while self-humidification and silicon carbide power devices improve system efficiency and power density, enabling large-power stacks to move from single-point breakthroughs toward high-efficiency and high-reliability of the entire system. From the perspective of commercialization landing, the development focus of 300kW stacks is shifting from technology verification to cost control, supply chain construction, and business model innovation. Cost structure analysis shows that the stack cost accounts for 40%–63% of the total system cost, of which catalysts, proton exchange membranes, and bipolar plates together account for more than 70% of the stack cost. Therefore, cost reduction strategies focus on three major paths: at the material level, low-platinum and localization efforts reduce platinum loading by more than 60% and halve the price of proton exchange membranes; at the manufacturing level, automated production lines increase production efficiency by 3 times and reduce unit manufacturing costs by 60%; at the scale level, the leap from thousand-unit to ten-thousand-unit levels enables rapid amortization of fixed costs. Supply chain system construction simultaneously advances the localization of key materials (proton exchange membranes, catalysts, gas diffusion layers) and the autonomy of core equipment to address the current bottlenecks of high dependence on imports for high-end materials and insufficient industrial chain coordination. On this basis, business models are evolving from single product sales to composite models such as “product + service,” equipment leasing, energy contract management (EMC), and “hydrogen-electricity integration,” effectively lowering the user’s initial investment threshold, extending the value acquisition chain, and promoting the accelerated penetration of 300kW stacks from demonstration applications to large-scale deployment in scenarios such as heavy trucks, logistics parks, and data centers. It is precisely that technology development provides performance and reliability support for commercialization, while commercialization provides cost feedback and application scenarios for technology iteration. The two form a mutually reinforcing and spiraling development force, constituting the fundamental driving force for the rapid breakthroughs of 300kW fuel cell stack in the past five years.

3. 300kW Fuel Cell Stack Development Trends

3.1. The 300kW Fuel Cell Stack: A Technological Evolution Toward High Power Density and Cost Reduction

Currently, China has achieved key technological breakthroughs and industrial implementation in the field of 300kW fuel cell stacks, with future development trends characterized by the dual drivers of continuously improving power density and accelerating cost reduction. From a technical perspective, third-generation 300kW stacks, represented by products that have optimized flow field design and material innovation, have achieved a leap in power density from previous generation levels to an internationally leading level, accompanied by a significant extension in operational lifespan. Leveraging advanced technologies such as dual-ejector hydrogen supply, energy recovery, and intelligent algorithms, these systems can now start in extremely low-temperature environments, meeting the demanding power requirements of long-endurance, heavy-load applications including mining trucks, heavy-duty haulers, and marine vessels. Industry consensus indicates that the next phase of technological development will focus on further surpassing power density thresholds, extending stack longevity to several tens of thousands of hours, and continuously expanding the high-efficiency operating range. Achieving these goals necessitates a better balance between high-performance catalyst loading and durability, alongside substantial progress in critical bottlenecks such as high-temperature durable membrane electrode assemblies and bipolar plate design. On the industrialization and cost front, driven by a rapidly increasing localization rate of key materials and components, leading domestic manufacturers have established fully automated production lines with significant annual capacities. By adhering to stringent quality management system certifications to ensure product consistency, these efforts have facilitated a marked reduction in the cost of high-power stacks. Through platform-based and integrated design strategies, coupled with the widespread adoption of material substitution—including graphite and metal bipolar plates, domestically produced proton exchange membranes, and novel catalysts—domestic manufacturers have substantially lowered manufacturing costs while laying the groundwork for achieving long-term cost reduction targets. Although challenges remain concerning the dependence on platinum group metals in catalysts, the industry is progressively establishing a sustainable closed-loop system by constructing large-scale catalyst recycling facilities to enhance material circularity. Looking ahead, the 300kW fuel cell stack will target large-scale hydrogen application scenarios such as heavy-duty commercial vehicles, large construction machinery, and marine vessels. Through continuous technological iteration and whole-industry-chain collaboration, it will aim to simultaneously enhance power density, durability, and environmental adaptability while relentlessly reducing costs, thereby accelerating its transition into a new phase of commercial proliferation.

3.2. Powering the Future: The High-Power Leap of 300kW Fuel Cell Stacks Under Policy Guidance and Supply Chain Synergy

Under the top-level design of the Medium and Long-Term Plan for the Development of the Hydrogen Energy Industry issued by the National Energy Administration, which sets phased goals of achieving approximately 50,000 fuel cell vehicles and 100,000 to 200,000 tons of renewable hydrogen production capacity annually by 2025, and further solidified by the formal inclusion of hydrogen into the national energy management framework through the Energy Law of the People‘s Republic of China, China’s fuel cell industry is rapidly concentrating on heavy-duty and long-haul applications. This strategic focus is reinforced by substantial purchase subsidies for heavy trucks with a power rating of 80kW or above, with national subsidies ranging from 171,000 to 378,000 yuan in 2023, complemented by various local supporting policies. Such momentum has directly fueled the demand for 300kW-class high-power fuel cell stacks, as achieving this power level is essential to meet the performance requirements of heavy trucks under high-speed and full-load conditions, enabling hydrogen to effectively replace traditional diesel in commercial operations. Concurrently, the refinement of regulatory and standard systems is paving the way for the large-scale deployment of 300kW stacks. From the Energy Law establishing hydrogen’s role in the energy sector, to the formulation of international hydrogen quality standards (ISO14687), and the accelerated development of national technical specifications for hydrogen refueling stations (GB/T34425) alongside various standards for fuel cell system components, a comprehensive standardization framework covering the entire “production, storage, transportation, and utilization” chain is taking shape. Active participation by leading enterprises in standard-setting ensures that technological advancement and regulatory evolution progress in tandem, providing clear technical guidelines and safety assurance for the engineering and deployment of 300kW-class products.

On the supply chain and raw materials front, the evolution of the 300kW stack is deeply intertwined with the localization of critical materials and the diversification of green hydrogen sources. To meet the durability demands of higher-power, higher-current-density stacks, domestic catalyst manufacturers have achieved a significant milestone by moving from platinum-carbon to mass-produced platinum-cobalt alloy catalysts. Leveraging technologies like platinum-cobalt superlattice structures, these products reduce membrane electrode platinum loading while enhancing activity and stability, directly addressing the core challenge of balancing precious metal usage with high performance in 300kW stacks. Although the catalyst market remains dominated by foreign firms, domestic players are advancing technologies such as single-atom platinum-carbon to control platinum group metal loading at low levels. By forging strategic partnerships with upstream precious metal suppliers and establishing a closed-loop recycling system—including the commissioning of the first large-scale carbonyl tailings processing line to enhance platinum group metal security—domestic manufacturers are removing critical material bottlenecks and cost barriers for mass production of 300kW stacks. On the hydrogen source side, national plans explicitly target scaling renewable hydrogen production to 100,000–200,000 tons annually while encouraging the utilization of industrial byproduct hydrogen. As green hydrogen production costs continue to decline and electrolysis equipment becomes more compact and efficient, the hydrogen supply for 300kW-class stacks will become increasingly diversified, encompassing water electrolysis, natural gas reforming, and liquid hydrogen transport. This evolution will not only determine the lifecycle carbon footprint of the stacks but also ensure that large-scale heavy-duty trucks powered by 300kW stacks have access to sufficient, low-carbon fuel for demonstration projects. Such a synergy between high-power stacks and green hydrogen is critical for advancing the commercial viability of hydrogen heavy trucks, particularly in typical application scenarios like “hydrogen highways” and port logistics, bringing them closer to a technological and economic tipping point.

3.3. The 300kW Fuel Cell Stack: Application Expansion and Performance Differentiation Driven by Multiple Scenarios

As hydrogen transportation transitions from demonstration projects to large-scale deployment, the market demand for 300kW fuel cell stacks is accelerating its expansion from a single heavy-duty scenario toward a diversified application matrix, with different use cases imposing differentiated and sometimes mutually constraining technical requirements on stack performance. In the commercial vehicle sector, hydrogen fuel cell heavy-duty trucks remain the most core driving force for 300kW stacks. For long-haul logistics applications, multiple mainstream vehicle manufacturers have launched purpose-built heavy-duty truck products equipped with 300kW high-power fuel cell systems. Through hydrogen-electric integrated chassis and deeply integrated powertrain designs, these vehicles meet the long-endurance and heavy-load climbing demands of 49-ton tractors under fully loaded conditions, achieving significant improvements in overall fuel cell system efficiency while maintaining stable operation under extreme high, low, and high-altitude environments. Concurrently, policy support through the establishment of fuel cell vehicle demonstration city clusters, with heavy-duty trucks designated as a priority area, explicitly supports the promotion and application of long-haul heavy-load scenarios. Several provincial-level jurisdictions have also implemented toll waivers on expressways for hydrogen vehicles, further reducing the total lifecycle operating costs of hydrogen heavy-duty trucks. In the public transportation domain, buses equipped with 300kW-class fuel cell systems are gradually being integrated into urban and intercity passenger networks, with their system efficiency and low-temperature start capability meeting operational requirements in standard urban routes and cold winter regions. In the stationary power generation field, 300kW-class solid oxide fuel cell systems are accelerating their entry into distributed power stations and microgrid markets. Represented by companies such as Doosan, intermediate-temperature SOFC products operating at specified temperatures achieve relatively high power generation efficiency and multi-year stack service life, making them suitable for combined heat and power applications and building backup power, where fast response capability and high operational reliability are required, along with the ability to independently support loads under islanded grid conditions. In the emerging maritime application sector, 300kW-class fuel cell systems are advancing from pilot validation to engineering demonstration phases. Multiple international classification societies have completed environmental testing standard certifications for marine SOFC core stacks, with 300kW systems designed as auxiliary power units for LNG carriers and ocean-going vessels, undergoing real-voyage validation periods exceeding one year to verify stability and efficiency under harsh marine conditions including high humidity, high salinity, vibration, and motion. Different application scenarios impose distinct performance priorities on 300kW stacks: long-haul heavy-duty trucks pursue a comprehensive balance among power density, durability, and environmental adaptability, emphasizing performance stability over a service life spanning tens of thousands of hours; stationary power generation focuses more on system efficiency, combined heat and power capability, and long-term maintenance-free operation, with relatively lower sensitivity to power density; maritime applications place higher demands on safety, vibration and shock resistance, and multi-fuel compatibility. This multi-scenario market demand pattern, with each scenario possessing unique characteristics, is driving the evolution of 300kW fuel cell stacks from a single technology pathway toward scenario-customized development. Through differentiated design in membrane electrode assembly catalyst formulations, bipolar plate flow field structures, system thermal management strategies, and control algorithms, a full-scenario product portfolio covering on-road freight, public transportation, stationary power, and marine propulsion will be formed, ultimately enabling high-power fuel cell technology to achieve a transformative leap from demonstration validation to commercial sustainability.

4. Leading Manufacturer in the Industry

Accelera is the zero-emissions business unit of Cummins Inc. Operating as a comprehensive technology integrator and component supplier, it is dedicated to accelerating the transition to a sustainable future for the world’s most critical industries. Its business portfolio spans a broad range of advanced technologies, including hydrogen fuel cells, battery systems, e-axles, traction systems, integrated electric powertrains, and electrolyzers for green hydrogen production. By integrating these core technologies, Accelera delivers tailored power solutions for heavy-duty applications, aiming to drive decarbonization across sectors ranging from commercial transportation and rail to stationary power and carbon-intensive industrial operations.

Accelera offers a 300kW Fuel Cell Stack specifically designed for heavy-duty on-highway and off-highway applications, with a design focus on modularity, ease of integration, and serviceability. This product is available in two types to meet different operational needs: metal bipolar plate stacks and graphite bipolar plate stacks. This dual-track technology approach enables Accelera to fully leverage the distinct characteristics of different materials, providing customers with flexible options to optimize performance and durability for specific use cases within the zero-emissions ecosystem.

4.1.1. Key Features of FCE300

Accelera’s FCE300 is Accelera’s advanced 4th generation 300kW Fuel Cell Stack purpose-built for heavy-duty on- and off-highway applications and crafted with a focus on modularity, ease-of-integration, and serviceability, incorporating advanced PEM stack technology with a fully-integrated balance-of-plant that includes DC/DC converter and thermal management system for simplified integration and enhanced efficiency, along with progressive on-board controls and diagnostics, variable pressure cathode air delivery, an externally humidified stack, and reliable operation down to -30 degrees Celsius. This 300kW Fuel Cell Stack delivers a rated power of 300kW comprised of two FCE150 units, with an operating current of 0 to 330 ADC per unit, operating voltage range of 450 to 850 VDC, peak efficiency of 55 percent under the heavy-duty truck duty cycle, response time of 30kW/s ramp-up and 45kW/s ramp-down, durability of up to 20,000 hours, coolant consisting of a 50/50 mix of de-ionized water and ethylene glycol, coolant temperature range of 62 to 83 degrees Celsius continuous with a maximum of 85 degrees Celsius, ambient operating temperature range without derating from -30 degrees Celsius to 45 degrees Celsius, storage temperature range from -40 degrees Celsius to 85 degrees Celsius with automated freeze preparation, CAN J1939 communication protocol supporting 250 and 500 kbps baud rates, compact dimensions of 1342 x 789 x 955 mm including the DC/DC and TMS, mass of 690 kg, volume of 1011 liters, and IP66/IP67 ingress protection, thereby providing innovative decarbonized power solutions for medium-duty trucks as well as bus, coach, transit, and intercity applications that keep the world running.

4.2. Shanghai FTXT Energy Technology

Shanghai FTXT Energy Technology focuses on the two major systems of fuel cells and hydrogen storage, establishing an integrated industrial chain development model encompassing “production, storage, transportation, refueling, and application” . As a high-tech enterprise committed to becoming a globally leading comprehensive service provider in the hydrogen energy industry, its core business covers the research, development, manufacturing, and sales of fuel cell engines, stacks, membrane electrodes, and onboard hydrogen storage systems, including hydrogen storage cylinders, cylinder valves, and pressure reducing valves . The company provides customers with integrated, full-scenario, and full-domain comprehensive solutions across the entire industrial chain. Its products have been widely applied in areas such as logistics transportation, urban sanitation, public transit, and maritime shipping, achieving large-scale implementation across multiple national hydrogen demonstration city clusters .

FTXT’s self-developed new-generation G30 Fuel Cell Stack is a high-power water-cooled stack with a rated power of 300kW, capable of meeting the power requirements of fuel cell systems ranging from the hundred-kilowatt to megawatt level . This series of stacks employs a dual-technology roadmap strategy in its technical approach, specifically including a stack type utilizing a metal bipolar plate and a stack type utilizing a new-generation ultra-thin graphite bipolar plate . Among these, the graphite bipolar plate stack is equipped with FTXT’s self-developed low-platinum, high-durability membrane electrode assembly, while the metal bipolar plate stack offers advantages in power density. Together, these technologies achieve breakthroughs in durability, conversion efficiency, and environmental adaptability.

4.2.1. Key Features of G30

Shanghai FTXT Energy Technology independently developed a new generation of 300kW+ high-power water-cooled fuel cell stack; it adopts the low-platinum and high-durability membrane electrode independently developed by FTXT Energy, matched with the company’s new generation of ultra-thin graphite bipolar plates; it can be modularly combined according to customer power requirements and usage scenario requirements to achieve customized development. The G30 fuel cell stack has a rated power of 300kW, with a voltage range of 502.5~750V, a current range of 0~600A, a stack core volumetric power density of 3.6kW/L, a cold start temperature as low as -30°C, and a durability of up to 20,000 hours, featuring high voltage consistency; the electrical conversion efficiency under rated power can reach 53.4%, with a wide power applicability range that can meet the power requirements of hundred-kilowatt to megawatt-level fuel cell systems.

4.3. Beijing Nowogen

Beijing Nowogen Technology Co., Ltd. focuses on the research, development, manufacturing, and sales of fuel cell stacks. It is one of the few domestic manufacturers of fuel cell stacks with core proprietary intellectual property rights and industrialization capabilities, and it is recognized as the creator of China’s first automated production line for fuel cell stacks with independent intellectual property rights. The company is dedicated to the industrialization and marketization of new energy technologies, with its core business encompassing fuel cell stack development, related technology research, product design, and manufacturing. Its products are widely applied across various sectors, including heavy-duty trucks, maritime shipping, stationary power generation, forklifts, and sanitation vehicles, actively promoting the commercial application of fuel cell technology in transportation and industrial fields.

Beijing Nowogen Technology Co., Ltd.’s self-developed 300kW Fuel Cell Stack belongs to its sixth-generation carbon composite plate stack product line, utilizing a carbon composite (graphite) bipolar plate technology path. This stack has been tested by an authoritative institution, achieving a rated power of 309kW and a peak power of 340kW, making it suitable for applications such as heavy-duty trucks, maritime shipping, and stationary power generation. Technologically, the stack features an ultra-large single-cell active area and ultra-thin bipolar plates, while its maximum operating temperature has been elevated to optimize the efficiency of the thermal management system.

4.3.1. Key Features of ST300VIC

The ST300VIC is classified as a 300kW Fuel Cell Stack, with a rated output power of 300kW at 0.65V and a peak power of 340kW at 0.65V. Regarding operating pressure, the anode pressure does not exceed 170kPa and the cathode pressure does not exceed 155kPa, with an operating temperature not exceeding 90°C. The stack achieves a power density of 4.6kW/L at the peak power of 340kW, and has a design life of 30,000 hours. The stack dimensions are 960mm × 427mm × 180mm, with a mass of 120kg. The operating voltage range is 346V to 550V, and the operating current range is 43A to 978A.

4.4. Shanghai Jichong Hydrogen Technology

Shanghai Jichong Hydrogen Technology focuses on the research and development as well as industrialization of fuel cell technology and serves as a vehicle hydrogen fuel cell stack solution provider. Its business covers the customized development, sales, and technical services of fuel cell stacks. The company has established a unique forward development system for vehicle fuel cell stacks by integrating fuel cell knowledge with vehicle product development processes and advancing from three aspects including product design, process development, and capacity realization. It is committed to promoting the commercialization of fuel cells through independent intellectual property rights and has built a professional team mainly composed of young and middle-aged engineers. Its products are applied in various vehicle types such as commercial vehicles, and the company actively expands into related fields including portable fuel cell applications, continuously enhancing product economic viability and reliability to support the broader adoption of hydrogen energy in transportation and energy sectors.

Shanghai Jichong Hydrogen Technology has developed 300kW Fuel Cell Stack products that demonstrate strong performance in high-power scenarios and can match 300kW-class systems to cover most commercial vehicle applications while extending to fields such as marine, aviation, large engineering machinery, and energy equipment. Its 300kW Fuel Cell Stack is divided into metal bipolar plate stack and graphite bipolar plate stack types, with the metal bipolar plate stack as the core product line represented by the MH series that adopts the international mainstream metal bipolar plate technology route featuring independent research and development in bipolar plate design, sealing, and coating technologies. This type emphasizes advantages in power density, low-temperature startup capability, and durability through continuous iteration and has achieved successful matching with multiple vehicle models and accumulated extensive operation experience. In contrast, graphite bipolar plate stacks represent another technical pathway, and the company’s development aligns with industry practices where both metal and graphite routes coexist to meet differentiated demands in power, cost, and application scenarios, thereby providing comprehensive high-power stack solutions that contribute to the advancement of fuel cell technology toward higher efficiency and reliability.

4.4.1. Key Features of MH Series

The MH170 from Shanghai Jichong Hydrogen Technology is a high-power metal bipolar plate stack product developed for 300kW-class and above fuel cell systems. It adopts a fully localized design with independent intellectual property rights and features core characteristics such as high power density, high reliability, and system-friendly adaptability. Its single-stack output power can reach over 200kW and has achieved a maximum power level of 376kW, enabling it to directly match the requirements of 300kW-class fuel cell systems and meet the power configuration needs of high-load scenarios such as heavy-duty commercial vehicles, construction machinery, and ships. In terms of performance, the bare stack achieves a volumetric power density of 4.7kW/L and a gravimetric power density of 4.0kW/kg, balancing high power output with lightweight design. It also supports low-pressure operation, external humidifier-free running, and a wide operating condition window, effectively reducing system complexity and the difficulty of vehicle integration. In terms of environmental adaptability, the MH170 possesses -40°C low-temperature storage capability and -39°C auxiliary-free startup ability, making it suitable for complex conditions such as high-cold and high-altitude environments and significantly expanding its application regions. In terms of lifetime and reliability, the product adopts fourth-generation corrosion-resistant non-precious metal coated bipolar plates and an integrated die-casting encapsulation design. Combined with long-term failure mode optimization experience, it achieves a lifetime exceeding 15,000 hours in commercial vehicle scenarios and ensures stable operation under extreme conditions such as cell reversal. At the manufacturing and cost level, relying on fully automated intelligent production lines and a localized material system, the MH170 significantly reduces manufacturing costs and improves large-scale production efficiency while maintaining performance. Overall, through its high-power output capability, excellent environmental adaptability, and system-level low-cost integration advantages, the MH170 stack has become a core stack solution adapted to 300kW Fuel Cell Stack systems and is capable of covering diverse high-power application scenarios such as heavy truck transportation, marine propulsion, and distributed energy.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The 300kW Fuel Cell Stack market is segmented as below:

By Company

EH Group

INOCEL

Bosch

Ballard

Cummins

Horizon Fuel Cell

Intelligent Energy

Shanghai Shen-Li High Tech

Shanghai FTXT Energy Technology

Shanghai REFIRE Group

Sino-Synergy Hydrogen Energy Technology (Jiaxing)

Shanghai Jichong Energy

Shanghai H-RISE New Energy Technology

Segment by Type

Carbon Composite Plate Stack

Sheet Metal Stack

Segment by Application

City Delivery

Material Handling

Small And Medium-Sized Construction Equipment

Other

Each chapter of the report provides detailed information for readers to further understand the 300kW Fuel Cell Stack market:

Chapter 1: Introduces the report scope of the 300kW Fuel Cell Stack report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of 300kW Fuel Cell Stack manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various 300kW Fuel Cell Stack market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of 300kW Fuel Cell Stack in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of 300kW Fuel Cell Stack in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth 300kW Fuel Cell Stack competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides 300kW Fuel Cell Stack comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides 300kW Fuel Cell Stack market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global 300kW Fuel Cell Stack Market Outlook, In‑Depth Analysis & Forecast to 2032

Global 300kW Fuel Cell Stack Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global 300kW Fuel Cell Stack Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp