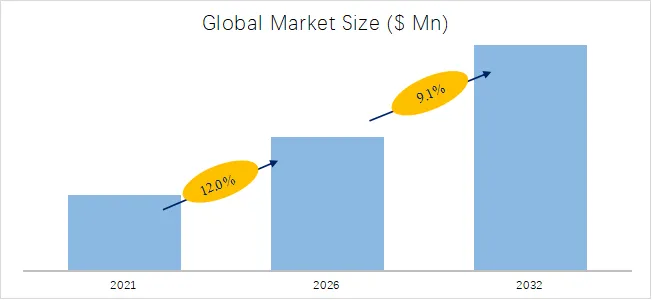

For grid operators facing renewable intermittency, data center facility managers requiring uninterruptible power supplies (UPS) with zero degradation, and electric transportation engineers seeking regenerative braking capture, a critical gap exists. Chemical batteries excel at long-duration storage but degrade rapidly under high-cycle, high-power charge/discharge events. They also pose thermal runaway risks. Flywheel energy storage equipment directly resolves these pain points by storing energy kinetically in a spinning mass, offering near-instantaneous response (milliseconds), unlimited cycle life without capacity fade, and zero hazardous materials. According to the latest industry benchmark, the global market for Flywheel Energy Storage Equipment was valued at USD 115 million in 2025 and is projected to reach USD 498 million by 2032, growing at an exceptional compound annual growth rate (CAGR) of 23.6% from 2026 to 2032. This explosive growth reflects accelerating adoption of flywheel energy storage across industrial UPS, electric transportation infrastructure, and aerospace power quality applications.

*Global Leading Market Research Publisher QYResearch announces the release of its latest report “Flywheel Energy Storage Equipment – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Flywheel Energy Storage Equipment market, including market size, share, demand, industry development status, and forecasts for the next few years.*

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5760790/flywheel-energy-storage-equipment

1. Product Definition: Kinetic Battery for High-Power Applications

Flywheel energy storage is a technology that converts and stores electrical energy as rotational mechanical energy using a spinning flywheel (rotor). The fundamental principle: electrical energy accelerates the flywheel to high rotational speeds (typically 15,000–60,000 rpm), storing energy kinetically. When electricity is needed, the flywheel’s momentum drives a generator (or acts as a motor in reverse), converting mechanical energy back to electrical energy for the power supply system. This bi-directional energy conversion happens within milliseconds—10 to 100 times faster than chemical battery response times.

Core components of flywheel energy storage equipment include:

- Rotating part (flywheel) – Typically a steel or composite rotor engineered for high strength-to-weight ratio

- Bearing system – Mechanical bearings (for lower speed) or magnetic bearings (for high-speed, low-loss operation)

- Generator/motor unit – Permanent magnet synchronous machine (PMSM) or induction machine

- Electronic control system – Power electronics for grid interfacing, voltage regulation, and speed control

- Housing and protection system – Vacuum enclosure to minimize aerodynamic drag, plus safety containment for rotor failure

Unique value proposition: Unlike batteries, flywheels experience no capacity degradation over cycling—they can complete hundreds of thousands of full-depth charge/discharge cycles with <1% performance loss. This makes them ideal for applications requiring frequent, high-power pulses.

2. Industry Development Trends: Energy Density, Intelligence, and Application Expansion

Based on analysis of corporate annual reports, government policy documents (US Department of Energy Grid Modernization Initiative, EU Clean Energy Package), and industry news from Q4 2025 to Q2 2026, four dominant trends shape the flywheel storage sector:

2.1 Energy Density Improvement – The Critical Path to e-Mobility

One of the future development trends of flywheel energy storage equipment is to increase energy density (watt-hour per kilogram or per liter) to better address scenarios with higher capacity requirements, such as electric transportation. Recent advances in carbon-fiber composite rotors (introduced by Amber Kinetics in Q1 2026) have achieved 40% higher energy density compared to steel rotors, making flywheel-only range extenders for buses and trams commercially viable. At the same time, high-temperature superconducting (HTS) bearings, demonstrated by Temporal Power in December 2025, reduce standby losses to under 1% per hour – a critical enabler for multi-hour storage.

2.2 Intelligence and Adaptive Control

Flywheel energy storage systems are becoming more intelligent, including more advanced electronic control systems, remote monitoring, and adaptive control to improve overall system performance. Modern systems now incorporate:

- Predictive balancing algorithms that anticipate grid frequency events using machine learning

- Remote diagnostics via cloud connectivity (Piller Power Systems’ Q2 2026 announcement)

- Self-calibrating magnetic bearing controllers that compensate for thermal drift and rotor imbalance

2.3 Grid Frequency Regulation as the Anchor Market

The fastest-growing application segment is grid frequency regulation – maintaining 50/60 Hz stability as renewable penetration increases. According to the US Energy Information Administration (EIA), frequency regulation service prices in ISO New England and CAISO markets increased 35% year-over-year in 2025, improving flywheel project economics. Flywheels excel here because they can respond to automatic generation control (AGC) signals within 1–2 cycles, versus 5–10 seconds for batteries.

2.4 Dual-Use Applications: Data Center UPS + Grid Services

An emerging business model, first observed in early 2026, installs flywheel arrays at data centers to serve two revenue streams: (1) providing UPS backup for the data center (primary function) and (2) selling frequency regulation services to the grid during non-emergency periods. This “UPS-as-a-grid-asset” model cuts payback periods from 8-10 years to 3-4 years, driving adoption among colocation providers.

Industry Layering Perspective: Discrete vs. Process Manufacturing Applications

- Discrete applications (e.g., electric bus flash charging, port crane regenerative capture) involve distinct, repeated high-power events. Flywheels are sized per vehicle or per machine, and modularity matters.

- Process applications (e.g., grid frequency regulation, industrial UPS for continuous chemical plants) involve steady-state operation with random disturbances. Flywheels are deployed in multi-unit arrays (5–50 units) with centralized control.

3. Market Segmentation and Competitive Landscape

Segment by Type (QYResearch Classification):

- Mechanical Flywheel Energy Storage Equipment – Uses mechanical bearings (typically ball or roller bearings). Operates at lower speeds (5,000–15,000 rpm) due to bearing friction limits. Lower upfront cost but higher standby losses. Suitable for short-duration (15–30 seconds) UPS applications where standby losses are acceptable.

- Maglev Flywheel Energy Storage Equipment – Uses active magnetic bearings to levitate the rotor, eliminating mechanical contact friction. Operates at higher speeds (20,000–60,000 rpm) with standby losses below 5% per hour. Higher upfront cost but superior efficiency for longer-duration storage (1–15 minutes). Dominates grid frequency regulation and e-mobility applications. Fastest-growing segment.

- Others – Includes superconducting magnetic bearing systems (still developmental) and hybrid flywheel-battery systems.

Segment by Application:

- Industrial – Largest share (~55% in 2025), including UPS for data centers, semiconductor fabs, hospitals, and critical manufacturing. Also includes regenerative energy capture from elevators, cranes, and mining haul trucks.

- Electric Transportation – Fastest-growing segment. Applications include: flash charging for electric buses (pantograph systems), wayside energy storage for rail (capturing braking energy), and marine port cranes. China’s 14th Five-Year Plan includes specific subsidies for flywheel-based transit energy recovery.

- Aerospace – Niche but high-value. Includes: ground power units (GPU) for aircraft starting, power quality for radar installations, and emerging applications in more electric aircraft (MEA) emergency power. Requires MIL-SPEC ruggedization.

Key Market Players (QYResearch-identified):

Qingdao Kingking Applied Chemistry, Piller Power Systems, Powerthru, Temporal Power, Amber Kinetics, Rotor Clipper, and Xinjiang Beiken Energy Engineering. The market is emerging and semi-fragmented. Amber Kinetics and Temporal Power collectively held an estimated 45% of the grid-scale segment in 2025. Piller Power Systems leads in industrial UPS flywheels, particularly in Europe and North America.

4. Exclusive Expert Insights and Recent Developments (Q4 2025 – Q2 2026)

Insight #1 – China’s Accelerating Domestic Production

Xinjiang Beiken Energy Engineering and Qingdao Kingking Applied Chemistry, both Chinese suppliers, have secured provincial government contracts for flywheel frequency regulation in Xinjiang and Shandong grids (announced March 2026). Chinese domestic content policies now require flywheel rotors and magnetic bearings to be locally sourced for state utility projects, accelerating indigenous supply chain development.

Insight #2 – The Regenerative Capture Opportunity in Ports and Mines

According to Temporal Power’s 2025 annual report, flywheel systems deployed at three Australian iron ore ports captured 12–15% of regenerative braking energy from ship loaders and conveyor systems, energy that previously dissipated as heat. A single port installation (April 2026) reported USD 680,000 annual electricity savings with a 2.9-year payback.

Typical User Case (Q1 2026 – US Data Center Operator):

A Northern Virginia colocation provider installed a 5 MW / 15 MJ flywheel array for UPS duty. During a grid voltage sag event lasting 4.5 seconds (January 2026), the flywheels provided seamless backup, avoiding USD 1.2 million in downtime costs. In the following months, the operator enrolled the system in PJM’s frequency regulation market, earning USD 18,000 per month in ancillary service revenue – turning a backup cost center into a profit center.

5. Technical Challenges and Future Development Pathways

Despite strong growth, technical challenges persist:

- Standby losses remain the primary limitation for long-duration storage. Even advanced maglev systems lose 3–5% of stored energy per hour. This makes flywheels uneconomic for applications requiring >30 minutes of storage.

- Rotor containment in catastrophic failure scenarios requires thick steel or composite housings, adding weight and cost. Recent composite containment designs (Powerthru, 2026) have reduced housing weight by 35% but remain expensive.

- Cost per kWh remains high (USD 1,500–3,000/kWh) compared to lithium-ion batteries (USD 300–500/kWh). However, on a cost-per-cycle basis (USD per cycle over lifetime), flywheels are lower for high-cycle applications (>10 cycles/day).

Future Direction: Flywheel energy storage systems will continue to evolve, focusing on higher energy density (via composite rotors and higher-speed magnetic bearings), greater intelligence (AI-driven predictive control and grid synchronization), and integration with batteries (hybrid systems where flywheels handle high-frequency power fluctuations and batteries handle long-duration energy). As electric transportation expands and grids demand faster frequency response, flywheel energy storage equipment will transition from a niche specialty product to a mainstream component of the decarbonized energy ecosystem.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666 (US)

JP: https://www.qyresearch.co.jp