QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Sumatriptan Subcutaneous Injection- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Sumatriptan Subcutaneous Injection market, including market size, share, demand, industry development status, and forecasts for the next few years.

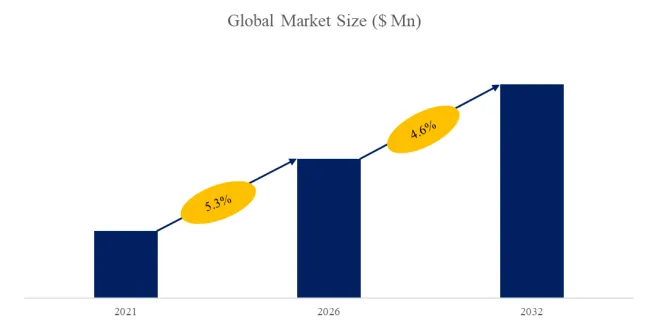

The global market for Sumatriptan Subcutaneous Injection was estimated to be worth US$ 176 million in 2025 and is projected to reach US$ 241 million, growing at a CAGR of 4.6% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6259137/sumatriptan-subcutaneous-injection

Sumatriptan Subcutaneous Injection Market Summary

Sumatriptan Subcutaneous Injection is an injectable formulation of a triptan-class 5-HT1B/1D receptor agonist, primarily used for the rapid relief of acute migraine attacks in adults and, in selected cases, cluster headache. Compared with oral and intranasal formulations, the subcutaneous route offers faster onset, quicker peak plasma exposure, and more direct symptom control, making it particularly suitable for patients requiring rapid intervention or those with nausea, vomiting, or poor tolerance for oral administration. The mainstream commercial presentations are 6 mg/0.5 mL prefilled syringes and auto-injector devices, both of which support use in hospital and outpatient self-administration settings.

From a value-chain perspective, sumatriptan subcutaneous injection is a mature specialty pharmaceutical product combining sterile injectable formulation with drug-delivery device integration. Upstream materials mainly include sumatriptan succinate API, sterile water for injection, buffer systems such as acetate or phosphate buffers, stabilizers, and device-related components including glass barrels, rubber stoppers, needle assemblies, and auto-injector parts. Although the pharmacology and clinical pathway are well established, manufacturing still depends on high-standard aseptic compounding, sterile filtration, filling, and either terminal sterilization or fully aseptic processing, requiring strict cleanroom control and robust GMP systems.

In midstream production, manufacturers must ensure formulation stability, content uniformity, and impurity control, while also addressing device usability, dosing accuracy, and product reliability. For prefilled syringes and auto-injectors, integrated control of both drug and device quality is especially important, which preserves a meaningful technical barrier even in a genericized market. In regulated markets, manufacturers also need to meet stringent requirements for sterile injectable registration, device consistency, and usability validation.

Downstream customers include global and regional generic pharmaceutical companies, hospital emergency departments, neurology clinics, headache specialty practices, and retail pharmacy channels. Hospital use is centered on rapid symptom control, while outpatient and retail channels place greater emphasis on self-administration convenience, device usability, and brand familiarity. Although it is not the largest-volume product in headache treatment, sumatriptan subcutaneous injection maintains a clear clinical role in the acute-relief segment.

Looking ahead, the market for sumatriptan subcutaneous injection is expected to remain relatively mature, with future growth driven mainly by rising self-management demand, broader adoption of auto-injector formats, and improved specialty care access in emerging markets. At the same time, competition is gradually shifting from simple price competition toward a more comprehensive focus on formulation stability, ease of administration, device reliability, and channel coverage. For manufacturers, long-term competitiveness will depend on maintaining stable registration and supply in mature markets while expanding product accessibility in growth regions.

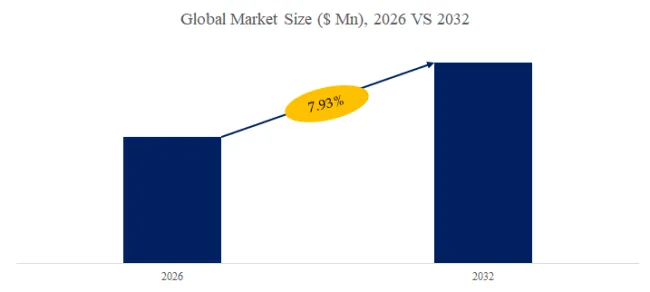

According to the new market research report “Global Sumatriptan Subcutaneous Injection Market Report 2026-2032”, published by QYResearch, the global Sumatriptan Subcutaneous Injection market size is projected to reach USD 0.24 billion by 2032, at a CAGR of 4.62% during the forecast period.

Figure00002. Global Sumatriptan Subcutaneous Injection Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global Sumatriptan Subcutaneous Injection Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

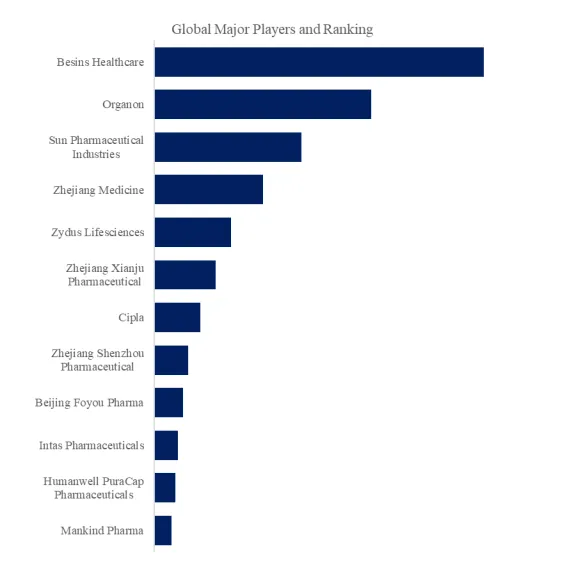

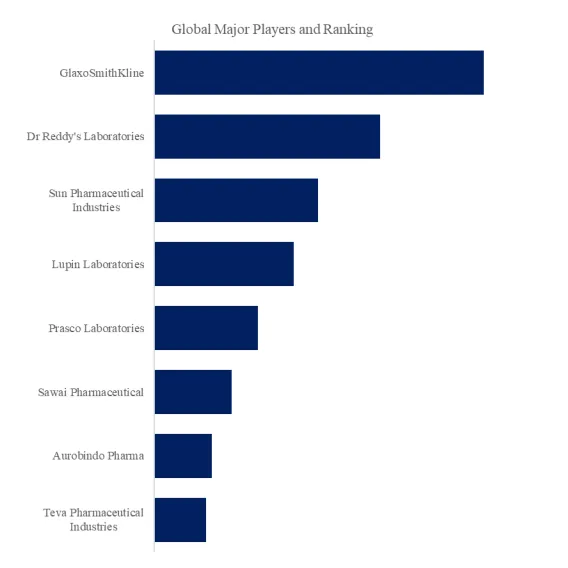

Figure00003. Global Sumatriptan Subcutaneous Injection Top 8 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Sumatriptan Subcutaneous Injection Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

According to QYResearch Top Players Research Center, the global key manufacturers of Sumatriptan Subcutaneous Injection include GlaxoSmithKline, Dr Reddy’s Laboratories, etc. In 2025, the global top three players had a share approximately 58.23% in terms of revenue.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Sumatriptan Subcutaneous Injection market is segmented as below:

By Company

GlaxoSmithKline

Dr Reddy’s Laboratories

Sun Pharmaceutical Industries

Lupin Laboratories

Prasco Laboratories

Sawai Pharmaceutical

Aurobindo Pharma

Teva Pharmaceutical Industries

Segment by Type

Prefilled Syringe

Auto-injector Device

Others

Segment by Application

Hospital

Clinic

Others

Each chapter of the report provides detailed information for readers to further understand the Sumatriptan Subcutaneous Injection market:

Chapter 1: Introduces the report scope of the Sumatriptan Subcutaneous Injection report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Sumatriptan Subcutaneous Injection manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Sumatriptan Subcutaneous Injection market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Sumatriptan Subcutaneous Injection in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Sumatriptan Subcutaneous Injection in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Sumatriptan Subcutaneous Injection competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Sumatriptan Subcutaneous Injection comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Sumatriptan Subcutaneous Injection market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Sumatriptan Subcutaneous Injection Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Sumatriptan Subcutaneous Injection Market Research Report 2026

Global Sumatriptan Subcutaneous Injection Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp