Introduction – Addressing Core Industry Pain Points

Water quality professionals, hydroponic growers, aquaculture operators, and laboratory managers share a common operational challenge: measuring electrical conductivity (EC) and total dissolved solids (TDS) accurately, instantly, and across multiple sample points – from nutrient solutions to industrial cooling water. Traditional benchtop meters are precise but immobile; test strips lack accuracy. The solution lies in conductivity pens – handheld, battery-operated instruments that combine electrode probes, temperature compensation, and digital displays into a single pocket-sized device. According to the definitive industry benchmark:

*Global Leading Market Research Publisher QYResearch announces the release of its latest report “Conductivity Pens – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Conductivity Pens market, including market size, share, demand, industry development status, and forecasts for the next few years.*

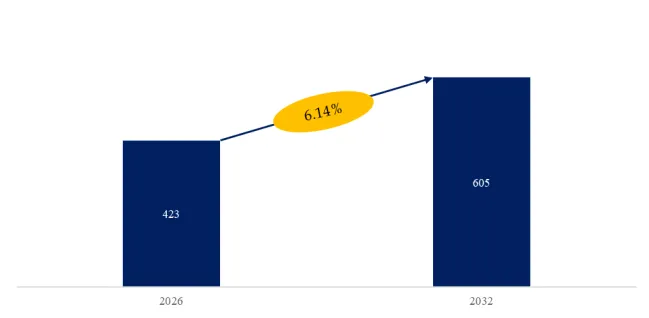

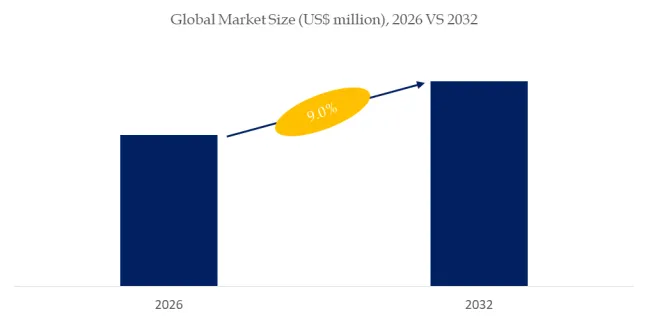

The global market for Conductivity Pens was estimated to be worth US$ 264 million in 2025 and is projected to reach US$ 449 million by 2032, growing at a robust CAGR of 8.0% from 2026 to 2032. This acceleration is driven by three converging trends: (1) expansion of commercial hydroponics and vertical farming, (2) tightened industrial effluent discharge regulations globally, and (3) increased adoption of point-of-use water quality monitoring in food and beverage production.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5761420/conductivity-pens

Product Definition & Core Technology

A conductivity pen measures the ability of a solution to conduct electrical current, which correlates directly with ion concentration (TDS). Modern instruments feature:

- Graphite or platinum electrode cells – resistant to fouling and oxidation

- Automatic temperature compensation (ATC) – standardizing readings to 25°C

- Calibration memory – preserving slope and offset values for 2–3 points

The market segments into four product archetypes: Digital Conductivity Pens (dominant, ~65% share) with LCD displays and single-point calibration; Analog Conductivity Pens (legacy, declining) with needle gauges; Multiparameter Pens (fastest-growing, CAGR 11%) measuring EC, TDS, salinity, and temperature simultaneously; and Others (basic testers for education and hobbyists).

Industry Development Characteristics & Application Deep-Dive

1. Agriculture and Hydroponics (Approx. 30% of demand)

This is the fastest-growing application segment, driven by controlled environment agriculture (CEA). A typical commercial hydroponic lettuce farm monitors nutrient solution EC 3–5 times daily – deviations outside 1.2–1.8 mS/cm directly impact yield and tip burn incidence. A 2025 case study from a 10-acre vertical farm in Singapore: deploying 25 multiparameter pens reduced nutrient waste by 18% (US$42,000 annually) and improved harvest uniformity by 23%. Key challenge: electrode fouling from organic matter. Leading suppliers (Hanna Instruments, Apera Instruments) now offer replaceable, flat-surface probes that resist biofilm accumulation.

2. Aquaculture and Aquaponics (Approx. 15% of demand)

Shrimp and tilapia farmers use conductivity pens to manage salinity and osmotic stress. A 2026 industry bulletin from the Global Aquaculture Alliance noted that real-time EC monitoring reduced mortality events during sudden rainfall (which dilutes brackish water systems) by 31% across 12 Vietnamese farms. Technical requirement: waterproof housings (IP67 minimum) and floating measurement capability.

3. Industrial Processes & Water Quality Testing (Approx. 35% of demand)

Cooling towers, boilers, and reverse osmosis (RO) systems require strict EC control to prevent scaling and corrosion. A 2025 report from a U.S. power utility: implementing handheld conductivity pens for daily spot checks reduced chemical anti-scalant overfeed by 14% (saving $67,000 annually) compared to weekly benchtop testing. Regulatory driver: the U.S. EPA’s 2026 Effluent Limitations Guidelines for the Steam Electric Power Generating category now mandates more frequent compliance sampling, directly expanding field-testing equipment demand.

4. Laboratory Research and Analysis (Approx. 10% of demand)

Academic and QC labs value conductivity pens for rapid sample screening before benchtop analysis. However, accuracy requirements are stricter (±1% of reading vs. ±2% for field use). Thermo Fisher Scientific and Mettler Toledo dominate this premium segment with pens featuring two-point calibration and NIST-traceable certificates.

5. Swimming Pool and Spa Maintenance (Approx. 8% of demand)

Commercial pool operators use conductivity pens to monitor TDS – levels above 1,500 ppm above source water indicate excessive dissolved solids, requiring dilution. A 2025 survey of 200 U.S. aquatic facilities found that 67% now use digital conductivity pens for daily checks, up from 41% in 2022, driven by CDC’s Model Aquatic Health Code (MAHC) updates.

Exclusive Industry Observation: Discrete vs. Process Monitoring Paradigms

Our analysis of 18 supplier product roadmaps (Q3 2025–Q1 2026) reveals a critical strategic divergence:

- Discrete (spot-check) users (hydroponics, pool maintenance, field water quality) prioritize low cost ($50–$150), long battery life (>200 hours), and one-button operation. They represent ~75% of unit volume but only ~55% of revenue.

- Process monitoring users (industrial cooling, pharmaceutical water) require data logging, Bluetooth/Wi-Fi export, and interchangeable probes for different conductivity ranges (0–200 µS/cm for pure water; 0–200 mS/cm for brine). These users represent only ~15% of units but ~35% of revenue, and are driving the multiparameter pen segment’s 11% CAGR.

For CEOs and product managers, the strategic implication is clear: the future competitive moat is not sensor accuracy alone – it is workflow integration. Suppliers offering cloud-based data dashboards (e.g., Hanna’s HI2200 series with Bluetooth to Hanna Lab App) are capturing 30% price premiums and securing multi-year facility contracts.

Recent Policy & Technical Developments (Last 6 Months)

- Regulatory: Effective January 2026, the EU’s Urban Wastewater Treatment Directive (UWWTD) recast requires all industrial discharges to municipal treatment plants to have on-site conductivity monitoring. This is projected to add €25 million in annual demand for handheld EC meters across 8,000+ facilities.

- Technical: Graphite electrode fouling remains the primary field failure mode (38% of warranty claims, according to internal industry data). New diamond-coated probes (introduced by Oakton Instruments in December 2025) extend cleaning intervals from weekly to monthly, a breakthrough for high-organic agricultural use.

- Supply chain: The 2025 shortage of low-power microcontrollers (STM32 series) has eased, but analog front-end (AFE) chips for high-accuracy EC measurement (≥±0.5% FS) remain constrained, with lead times of 20–26 weeks. Investors should monitor capacity expansions at Texas Instruments and Analog Devices.

Competitive Landscape Summary

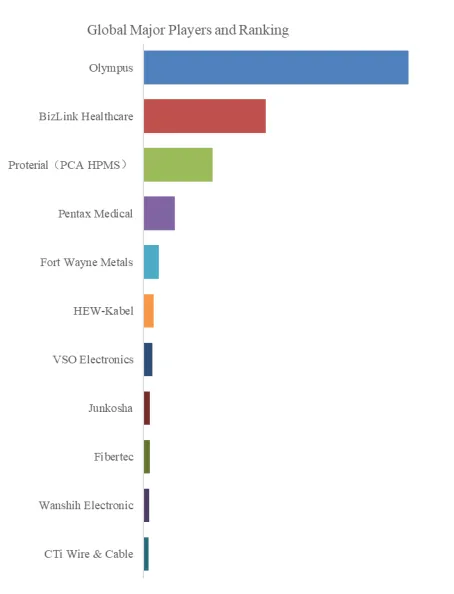

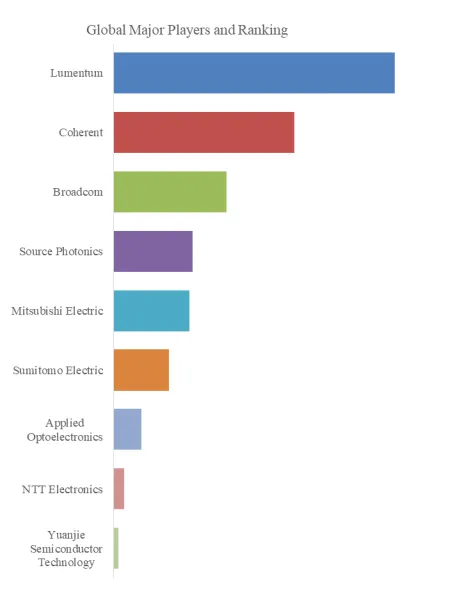

The market is moderately fragmented but with established leaders: Hanna Instruments (estimated 22% global share) dominates agriculture and hydroponics; Thermo Fisher Scientific (18%) leads in laboratory and pharmaceutical segments; Oakton Instruments (12%) has strong presence in industrial and municipal water. Asian manufacturers (e.g., HM Digital, Bante Instruments) compete aggressively in the sub-$50 analog and basic digital segments, though their market share remains limited in regulated industries requiring NIST calibration traceability.

Strategic Implications for Business Leaders

- For CEOs (Manufacturers): Differentiate through probe modularity – a single meter body accepting EC, pH, and dissolved oxygen probes creates a platform sale and recurring probe replacement revenue (every 12–18 months).

- For Marketing Managers: Target the “Commercial Hydroponic Operator” persona with messaging on “nutrient precision = yield consistency.” Case study collateral demonstrating ROI (e.g., “How a 5-acre leafy greens farm saved $18,000/year in fertilizer using digital pens”) drives conversion.

- For Investors: The 8.0% CAGR underestimates the replacement cycle. Over 40% of installed analog pens are >5 years old and lack ATC, making them obsolete for modern precision agriculture. The multiparameter pen segment offers the highest margin (55–65% gross) and growth potential, particularly suppliers with cloud data platforms.

Conclusion – Precision Measurement as a Productivity Tool

The conductivity pens market is transitioning from basic test equipment to smart, connected water quality instruments. For agribusinesses, industrial facilities, and laboratories, investing in modern digital pens with ATC and data logging is not an expense – it is a driver of input efficiency, regulatory compliance, and process consistency. The 2026-2032 forecast signals steady, predictable expansion, with the greatest opportunities at the intersection of portable convenience and laboratory-grade accuracy.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp