QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Industrial Robot Conveyor Belt Tracking Solutions- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Industrial Robot Conveyor Belt Tracking Solutions market, including market size, share, demand, industry development status, and forecasts for the next few years.

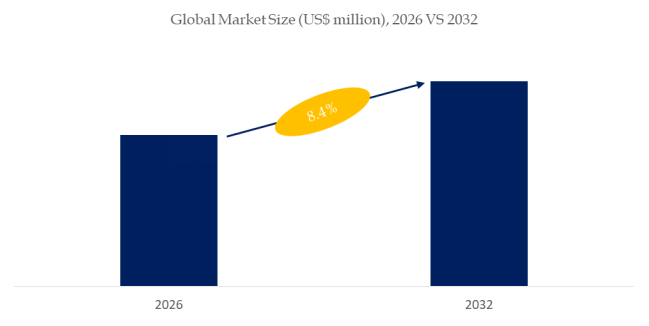

The global market for Industrial Robot Conveyor Belt Tracking Solutions was estimated to be worth US$ 1201 million in 2025 and is projected to reach US$ 2041 million, growing at a CAGR of 8.4% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5786318/industrial-robot-conveyor-belt-tracking-solutions

Industrial Robot Conveyor Belt Tracking Solutions Market Summary

According to the new market research report “Global Industrial Robot Conveyor Belt Tracking Solutions Market Report 2026-2032”, published by QYResearch, the global Industrial Robot Conveyor Belt Tracking Solutions market size is projected to reach USD 2.04 billion by 2032, at a CAGR of 8.4% during the forecast period.

Figure00001. Global Industrial Robot Conveyor Belt Tracking Solutions Market Size (US$ million), 2026 VS 2032

Above data is based on report from QYResearch: Global Industrial Robot Conveyor Belt Tracking Solutions Market Report 2021-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

The industrial robot conveyor belt tracking solutions market is growing rapidly as manufacturers seek to synchronize robotic operations with continuously moving production lines. These solutions enable robots to dynamically track, pick, place, assemble, or inspect products on conveyors without stopping line motion, significantly improving throughput and equipment utilization. Demand is closely tied to the expansion of automated production in food processing, logistics, packaging, electronics, automotive, and general manufacturing. Compared with traditional fixed-position automation, conveyor tracking solutions reduce cycle time, floor space requirements, and mechanical complexity. Advances in vision systems, real-time controllers, and motion algorithms have lowered deployment barriers and improved accuracy. As factories pursue higher efficiency and lower unit costs, conveyor belt tracking is evolving from a niche capability into a standard automation module.

Asia-Pacific is the largest and fastest-growing regional market, driven by large-scale manufacturing capacity in China, Japan, South Korea, and Southeast Asia. High adoption rates in electronics assembly, battery manufacturing, and fast-moving consumer goods production underpin strong regional demand. Europe represents a technologically mature market, with emphasis on precision, reliability, and integration into Industry 4.0 architectures. Germany, Italy, and Northern Europe lead adoption in automotive, packaging, and intra logistics applications. North America shows stable growth, supported by food processing automation, logistics sorting systems, and reshoring-driven factory upgrades. Emerging markets are gradually adopting conveyor tracking as costs decline and integrator capabilities improve.

Major opportunities lie in high-speed sorting, flexible packaging, and mixed-product production lines where traditional automation struggles with variability. The growth of e-commerce and warehouse automation creates new demand for robotic conveyor tracking in parcel handling and distribution centers. Integration with AI vision and 3D sensing further expands application scope to randomly oriented and overlapping items. However, risks include system complexity and sensitivity to conveyor vibration, lighting changes, and product variability. Integration and commissioning costs can be a barrier for small and mid-sized factories. In addition, dependence on high-quality vision hardware and software increases exposure to supply chain and cost fluctuations.

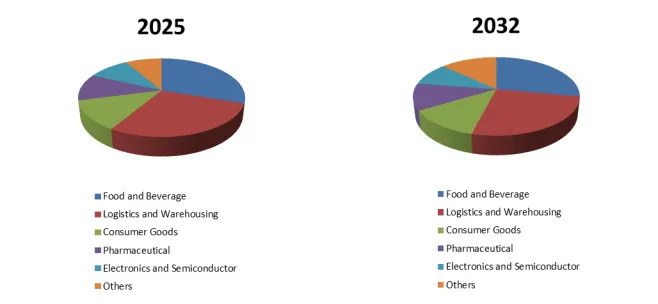

Figure00002. Industrial Robot Conveyor Belt Tracking Solutions, Global Market Size, Split by Application Segment

Based on or includes research from QYResearch: Global Industrial Robot Conveyor Belt Tracking Solutions Market Report 2021-2032.

In terms of product application, currently Food and Beverage is the largest segment, hold a share of 30%.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Industrial Robot Conveyor Belt Tracking Solutions market is segmented as below:

By Company

Epson

DENSO WAVE INCORPORATED

ABB

NexCOBOT

ROKAE

TIANJIZN

FAIR INNOVATION (SUZHOU) ROBOT SYSTEM

KUKA

Martin

Segment by Type

Vision-Guided Tracking

Encoder-Based Tracking

Laser Sensor Tracking

Hybrid Multi-Sensor Tracking

Segment by Application

Food and Beverage

Logistics and Warehousing

Consumer Goods

Pharmaceutical

Electronics and Semiconductor

Others

Each chapter of the report provides detailed information for readers to further understand the Industrial Robot Conveyor Belt Tracking Solutions market:

Chapter 1: Introduces the report scope of the Industrial Robot Conveyor Belt Tracking Solutions report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Industrial Robot Conveyor Belt Tracking Solutions manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Industrial Robot Conveyor Belt Tracking Solutions market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Industrial Robot Conveyor Belt Tracking Solutions in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Industrial Robot Conveyor Belt Tracking Solutions in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Industrial Robot Conveyor Belt Tracking Solutions competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Industrial Robot Conveyor Belt Tracking Solutions comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Industrial Robot Conveyor Belt Tracking Solutions market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Industrial Robot Conveyor Belt Tracking Solutions Market Research Report 2026

Global Industrial Robot Conveyor Belt Tracking Solutions Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Industrial Robot Conveyor Belt Tracking Solutions Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp