QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Electric Vehicle- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Electric Vehicle market, including market size, share, demand, industry development status, and forecasts for the next few years.

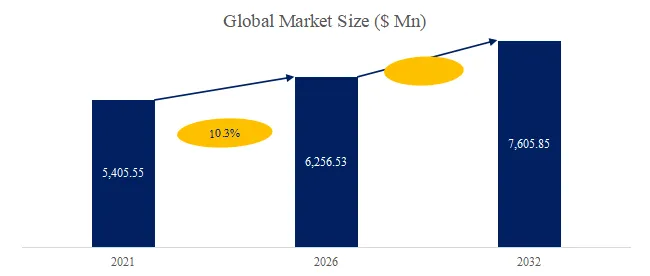

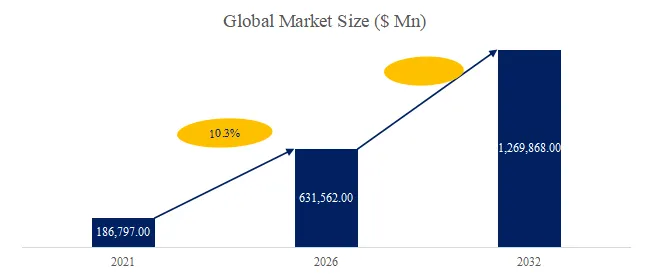

The global Electric Vehicle market was valued at US$ 513,246 million in 2025 and is expected to reach US$ 1,269,868 million by 2032, growing at a CAGR of 12.35% during 2026–2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5498985/electric-vehicle

Electric Vehicle

Electric Vehicle (EV) refers to a class of automobiles that use electric motors as the primary source of propulsion, with energy supplied by onboard electrical storage systems such as lithium-ion batteries or, in some cases, fuel cells. Compared with internal combustion engine vehicles, EVs feature higher energy conversion efficiency, instant torque output, lower operating noise, and zero tailpipe emissions, making them a key pathway toward decarbonization of the transportation sector. Modern electric vehicles integrate advanced battery management systems, power electronics, regenerative braking, and increasingly software-defined architectures, enabling improvements in driving range, safety, connectivity, and intelligent functions. As charging infrastructure expands and battery technology continues to advance, electric vehicles are becoming a core component of future mobility systems worldwide.

According to the new market research report ” Electric Vehicle- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032 “, published by QYResearch, the global Electric Vehicle market size is projected to grow from USD 631562 million in 2026 to USD 1269868 million by 2032, at a CAGR of 12.35% during the forecast period.

Figure00002. Global Electric Vehicle Market Insights, Forecast to 2032

Above data is based on report from QYResearch: Electric Vehicle – Global Market Share and Ranking, Overall Sales and Demand Forecast 2025-2031

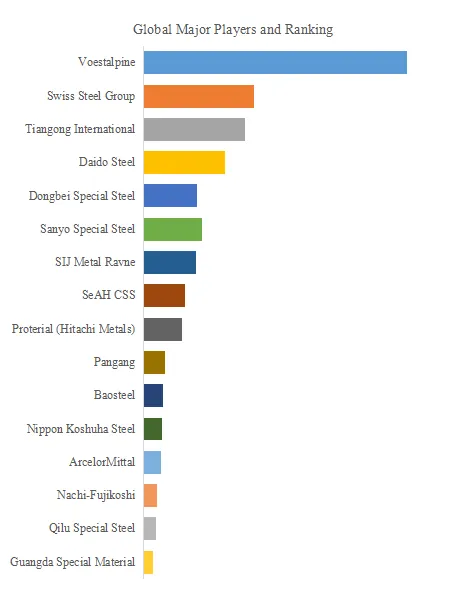

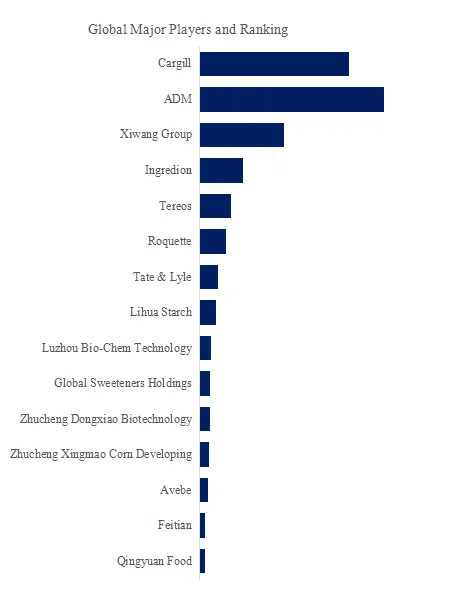

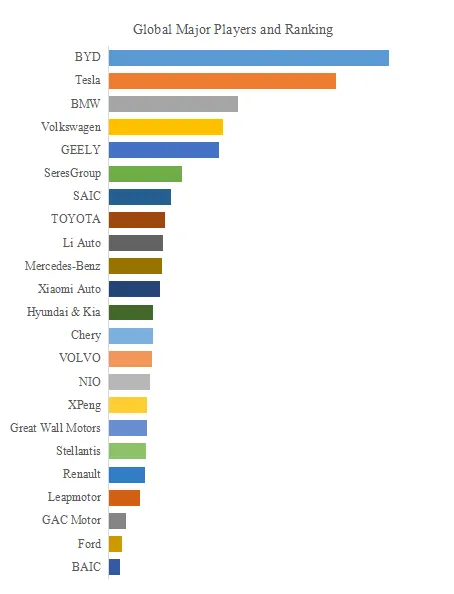

Figure00003. Global Electric Vehicle Top 23 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Electric Vehicle – Global Market Share and Ranking, Overall Sales and Demand Forecast 2025-2031

This report profiles key players of Electric Vehicle such as BYD, Tesla, BMW, Volkswagen, Li Auto, Seres Group, Geely, Mercedes-Benz, Volvo, SAIC, Hyundai & Kia, Stellantis, Great Wall Motors, Renault, Chery, NIO, Toyota, GAC Motor, XPeng, Leapmotor, Xiaomi Auto, Ford, BAIC.

In 2025, the global top five Electric Vehicle players account for 47% of market share in terms of revenue. Above figure shows the key players ranked by revenue in Electric Vehicle.

|

Company Name |

Description |

|

Tesla |

Tesla is a U.S.-based electric vehicle and clean energy company, best known for accelerating the global adoption of battery electric vehicles. Its core strengths lie in vehicle platforms, electric drivetrains, battery technology, software-defined vehicles, and over-the-air updates, supported by a direct-sales model. Through high vertical integration and a global manufacturing footprint, Tesla continues to reduce unit costs and maintains strong influence across the global new energy vehicle value chain. |

|

BMW |

BMW Group is a Germany-based premium automotive manufacturer with brands including BMW, MINI, and Rolls-Royce, traditionally recognized for luxury vehicles, performance engineering, and strong brand equity. In recent years, BMW has accelerated its electrification and digital transformation while maintaining strengths in internal combustion and hybrid platforms, expanding its pure electric lineup and next-generation E/E architectures, supported by a global manufacturing and premium supply-chain network. |

|

BYD |

BYD is a China-based new energy vehicle and battery technology company with operations spanning passenger vehicles, commercial vehicles, batteries, electric powertrains, and energy storage. As one of the few automakers with deep vertical integration across batteries, motors, electronics, and vehicle manufacturing, BYD leverages proprietary technologies such as Blade Battery and large-scale production to maintain leadership in China’s NEV market while expanding its global footprint. |

|

Geely |

Geely is one of China’s leading automotive groups, operating a diversified portfolio of domestic and international brands across multiple powertrain technologies. Through acquisitions and strategic investments, Geely has built a broad product matrix covering internal combustion, hybrid, and pure electric vehicles, while strengthening capabilities in modular platforms, electrification, and intelligent cockpit technologies to enhance its competitiveness in mid-to-high-end and global markets. |

Market Drivers:

Tightening carbon-reduction targets, emissions regulations, and fuel-economy standards are accelerating OEM electrification strategies and steering end-market demand toward electric vehicles. Continuous improvements in battery energy density, manufacturing processes, and production scale are reshaping vehicle cost structures while enhancing driving range, charging performance, and overall vehicle capability. Expanding charging networks, greater penetration of digital and software-defined features, and fleet purchasing decisions based on lifecycle cost considerations are collectively strengthening EV adoption across both passenger and commercial segments.

Restraint:

Uneven development of charging infrastructure across regions affects charging convenience, with variations in network density, reliability, and high-power availability influencing user experience. Battery cost management faces challenges from raw-material price volatility, geopolitical supply risks, and still-maturing recycling ecosystems. In parallel, differing consumer expectations regarding driving range, cold-weather performance, maintenance costs, and resale values—together with evolving subsidy schemes and electricity pricing—continue to moderate the pace of market penetration.

Opportunity:

On the product side, advances in batteries, thermal management, 800V high-voltage architectures, and vehicle E/E platforms open room for performance gains and cost reductions, enabling EVs to penetrate broader price segments. From a business perspective, deeper integration between vehicles and energy systems is expanding use cases through charging services, energy management, and vehicle-to-grid interactions, shifting value creation from one-time vehicle sales toward recurring services. At the same time, accelerating electrification in light commercial vehicles, logistics, shared mobility, and selected emerging markets creates new growth avenues for companies with scalable manufacturing, cost discipline, and localized operational capabilities.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Electric Vehicle market is segmented as below:

By Company

BYD

Tesla

BMW

Volkswagen

Li Auto

SeresGroup

GEELY

Mercedes-Benz

VOLVO

SAIC

Hyundai & Kia

Stellantis

Great Wall Motors

Renault

Chery

NIO

TOYOTA

GAC Motor

XPeng

Leapmotor

Xiaomi Auto

Ford

BAIC

Segment by Type

PHEV

BEV

Segment by Application

Home Use

Commercial Use

by Region

North America

United States

Canada

Asia Pacific

China

Japan

South Korea

India

Rest of Asia Pacific

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Latin America

Mexico

Brazil

Rest of Latin America

Middle East & Africa

Turkey

Rest of MEA

Each chapter of the report provides detailed information for readers to further understand the Electric Vehicle market:

Chapter 1: Introduces the report scope of the Electric Vehicle report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Electric Vehicle manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Electric Vehicle market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Electric Vehicle in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Electric Vehicle in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Electric Vehicle competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Electric Vehicle comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Electric Vehicle market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Electric Vehicle Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Electric Vehicle Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Electric Vehicle Market Research Report 2026

Global AI Electric Vehicles Market Outlook, In‑Depth Analysis & Forecast to 2032

Global AI Electric Vehicles Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Electric Vehicle MRO – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

Global Electric Vehicle MRO Market Research Report 2026

AI Electric Vehicles- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

Global AI Electric Vehicles Market Research Report 2026

Electric Vehicle ADAS – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

Global Electric Vehicle ADAS Market Research Report 2026

800V Electric Vehicle- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

Global 800V Electric Vehicle Market Research Report 2026

Mini Electric Vehicle- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

Electric Vehicle PMIC- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

Global Mini Electric Vehicle Market Research Report 2026

Global Electric Vehicle PMIC Market Research Report 2026

Global Electric Vehicle Glass Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Electric Vehicle Glass Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Electric Vehicle Crane Market Outlook, In‑Depth Analysis & Forecast to 2032

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp