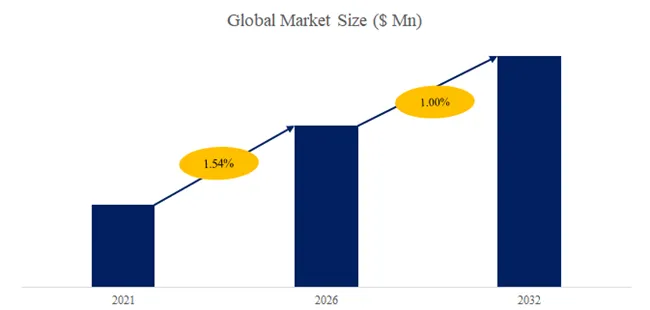

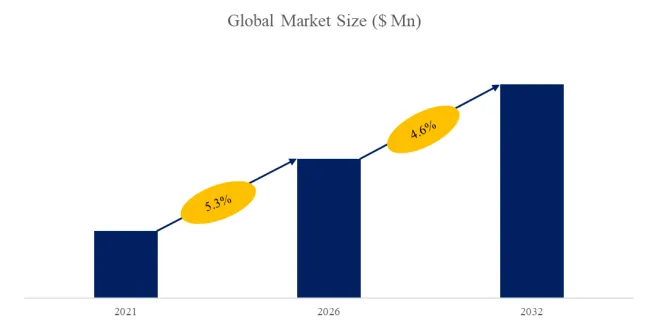

The global market for 2 Way Ball Valve was estimated to be worth US$ million in 2025 and is projected to reach US$ million, growing at a CAGR of %from 2026 to 2032.

QYResearch announces the release of 2026 latest report “2 Way Ball Valve – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global 2 Way Ball Valve market, including market size, share, demand, industry development status, and forecasts for the next few years.

This report will help you generate, evaluate and implement strategic decisions as it provides the necessary information on technology-strategy mapping and emerging trends. The report’s analysis of the restraints in the market is crucial for strategic planning as it helps stakeholders understand the challenges that could hinder growth. This information will enable stakeholders to devise effective strategies to overcome these challenges and capitalize on the opportunities presented by the growing market. Furthermore, the report incorporates the opinions of market experts to provide valuable insights into the market’s dynamics. This information will help stakeholders gain a better understanding of the market and make informed decisions.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5764325/2-way-ball-valve

This 2 Way Ball Valve Market Research/Analysis Report includes the following points:

How much is the global 2 Way Ball Valvemarket worth? What was the value of the market In 2026?

Would the market witness an increase or decline in the demand in the coming years?

What is the estimated demand for different typesand upcoming industry applications of products in 2 Way Ball Valve?

What are Projections of Global 2 Way Ball ValveIndustry Considering Capacity, Production and Production Value? What Will Be the Estimation of Cost and Profit?

What Will Be Market Share, Supply,Consumption and Import and Export of 2 Way Ball Valve?

What Should Be Entry Strategies, Countermeasures to Economic Impact, and Marketing Channels for 2 Way Ball Valve Industry?

Where will the strategic developments take the industry in the mid to long-term?

What are the factors contributing to the final price of 2 Way Ball Valve? What are the raw materials used for 2 Way Ball Valve manufacturing?

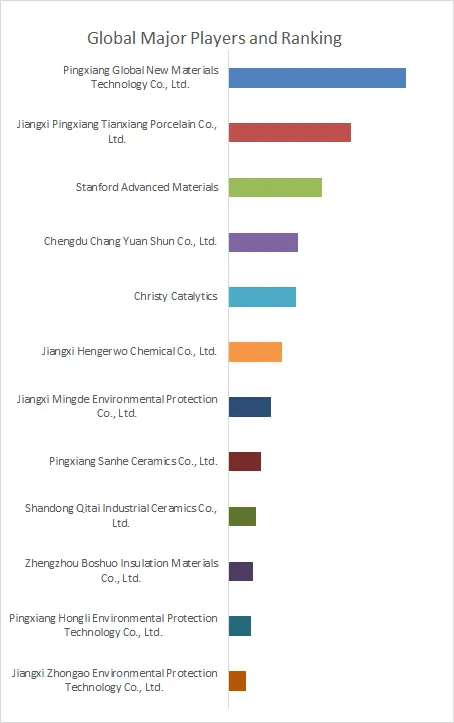

Who are the major Manufacturersin the 2 Way Ball Valve market? Which companies are the front runners?

Which are the recent industry trends that can be implemented to generate additional revenue streams?

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The 2 Way Ball Valve market is segmented as below:

By Company

Gemini Valve

IMI Critical Engineering

4G GHIDINI

International Polymer Solutions Inc.

Simtech USA

A-T Controls, Inc.

Jordan Valve

Tylok International, Inc.

AS-Schneider

Aimco Term

Conval

Velan

Segment by Type

Brass

PVC

Stainless Steel

Segment by Application

Oil and Gas

Energy Power

Chemical Industry

Water Treatment

Others

This information will help stakeholders make informed decisions and develop effective strategies for growth. The report’s analysis of the restraints in the market is crucial for strategic planning as it helps stakeholders understand the challenges that could hinder growth. This information will enable stakeholders to devise effective strategies to overcome these challenges and capitalize on the opportunities presented by the growing market. Furthermore, the report incorporates the opinions of market experts to provide valuable insights into the market’s dynamics. This information will help stakeholders gain a better understanding of the market and make informed decisions.

Each chapter of the report provides detailed information for readers to further understand the 2 Way Ball Valve market:

Chapter One: Introduces the study scope of this report, executive summary of market segment by type, market size segments for North America, Europe, Asia Pacific, Latin America, Middle East & Africa.

Chapter Two: Detailed analysis of 2 Way Ball Valve manufacturers competitive landscape, price, sales, revenue, market share and ranking, latest development plan, merger, and acquisition information, etc.

Chapter Three: Sales, revenue of 2 Way Ball Valve in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the future development prospects, and market space in the world.

Chapter Four: Introduces market segments by application, market size segment for North America, Europe, Asia Pacific, Latin America, Middle East & Africa.

Chapter Five, Six, Seven, Eight and Nine: North America, Europe, Asia Pacific, Latin America, Middle East & Africa, sales and revenue by country.

Chapter Ten: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc.

Chapter Eleven: Analysis of industrial chain, key raw materials, manufacturing cost, and market dynamics. Introduces the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry.

Chapter Twelve: Analysis of sales channel, distributors and customers.

Chapter Thirteen: Research Findings and Conclusion.

Table of Contents

1 2 Way Ball Valve Market Overview

1.1 2 Way Ball Valve Product Overview

1.2 2 Way Ball Valve Market by Type

1.3 Global 2 Way Ball Valve Market Size by Type

1.3.1 Global 2 Way Ball Valve Market Size Overview by Type (2021-2032)

1.3.2 Global 2 Way Ball Valve Historic Market Size Review by Type (2021-2026)

1.3.3 Global 2 Way Ball Valve Forecasted Market Size by Type (2026-2032)

1.4 Key Regions Market Size by Type

1.4.1 North America 2 Way Ball Valve Sales Breakdown by Type (2021-2026)

1.4.2 Europe 2 Way Ball Valve Sales Breakdown by Type (2021-2026)

1.4.3 Asia-Pacific 2 Way Ball Valve Sales Breakdown by Type (2021-2026)

1.4.4 Latin America 2 Way Ball Valve Sales Breakdown by Type (2021-2026)

1.4.5 Middle East and Africa 2 Way Ball Valve Sales Breakdown by Type (2021-2026)

2 2 Way Ball Valve Market Competition by Company

2.1 Global Top Players by 2 Way Ball Valve Sales (2021-2026)

2.2 Global Top Players by 2 Way Ball Valve Revenue (2021-2026)

2.3 Global Top Players by 2 Way Ball Valve Price (2021-2026)

2.4 Global Top Manufacturers 2 Way Ball Valve Manufacturing Base Distribution, Sales Area, Product Type

2.5 2 Way Ball Valve Market Competitive Situation and Trends

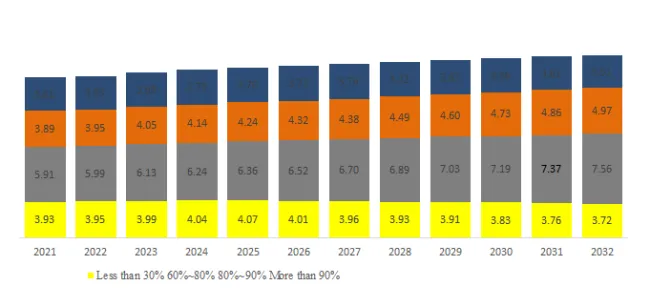

2.5.1 2 Way Ball Valve Market Concentration Rate (2021-2026)

2.5.2 Global 5 and 10 Largest Manufacturers by 2 Way Ball Valve Sales and Revenue in 2024

2.6 Global Top Manufacturers by Company Type (Tier 1, Tier 2, and Tier 3) & (based on the Revenue in 2 Way Ball Valve as of 2024)

2.7 Date of Key Manufacturers Enter into 2 Way Ball Valve Market

2.8 Key Manufacturers 2 Way Ball Valve Product Offered

2.9 Mergers & Acquisitions, Expansion

…

Overall, this report strives to provide you with the insights and information you need to make informed business decisions and stay ahead of the competition.

To contact us and get this report: https://www.qyresearch.com/reports/5764325/2-way-ball-valve

About Us:

QYResearch is not just a data provider, but a creator of strategic value. Leveraging a vast industry database built over 19 years and professional analytical capabilities, we transform raw data into clear trend judgments, competitive landscape analysis, and opportunity/risk assessments. We are committed to being an indispensable, evidence-based cornerstone for our clients in critical phases such as strategic planning, market entry, and investment decision-making.

Contact Us:

If you have any queries regarding this report or if you would like further information, please Contact us:

QY Research Inc. (QYResearch)

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US) 0086-133 1872 9947(CN)

EN: https://www.qyresearch.com

JP: https://www.qyresearch.co.jp