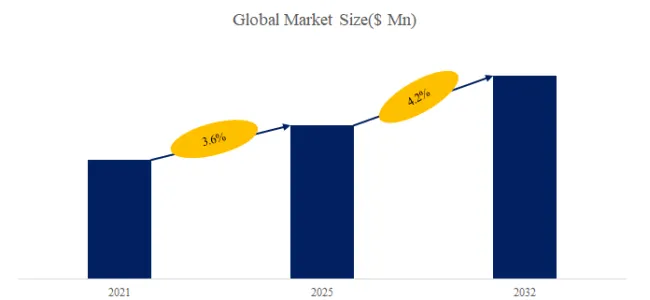

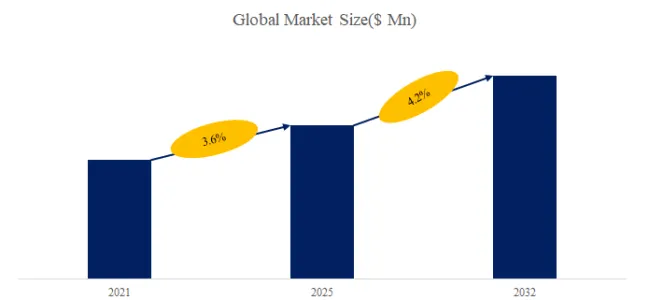

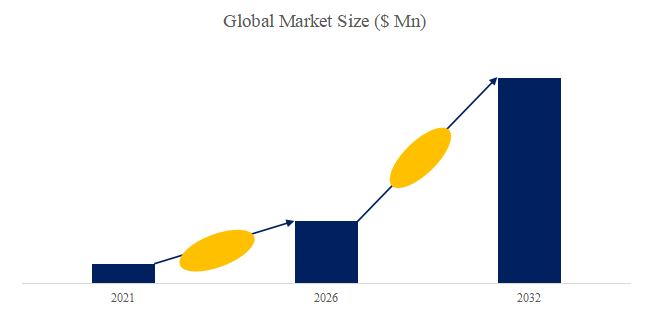

The global market for Mass Detectors was estimated to be worth US$ 4832 million in 2025 and is projected to reach US$ 7225 million, growing at a CAGR of 6.0% from 2026 to 2032.

QY Research (Market Research Report Publisher) announces the release of its lastest report “Mass Detectors – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on historical analysis (2021-2026) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Mass Detectors market, including market size, share, demand, industry development status, and forecasts for the next few years. Provides advanced statistics and information on global market conditions and studies the strategic patterns adopted by renowned players across the globe. It aims to help readers gain a comprehensive understanding of the global Mass Detectors market with multiple angles, which provides sufficient supports to readers’ strategy and decision making. As the market is constantly changing, the report explores competition, supply and demand trends, as well as the key factors that contribute to its changing demands across many markets.

In addition, the market research industry delivers the detailed analysis of the global Mass Detectors market for the estimated forecast period. The market research study delivers deep insights about the different market segments based on the end-use, types and geography. One of the most crucial feature of any report is its geographical segmentation of the market that consists of all the key regions. This section majorly focuses over several developments taking place in the region including substantial development and how are these developments affecting the market. Regional analysis provides a thorough knowledge about the opportunities in business, market status& forecast, possibility of generating revenue, regional market by different end users as well as types and future forecast of upcoming years.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5761353/mass-detectors

Key Benefits for Industry Participants and Stakeholders:

1.In-depth understanding of the Mass Detectorsmarket and its growth prospects

2.Analysis of market drivers, restraints, and opportunities to identify lucrative business avenues

3.Insights into the competitive landscape and strategies of key market players.

4.Knowledge of key trends shaping the Mass Detectors

5.Evaluation of the current economic situationon the industry and potential recovery strategies

6.Future outlook and growth prospects for informed decision-making.

Overall, this report strives to provide you with the insights and information you need to make informed business decisions and stay ahead of the competition.

All findings, data and information provided in the report have been verified and re-verified with the help of reliable sources. The analysts who wrote the report conducted in-depth research using unique and industry-best research and analysis methods.

The Mass Detectors market is segmented as below:

By Company

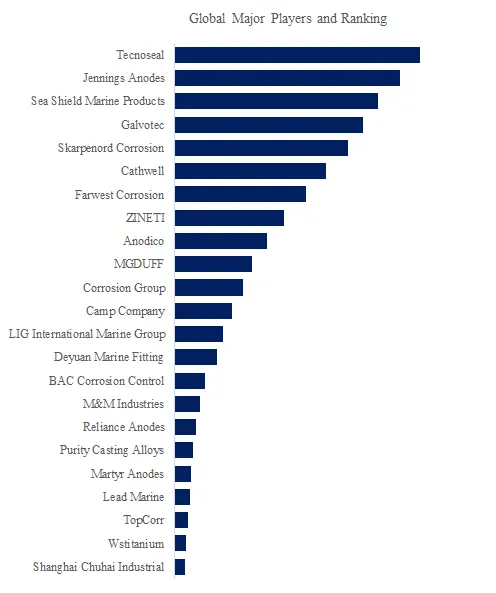

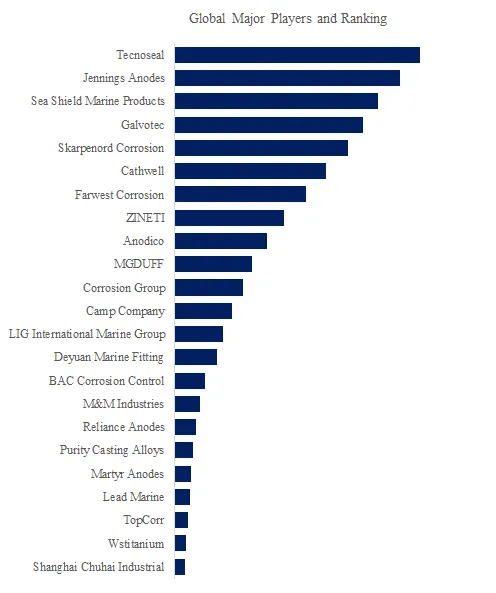

Thermo Fisher Scientific

Agilent Technologies

Waters Corporation

Bruker Corporation

Shimadzu Corporation

PerkinElmer, Inc.

SCIEX

JEOL Ltd.

LECO Corporation

Segment by Type

Quadrupole Mass Detector

Time-of-Flight (TOF) Mass Detector

Ion Trap Mass Detector

Orbitrap Mass Detector

Linear Ion Trap Mass Detector

FT-ICR (Fourier Transform Ion Cyclotron Resonance) Mass Detector

Triple Quadrupole Mass Detector

Hybrid Mass Detectors

Segment by Application

Chemical Analysis

Environmental Monitoring

Pharmaceutical Research

Clinical Diagnostics

Forensic Science

Biotechnology

Others

This information will help stakeholders make informed decisions and develop effective strategies for growth. The report’s analysis of the restraints in the market is crucial for strategic planning as it helps stakeholders understand the challenges that could hinder growth. This information will enable stakeholders to devise effective strategies to overcome these challenges and capitalize on the opportunities presented by the growing market. Furthermore, the report incorporates the opinions of market experts to provide valuable insights into the market’s dynamics. This information will help stakeholders gain a better understanding of the market and make informed decisions.

Each chapter of the report provides detailed information for readers to further understand the Mass Detectors market:

Chapter One: Introduces the study scope of this report, executive summary of market segments by Type, market size segments for North America, Europe, Asia Pacific, Latin America, Middle East & Africa.

Chapter Two: Detailed analysis of Mass Detectors manufacturers competitive landscape, price, sales, revenue, market share and ranking, latest development plan, merger, and acquisition information, etc.

Chapter Three: Sales, revenue of Mass Detectors in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the future development prospects, and market space in the world.

Chapter Four: Introduces market segments by Application, market size segment for North America, Europe, Asia Pacific, Latin America, Middle East & Africa.

Chapter Five, Six, Seven, Eight and Nine: North America, Europe, Asia Pacific, Latin America, Middle East & Africa, sales and revenue by country.

Chapter Ten: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc.

Chapter Eleven: Analysis of industrial chain, key raw materials, manufacturing cost, and market dynamics. Introduces the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry.

Chapter Twelve: Analysis of sales channel, distributors and customers.

Chapter Thirteen: Research Findings and Conclusion.

Table of Contents

1 Mass Detectors Market Overview

1.1Mass Detectors Product Overview

1.2 Mass Detectors Market by Type

1.3 Global Mass Detectors Market Size by Type

1.3.1 Global Mass Detectors Market Size Overview by Type (2021-2032)

1.3.2 Global Mass Detectors Historic Market Size Review by Type (2021-2026)

1.3.3 Global Mass Detectors Forecasted Market Size by Type (2026-2032)

1.4 Key Regions Market Size by Type

1.4.1 North America Mass Detectors Sales Breakdown by Type (2021-2026)

1.4.2 Europe Mass Detectors Sales Breakdown by Type (2021-2026)

1.4.3 Asia-Pacific Mass Detectors Sales Breakdown by Type (2021-2026)

1.4.4 Latin America Mass Detectors Sales Breakdown by Type (2021-2026)

1.4.5 Middle East and Africa Mass Detectors Sales Breakdown by Type (2021-2026)

2 Mass Detectors Market Competition by Company

2.1 Global Top Players by Mass Detectors Sales (2021-2026)

2.2 Global Top Players by Mass Detectors Revenue (2021-2026)

2.3 Global Top Players by Mass Detectors Price (2021-2026)

2.4 Global Top Manufacturers Mass Detectors Manufacturing Base Distribution, Sales Area, Product Type

2.5 Mass Detectors Market Competitive Situation and Trends

2.5.1 Mass Detectors Market Concentration Rate (2021-2026)

2.5.2 Global 5 and 10 Largest Manufacturers by Mass Detectors Sales and Revenue in 2025

2.6 Global Top Manufacturers by Company Type (Tier 1, Tier 2, and Tier 3) & (based on the Revenue in Mass Detectors as of 2025)

2.7 Date of Key Manufacturers Enter into Mass Detectors Market

2.8 Key Manufacturers Mass Detectors Product Offered

2.9 Mergers & Acquisitions, Expansion

…

Our Service:

1.Express Delivery Report Service

2.More than 19 years of vast experience

3.Establish offices in 6 countries

4.Operation for 24 * 7 & 365 days

5.Owns large database

6.In-depth and comprehensive analysis

7.Professional and timely after-sales service

To contact us and get this report: https://www.qyresearch.com/reports/5761353/mass-detectors

About Us:

QYResearch founded in California, USA in 2007. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. Through QYResearch, we will provide a wide range of specialized market research solutions, catering to the unique needs of diverse industries and businesses of all sizes.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp