QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Mechanical Test Equipment- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Mechanical Test Equipment market, including market size, share, demand, industry development status, and forecasts for the next few years.

The global market for Mechanical Test Equipment was estimated to be worth US$ 1984 million in 2025 and is projected to reach US$ 2609 million, growing at a CAGR of 4.0% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5499177/mechanical-test-equipment

Mechanical Test Equipment Market Summary

Mechanical testing equipment is specialized equipment used to verify the performance, safety, and reliability of materials or products. It acquires mechanical, physical, or chemical property data by simulating actual operating conditions (such as vibration, shock, and temperature fluctuations) or applying specific loads (such as tension, compression, and torsion). Its core functions include defect detection, dimensional measurement, fatigue life assessment, and environmental compatibility verification.

Figure00001. Mechanical Test Equipment

Source, Tinius Olsen

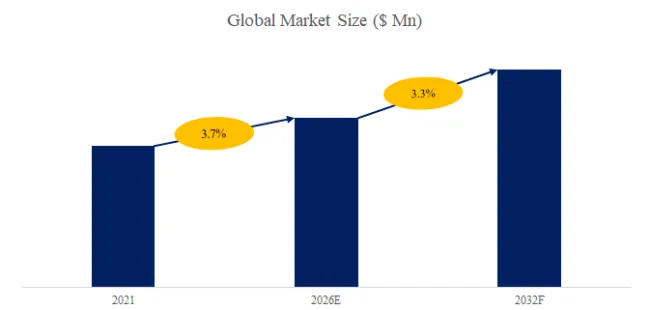

According to the new market research report “Global Mechanical Test Equipment Market Report 2026-2032”, published by QYResearch, the global Mechanical Test Equipment market size is projected to reach USD 2.65 billion by 2032, at a CAGR of 3.3% during the forecast period.

Figure00002. Global Mechanical Test Equipment Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global Mechanical Test Equipment Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

As the quality “gatekeepers” of the entire industrial production process, mechanical testing equipment simulates extreme working conditions, tests material performance, and verifies product reliability, building a closed-loop quality system of “R&D-production-verification” in fields such as aerospace, automotive manufacturing, electronic semiconductors, and building materials. Its industrial chain presents a collaborative architecture of “upstream precision components—midstream integrated manufacturing—downstream application scenarios”: upstream focuses on the R&D of core components such as high-precision sensors, servo motors, and hydraulic components, with companies like Siemens and Honeywell providing industrial-grade control modules; midstream companies such as MTS and China Machinery Testing use system integration technology to assemble components into standardized equipment such as universal testing machines, impact testing machines, and fatigue testing machines; downstream is deeply integrated with scenarios such as lightweight component testing for new energy vehicles, reliability verification of semiconductor packaging, and health monitoring of bridge steel structures, forming a value-added ecosystem of “equipment + services + data.”

Policy empowerment and standard upgrades promote the standardized development of the industry

The National 14th Five-Year Plan for Quality Infrastructure Development clearly lists high-end testing equipment as a key breakthrough area. The State Administration for Market Regulation supports the substitution of domestic equipment through first-of-its-kind insurance compensation and R&D subsidies; EU CE certification and the US ASTM standard system promote the unification of equipment safety and performance specifications. Local governments are implementing supporting policies for industrial upgrading. For example, the Yangtze River Delta region has formed a complete industrial chain innovation cluster, from components to finished products, promoting the joint development of industry standards and cross-regional collaboration.

Development opportunities and challenges exhibit structural characteristics

With the accelerated penetration of intelligent manufacturing, the demand for high-precision, multi-axis linkage testing equipment is surging in fields such as new energy vehicles, commercial aerospace, and high-end equipment. The global market size is expected to exceed 100 billion yuan by 2030. Technological trends are evolving towards intelligence, modularity, and green technologies. For example, AI algorithm-driven real-time data analysis, reconfigurable modular test platforms, and low-energy hydraulic systems are becoming innovative directions. However, significant technological barriers exist: the domestic production rate of high-end sensors is less than 30%, and multi-axis synchronous control algorithms require long-term accumulation; cost pressures limit widespread adoption, and small and medium-sized enterprises have limited equipment procurement budgets; the industry standard system still needs improvement, and unifying cross-domain testing methods is difficult.

The barriers to entry in this industry are multi-dimensional

Technically, it involves interdisciplinary fields such as materials mechanics, control engineering, and computer science, requiring long-term accumulation to master core processes like dynamic load calibration and high/low temperature environment simulation. Financially, a single production line requires an investment exceeding 50 million yuan, and large-scale projects necessitate supporting laboratory construction and certification systems. Market-wise, establishing a certification network covering aerospace, automotive, and electronics sectors, along with building customer trust, makes it difficult for new entrants to achieve effective market penetration in the short term.

Looking to the future, the mechanical testing equipment industry will deepen its development along the path of “high precision, intelligence, and ecological sustainability.” Enterprises need to increase R&D efforts in anti-interference sensors and adaptive control algorithms to overcome cost and performance bottlenecks; achieve real-time sharing of test data and remote operation and maintenance through the Industrial Internet; and build a composite profit model of “equipment sales + testing services + data insights.” Driven by both policy guidance and market demand, mechanical testing equipment is expected to become a key infrastructure supporting the high-end transformation of the manufacturing industry, leading industrial quality assurance towards a more precise and reliable future.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Mechanical Test Equipment market is segmented as below:

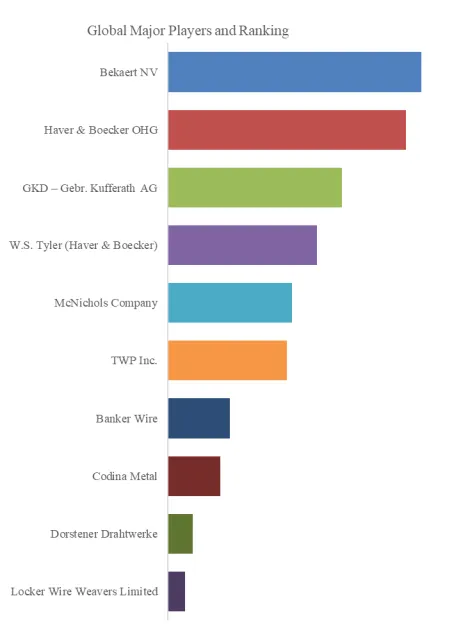

By Company

MTS

ZwickRoell

Instron Corporation

Shimadzu

Ametek STC

SINOTEST

Tinius Olsen

SUNS

Changchun Kexin Test Instrument Co., Ltd

Tianchen Testing Machine

Shanghai Hualong Test Instruments

Buehler

Emerson Apparatus

Applied Test Systems

Hegewald & Peschke

Torontech Group International

Hung Ta Instrument

Jinan Heng Rui Jin Testing Machine Co., Ltd

ADMET

Lishi Instruments

Segment by Type

Universal Testing Machine

Fatigue Testing Machine

Special Testing Machine

Segment by Application

Manufacturing

Civil Engineering

Pharmaceutical Industry

Scientific Institutions

Others

Each chapter of the report provides detailed information for readers to further understand the Mechanical Test Equipment market:

Chapter 1: Introduces the report scope of the Mechanical Test Equipment report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Mechanical Test Equipment manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Mechanical Test Equipment market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Mechanical Test Equipment in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Mechanical Test Equipment in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Mechanical Test Equipment competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Mechanical Test Equipment comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Mechanical Test Equipment market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Mechanical Test Equipment Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Mechanical Test Equipment Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Mechanical Test Equipment Market Research Report 2026

Global Mechanical Test Equipment Market Research Report 2025

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp