Opening Paragraph (User Pain Point & Solution Orientation):

For quality assurance directors and ESD (electrostatic discharge) control engineers in electronics, semiconductor, and medical device manufacturing, a single undetected static charge can destroy micron-thin circuit traces, contaminate sterile cleanrooms, or ignite flammable dust. Traditional go/no-go surface resistivity tests fail to capture how quickly a material actually dissipates a charge—the critical parameter for real-world ESD safety. The Static Decay Meter directly addresses this blind spot by applying a controlled electrostatic voltage (typically ±1 kV to ±5 kV) to a material surface and measuring the charge decay half-life—the time required for the charge to dissipate to 10% or 1% of its initial value. *Global Leading Market Research Publisher QYResearch announces the release of its latest report “Static Decay Meter – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″*. Based on historical analysis (2021–2025) and forecast calculations (2026–2032), this report provides a comprehensive assessment of market size, competitive positioning, and technology adoption curves across electronics manufacturing, medical protection, automotive, and industrial material applications.

Market Sizing & Core Keyword Integration:

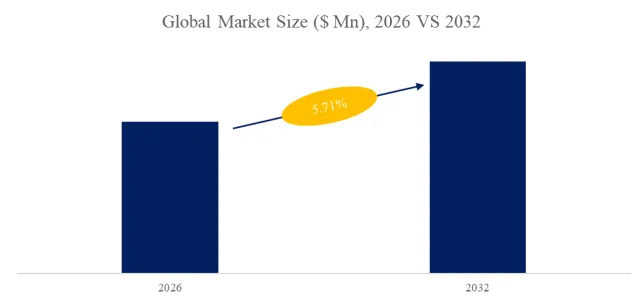

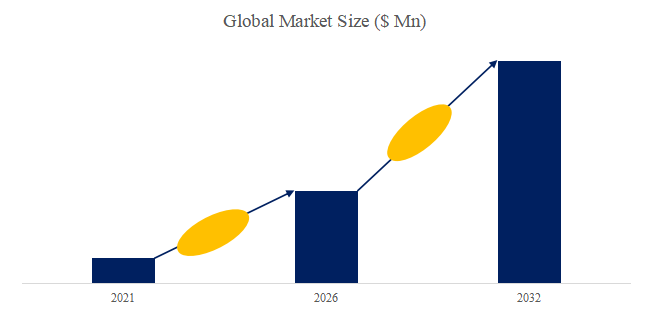

The global market for Static Decay Meters was valued at approximately US$ 97 million in 2025 (QYResearch consolidated estimate) and is projected to reach US$ 137 million by 2032, growing at a CAGR of 5.1% from 2026 to 2032. Three core technical keywords govern this market’s trajectory: Electrostatic Dissipation Speed (measured in seconds or milliseconds for charge to decay to a safe threshold), Charge Decay Half-Life (the time for initial charge to reduce by 50%, a key material qualification metric), and Surface Resistivity Correlation (the relationship between a material’s bulk resistance and its real-world static decay performance). A fourth emerging keyword, In-Situ Monitoring (real-time ESD measurement on production lines), is increasingly differentiating advanced instruments from laboratory-only units.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)

https://www.qyresearch.com/reports/6067738/static-decay-meter

Product Definition & Technical Foundation:

A Static Decay Meter (also known as an electrostatic decay tester or charge decay analyzer) quantifies how quickly a material dissipates an applied electrostatic charge. The instrument operates by: (a) charging a material sample to a specified voltage using a corona discharge or contact charging method, (b) monitoring the voltage decay over time via a non-contact electrostatic probe, and (c) reporting the charge decay half-life (t50) and decay to 1% (t99) or 0.1% (t99.9). This measurement is critical for qualifying ESD-safe materials such as static-dissipative floor mats, workbench surfaces, wrist straps, packaging films, and cleanroom garments. Unlike surface resistivity meters (which measure DC resistance under low voltage), static decay meters assess real-world electrostatic behavior under high-voltage conditions, capturing effects like charge injection, polarization, and air ionization that resistivity alone cannot reveal.

Segment-Level Analysis: Table-Type vs. Portable Instruments

Table-Type Static Decay Meters:

This segment represented 62% of revenue in 2025, driven by laboratory qualification and incoming material inspection in semiconductor fabs and medical device manufacturing. Table-type units offer controlled environmental chambers (temperature and humidity regulation per IEC 61340-2-1 standards), automated test sequences, and data logging for regulatory compliance. A typical user case: a leading automotive electronics supplier in Germany installed 18 table-type static decay meters across its component qualification labs in Q4 2025, following a field failure traced to a static-dissipative tray that passed resistivity testing (10⁶–10⁹ ohms) but exhibited 8-second charge decay half-life—exceeding the 2-second requirement for high-speed pick-and-place assembly. Post-installation, the company reduced ESD-related component damage by 73% within four months.

Portable Static Decay Meters:

Portable units accounted for 38% of 2025 revenue and represent the faster-growing segment at 6.8% CAGR. These battery-powered instruments are used for on-site verification of ESD control measures on production floors, in-field audits of supplier facilities, and troubleshooting of intermittent ESD events. Key advantages include lightweight design (under 1.5 kg), quick setup (under 2 minutes), and the ability to test installed surfaces (flooring, conveyor belts, workstations) without cutting samples. A recent user case: a major lithium-ion battery manufacturer in South Korea deployed 45 portable static decay meters across its gigafactory in January 2026, conducting weekly audits of 2,800 ESD-critical surfaces. The program identified 14% of workstations with electrostatic dissipation speed exceeding the 0.5-second threshold for cell assembly areas, enabling targeted remediation before production incidents occurred.

Recent Industry Data, Policy Developments & Technical Depth (Last 6 Months – October 2025 to April 2026):

Semiconductor Manufacturing Advances Driving Precision Requirements:

As logic chips advance to 3nm and below nodes, the tolerance for electrostatic damage has shrunk proportionally. According to industry data from SEMI (Global Semiconductor Equipment and Materials International) published in February 2026, ESD sensitivity of advanced gate-all-around (GAA) transistors is now below 10 volts—compared to 50–100 volts for 28nm planar devices. This has raised the required electrostatic dissipation speed measurement resolution from 0.5-second to 0.1-second levels. Leading static decay meter manufacturers (including Electro-Tech Systems and Prostat Corporation) have introduced high-speed sampling probes (1 kHz update rate) capable of capturing sub-100-millisecond decay events, but these features add 40–60% to instrument costs, creating a two-tier market.

New Energy Battery Safety – A Major Demand Driver:

The production of lithium-ion power batteries presents unique ESD risks: static discharge can ignite electrolyte vapors or puncture separator films, leading to thermal runaway. According to China’s Ministry of Industry and Information Technology (MIIT) guidance issued December 2025, battery cell assembly lines must now verify the charge decay half-life of all handling trays, fixture coatings, and cleanroom garments at weekly intervals. The total addressable demand for static decay meters in the global battery sector is estimated to exceed 35,000 units by 2030 (QYResearch battery industry cross-analysis). A case study: a top-three global EV battery manufacturer (headquartered in China) standardized on portable static decay meters across 26 production sites in Q1 2026, following a minor fire incident traced to a failed ESD tray. The company now conducts 12,000+ decay time measurements monthly, with non-compliant materials rejected before entering the production floor.

Medical Sterile Environment Monitoring:

Post-COVID-19, regulatory scrutiny of medical device cleanrooms has intensified. The FDA’s revised Quality System Regulation (QSR) effective January 2026 explicitly cites ESD control as a “critical process parameter” for manufacturing implantable electronics (pacemakers, neurostimulators) and sterile packaging. Static decay meters are now required for quarterly validation of cleanroom flooring and garment materials. The medical segment demand is projected to double by 2030, from approximately 1,200 units annually to 2,500 units.

Policy Driver – China’s Domestic Substitution and Tax Incentives:

China’s “Made in China 2025″ initiative has allocated over RMB 50 billion (approximately US$6.9 billion) for advanced manufacturing R&D, including ESD measurement instrumentation. By 2025, domestic-brand static decay meters (e.g., Chengwei Instrument, Shiruide Testing Instruments, Hongda Experimental Instruments) had reached approximately 60% share of the Chinese market, up from 35% in 2020. High-tech enterprise certification (reducing corporate income tax to 15% from standard 25%) and export rebate policies have accelerated domestic substitution. However, a technical gap remains: according to a January 2026 evaluation by China’s National Institute of Metrology, domestic meters show 15–20% higher measurement variability than imported equivalents (Electro-Tech Systems, Prostat) in high-humidity conditions (>60% RH), limiting their adoption in semiconductor and medical applications.

Technical Barrier – Sensor Distortion in Harsh Environments:

The most persistent technical challenge in static decay measurement is sensor accuracy degradation in high-humidity (over 70% RH) or strong electromagnetic interference (EMI) environments. Field data from a multinational electronics contract manufacturer (Q4 2025) showed that standard non-contact electrostatic probes exhibited distortion rates up to 30% when used within 2 meters of operating pick-and-place machines or RF welders. The root cause is charge leakage through humid air pathways and EMI-induced offset in the probe’s preamplifier. High-end instruments (Advanced Energy, DEKRA) incorporate guarded sensors and active EMI cancellation, increasing cost by 2–3×. The import dependence for high-sensitivity sensors (gallium nitride or MEMS-based designs) exceeds 60% globally, with leading suppliers concentrated in Japan (Shishido Electrostatic), Germany, and the United States.

独家观察 – Manufacturing Paradigm: Discrete Instrument vs. Integrated ESD Workstation

The static decay meter industry exhibits a divergence between discrete instrument manufacturers (producing stand-alone meters for laboratory use) and integrated ESD solution providers (embedding decay measurement into smart workstations with real-time data upload). Traditional vendors (DAIEI KAGAKU SEIKI MFG, IDB Systems, Prostat) focus on discrete instruments, emphasizing measurement accuracy and certification traceability. However, a newer category of integrated systems—exemplified by advanced ESD workstations from European and Chinese vendors—incorporates in-line static decay sensors that automatically log material qualification data into manufacturing execution systems (MES). A December 2025 pilot at a German automotive electronics plant showed that integrated systems reduced ESD compliance audit time by 87% (from 6 hours to 47 minutes per week) but required 25% higher upfront capital. The integrated approach is gaining traction in Industry 4.0-aligned factories, while discrete instruments remain dominant in third-party testing labs and smaller manufacturers.

独家观察 – Industry Segmentation: Semiconductor vs. General Industrial Material

Semiconductor and Electronics (approximately 45% of 2025 revenue, highest growth at 6.5% CAGR):

This segment demands the highest measurement precision: charge decay half-life resolution to 0.01 seconds, test voltages up to ±5 kV, and environmental chamber control to ±2% RH. Users include wafer fabs, assembly/test houses, and equipment manufacturers. A critical requirement is compliance with ANSI/ESD STM11.11 and IEC 61340-2-1 standards. Major semiconductor companies (Intel, TSMC, Samsung) specify approved static decay meter models in their supplier quality manuals; instruments not on the approved list must undergo expensive correlation studies. This creates strong brand loyalty—once a fab qualifies a meter (typically Electro-Tech Systems or Prostat), replacement cycles extend 5–7 years.

Medical Protection and Cleanroom (approximately 28% of 2025 revenue):

Medical applications prioritize cleanability and validation traceability. Sterile gowning materials, surgical drapes, and cleanroom wipes must demonstrate both electrostatic dissipation speed (typically <2 seconds to 1% of initial charge) and low particle shedding. FDA Quality System Regulation (21 CFR 820) requires documented evidence of ESD control material qualification, making static decay meters mandatory for medical device contract manufacturers. A case study: a Puerto Rico-based manufacturer of implantable cardiac monitors implemented weekly decay testing of cleanroom garments in Q3 2025 using portable meters from Static Clean International. Over six months, the program identified 12% of garments with degraded ESD performance (extended charge decay half-life beyond the 1-second limit), all of which were replaced before they could cause field failures.

Industrial Material and Others (approximately 27% of 2025 revenue – packaging, textiles, automotive interiors):

This segment is the most price-sensitive, with buyers often selecting lower-cost portable meters from regional Chinese vendors (Shiruide, Hongda, Sataton). Applications include qualifying antistatic packaging films (per MIL-PRF-81705), automotive interior textiles (to prevent seat discharge shocks), and industrial flooring. Unlike semiconductor users who require laboratory-grade accuracy, industrial users prioritize speed (under 5 minutes per test) and simplicity (pass/fail indication without data analysis). The challenge for vendors is balancing cost (target price under US$3,000) with sufficient accuracy to meet industry standards.

Technical Frontier – Gallium Nitride Sensors and AI Compensation:

Recent innovations are expanding measurement capabilities. Gallium nitride (GaN) electrostatic sensors, introduced by Advanced Energy in January 2026, offer micro-nano level charge sensitivity and 30% faster response time compared to conventional JFET-based probes. Meanwhile, AI algorithms combined with edge computing are being deployed to compensate for environmental interference—a system demonstrated by DEKRA in March 2026 reduced humidity-induced measurement error from 18% to 4% across the 20–80% RH range using a neural network trained on 50,000 decay curves. Additionally, 5G wireless modules (now included in over 40% of new premium static decay meters) support remote monitoring and predictive maintenance, alerting quality managers when sensor drift exceeds user-defined thresholds. These features align with Industry 4.0 requirements for real-time process control but add US$1,500–US$3,000 to instrument costs.

Segment Summary (as below):

Segment by Type

- Table Type (laboratory qualification, environmental chamber, high accuracy; US$8,000–US$25,000)

- Portable (on-site verification, battery-powered, moderate accuracy; US$3,000–US$10,000)

Segment by Application

- Medical Protection (cleanroom garments, surgical drapes, sterile packaging)

- Industrial Material (packaging films, textiles, flooring, automotive interiors)

- Others (semiconductor handling trays, battery assembly, aerospace coatings)

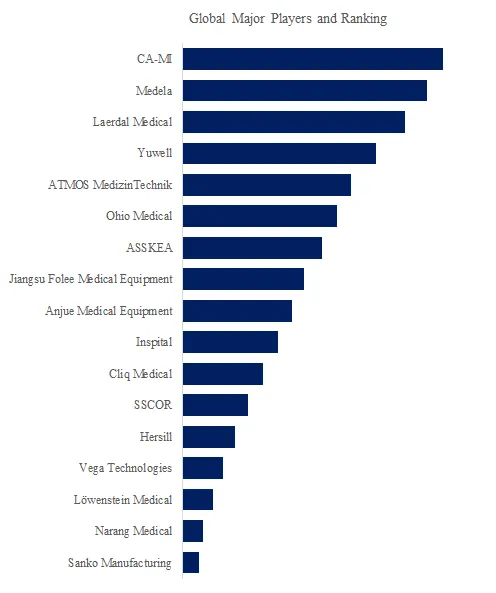

Competitive Landscape Summary (Selected Vendors – Data from QYResearch & Public Filings):

- Electro-Tech Systems (ETS): Global market leader in table-type static decay meters; 24% revenue share. Preferred by semiconductor fabs; launched high-speed 1 kHz sampling probe (February 2026).

- Prostat Corporation: Strong in portable instruments; offers Bluetooth-enabled units with smartphone data logging.

- Advanced Energy (Monroe Electronics): Premium segment leader; introduced GaN sensor-based meter (January 2026) with sub-10-millisecond decay resolution.

- Shishido Electrostatic (Japan): Dominant in Asian semiconductor market; known for exceptional humidity stability (±3% measurement variance from 30–70% RH).

- DEKRA: Focus on calibration services and certified instruments; operates 14 ESD calibration labs globally.

- DAIEI KAGAKU SEIKI MFG, IDB Systems, Static Clean International: Established players with strong regional distribution in Japan, Europe, and North America respectively.

- GESTER International, Chengwei Instrument, Shiruide, Hongda, Derick, Sataton, Huitao, Standard Groups, Source-Grid Scientific, SHANGHAI CHENG SI, SHANDONG PUCHUANG: Chinese domestic vendors serving price-sensitive industrial segment; collectively hold ~55% of China market but under 10% of global premium segment.

Forward-Looking Summary (2026–2032):

The static decay meter market will continue its steady 5%+ growth trajectory, driven by three irreversible trends: (1) semiconductor scaling to sub-3nm nodes requiring 0.1-second decay measurement resolution, (2) battery industry ESD safety mandates following high-profile thermal runaway incidents, and (3) regulatory alignment of ESD control as a critical process parameter in medical device manufacturing. The primary technical challenge remains sensor accuracy in high-humidity and EMI environments—a problem that AI-based compensation and GaN sensors are beginning to address but not yet solve at affordable price points. The market will increasingly bifurcate between premium table-type units (US$15,000+, semiconductor/medical/R&D) and lower-cost portable meters (US$4,000–8,000, general industrial). Domestic Chinese vendors will continue gaining share in their home market but face an uphill battle in international premium segments until sensor accuracy parity is achieved. For granular 10-year forecasts by type, application, and region, including detailed analysis of the 15 national standards (such as GB/T 7689) and their enforcement gaps, QYResearch’s full report provides essential decision-support data for quality managers, ESD program leaders, and industrial investors.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp