Introduction: Addressing Grid Stability, Telecom Backup Reliability, and Infrastructure Modernization Pain Points

For utility operators, telecommunications providers, and transit authorities, battery backup is not a convenience—it is a critical infrastructure requirement. A 1-second power interruption at a 5G cell tower disrupts thousands of calls; a 5-minute outage at a data center costs $5,000–10,000 per minute; a grid frequency drop of 0.1Hz can trigger blackouts affecting millions. Traditional lead-acid batteries, while low-cost, suffer from short cycle life (300–500 cycles), high maintenance (water topping, terminal cleaning), and poor performance in temperature extremes (capacity drops 50% at -20°C). The result: infrastructure operators face frequent battery replacements (every 3–5 years), unplanned outages (aging batteries fail without warning), and high total cost of ownership (maintenance labor, replacement costs). Global Leading Market Research Publisher QYResearch announces the release of its latest report “Infrastructure Batteries – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Infrastructure Batteries market, including market size, share, demand, industry development status, and forecasts for the next few years.

For telecommunications tower operators (cell sites, data centers), power grid utilities (frequency regulation, peak shaving), and rail transit authorities (signaling backup, traction power), the core pain points include achieving 10–20 year battery life (reduce replacement frequency), enabling remote monitoring (no site visits for maintenance), and supporting MW-scale energy storage (grid stabilization, renewable integration). Infrastructure batteries address these challenges as large-scale energy storage batteries supporting stable operation of various infrastructure systems—featuring high capacity (MWh scale), long life (10–20 years), and high safety (thermal runaway prevention). As 5G telecom expansion (1.4M new cell sites annually), renewable energy grid integration (solar/wind require storage for frequency regulation), and rail transit electrification (new metro lines) accelerate, the infrastructure battery market is experiencing explosive growth, with lithium-ion rapidly replacing lead-acid in most applications.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6096463/infrastructure-batteries

Market Sizing and Recent Trajectory (Q1–Q2 2026 Update)

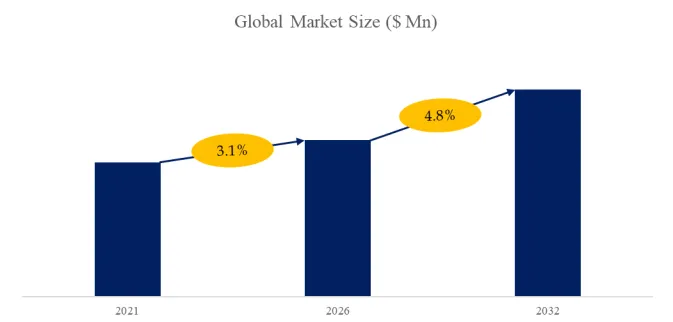

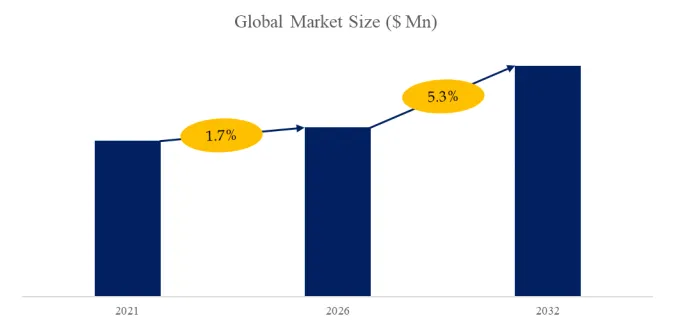

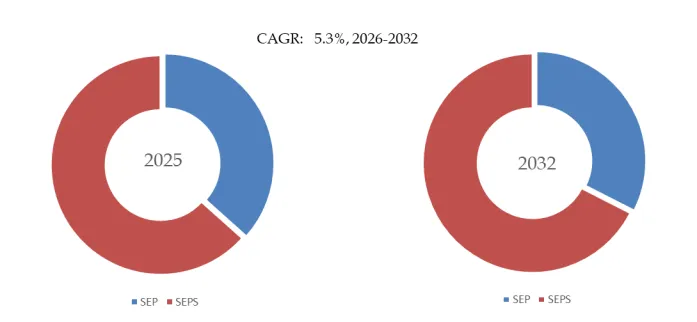

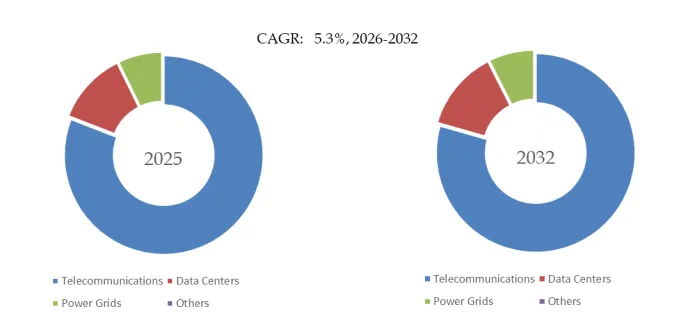

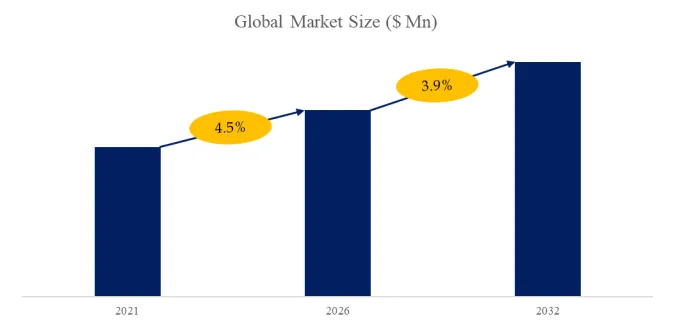

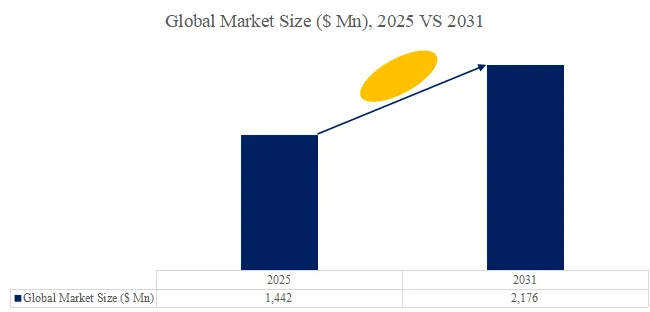

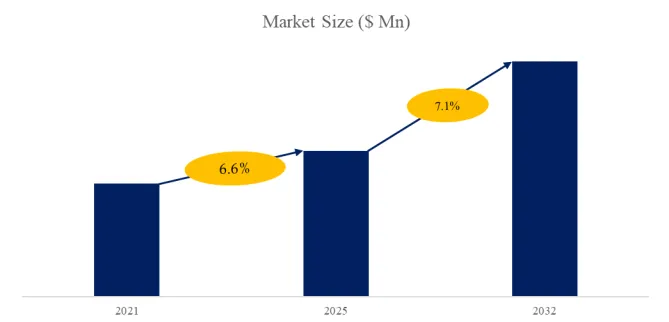

The global market for Infrastructure Batteries was estimated to be worth US$ 49,670 million in 2025 and is projected to reach US$ 139,260 million, growing at a CAGR of 16.1% from 2026 to 2032. In 2024, global production reached approximately 50,355 MWh, with an average global market price of around US$ 847 per kWh. Preliminary data for the first half of 2026 indicates explosive demand in telecommunications (5G rollout requiring 2–4 hours backup at 50,000+ new sites monthly), power grid energy storage (US Inflation Reduction Act, EU REPowerEU driving 100GW+ storage by 2030), and urban transportation (metro, light rail, bus rapid transit). The lithium-ion battery segment dominates (68% of revenue, fastest-growing at CAGR 19.5%) for telecom, power, and transportation applications requiring long cycle life (4,000–8,000 cycles) and high energy density. The lead-acid battery segment (28% of revenue, declining -2% CAGR) persists in legacy telecom sites and cost-sensitive power backup. The power application segment (grid-scale storage) leads (45% of revenue, fastest-growing at CAGR 22%), followed by telecommunications (30%), railways (12%), urban transportation (8%), and others (5%).

Product Mechanism: LFP vs. NMC for Infrastructure, Cycle Life, and Safety

Infrastructure batteries refer to large-scale energy storage batteries used to support the stable operation of various infrastructure systems. They usually have characteristics such as high capacity, long life and high safety.

A critical technical differentiator is chemistry (LFP vs. NMC vs. Lead-Acid), cycle life, and safety certification:

- Lithium-Ion (LFP – Lithium Iron Phosphate) – Safety-focused chemistry for stationary storage. Advantages: superior safety (no thermal runaway, even when punctured/overcharged), long cycle life (4,000–8,000 cycles to 80% capacity), wide temperature range (-20°C to +60°C), 15–20 year lifespan. Disadvantages: lower energy density (150–160 Wh/kg) vs. NMC, higher cost than lead-acid ($200–300/kWh vs. $100–150/kWh). Applications: telecom backup, grid storage, rail signaling backup. Market share: 55% of Li-ion segment (fastest-growing).

- Lithium-Ion (NMC – Nickel Manganese Cobalt) – Energy density-focused for space-constrained applications. Advantages: higher energy density (200–250 Wh/kg), smaller footprint for same capacity. Disadvantages: shorter cycle life (2,000–4,000 cycles), thermal runaway risk (requires robust BMS, fire suppression). Applications: urban transportation (bus depots, light rail), some grid storage. Market share: 13% of Li-ion segment.

- Lead-Acid (VRLA, AGM, Gel) – Legacy technology. Advantages: lowest upfront cost ($100–150/kWh), recyclable (98% recycling rate), simple charging. Disadvantages: short life (3–7 years, 300–500 cycles), temperature sensitive (capacity drops 50% at -20°C), requires maintenance (flooded) or monitoring (VRLA), heavy (3–5× Li-ion for same capacity). Applications: legacy telecom sites, small-scale UPS. Market share: 28% of revenue (declining -2% CAGR).

- Cycle Life Comparison – LFP: 4,000–8,000 cycles (15–20 years at daily cycle). NMC: 2,000–4,000 cycles (7–10 years). Lead-acid: 300–500 cycles (3–5 years, less with deep cycling). For daily cycle applications (grid frequency regulation), LFP required; lead-acid impractical (annual replacement).

Recent technical benchmark (March 2026): GS Yuasa’s LFP telecom battery (48V, 200Ah, 9.6kWh, $2,400) achieved 6,000 cycles at 80% DoD, 15-year design life, and -20°C to +60°C operation with integrated BMS (cell balancing, temperature monitoring). Independent testing (NTT DoCoMo) confirmed 99.999% reliability over 5-year field trial (10,000 batteries deployed).

Real-World Case Studies: Telecom Backup, Grid Storage, and Rail Signaling

The Infrastructure Batteries market is segmented as below by battery type and application:

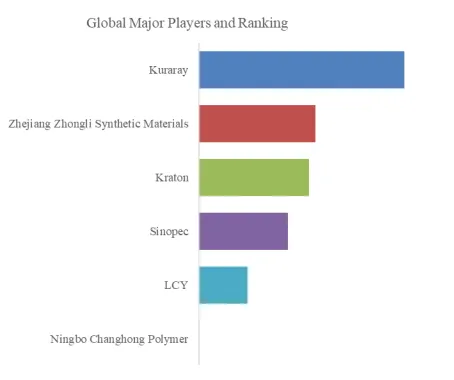

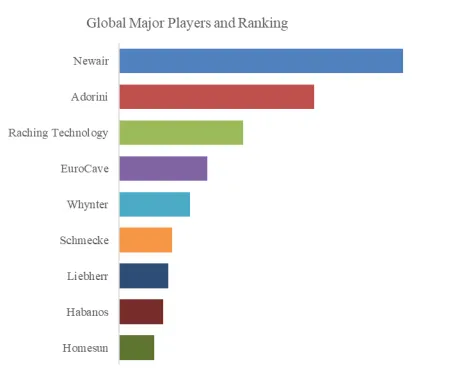

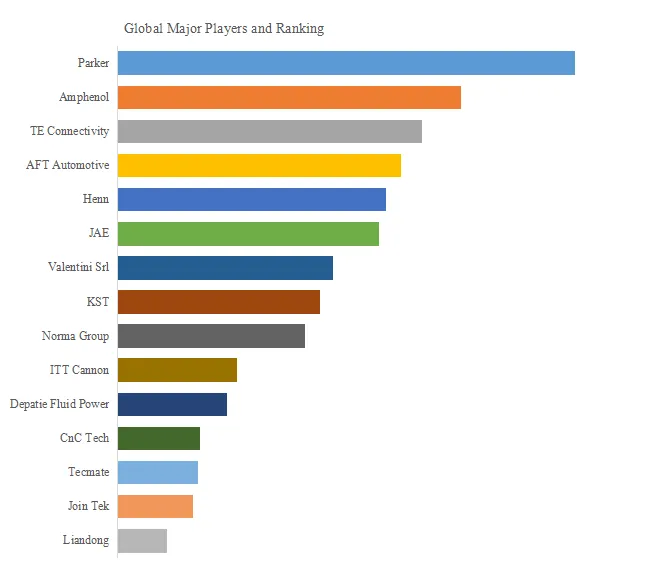

Key Players (Selected):

GS Yuasa, Hoppecke, East Penn Manufacturing, Saft, Exide Industries, LEOCH, Amara Raja, HBL Power Systems, Eastman New Energy, Sakthi Power, Radix Battery, C&D Technologies

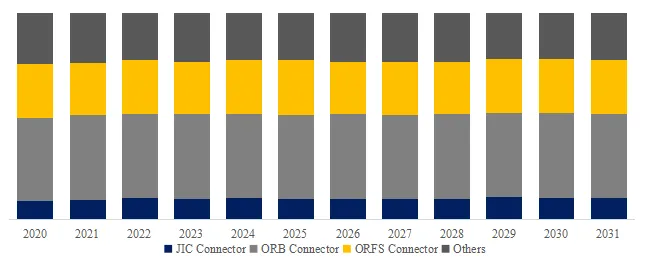

Segment by Type:

- Lead-acid Battery – VRLA, AGM. 28% of revenue (declining -2% CAGR).

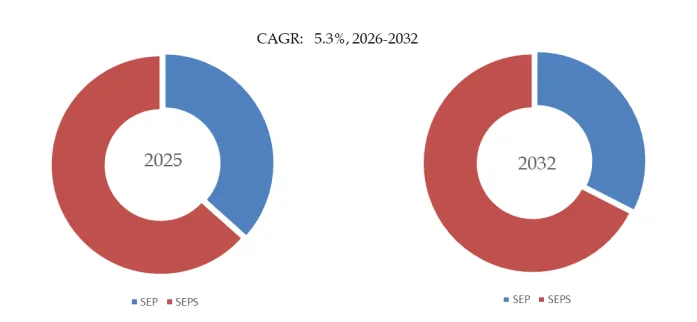

- Lithium-ion Battery – LFP (55%) + NMC (13%). 68% of revenue (CAGR 19.5%).

- Others – Ni-Cd, flow batteries. 4% of revenue.

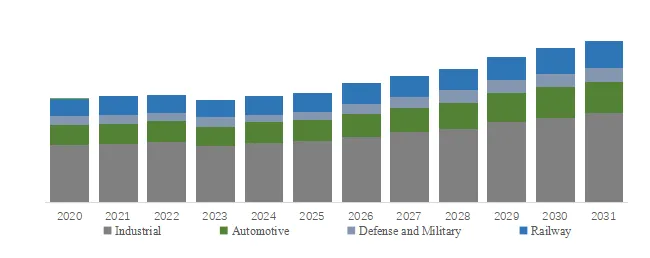

Segment by Application:

- Telecommunications – Cell tower backup. 30% of revenue.

- Power – Grid storage, frequency regulation. 45% of revenue (CAGR 22%).

- Urban Transportation – Bus depot charging, light rail. 8% of revenue.

- Railways – Signaling backup, traction power. 12% of revenue.

- Others – Data centers, hospitals. 5% of revenue.

Case Study 1 (Telecommunications – 5G Cell Tower Backup): Verizon (US) deployed 50,000 LFP batteries (GS Yuasa, 48V, 200Ah, 9.6kWh, $2,400 each) for 5G cell tower backup (4-hour runtime). Previous lead-acid required replacement every 4 years (tower climb $500 per visit, battery $800). LFP: 15-year life, maintenance-free, remote monitoring (BMS reports state-of-health). Verizon estimates $50M annual maintenance savings across 50,000 towers. Telecom segment (30% of revenue) growing 15% CAGR.

Case Study 2 (Power – Grid Frequency Regulation, 100MWh): UK National Grid deployed 100MWh LFP battery storage (GS Yuasa, 20MW power, 5-hour duration, $30M) for frequency regulation (FFR). Requirements: 4,000+ cycles (daily charge/discharge), 20-year life, and sub-second response (grid stabilization). LFP provides 800ms response (vs. 5–10 seconds for gas peaker). Battery expected 10,000 cycles (27 years at daily cycle). Power segment (45% of revenue) fastest-growing (CAGR 22%).

Case Study 3 (Railways – Signaling Backup, London Underground): London Underground deployed LFP batteries (Hoppecke, 110V, 100Ah, 11kWh, $3,000 per unit) for signaling backup (30-minute runtime). Requirements: 15-year life (no access for maintenance), -10°C to +40°C operation (tunnel environment), and fire safety (LFP no thermal runaway). Underground has 5,000 signaling locations → $15M battery spend. Railways segment (12% of revenue) growing 10% CAGR.

Case Study 4 (Urban Transportation – Electric Bus Depot Charging): Los Angeles Metro (electric bus fleet, 500 buses) deployed NMC batteries (East Penn, 800V, 500kWh per charger, $200k per unit) for depot charging energy storage (peak shaving, reduce demand charges). NMC energy density (smaller footprint) critical for space-constrained depot. Charging storage reduces demand charges $50k per charger annually (payback 4 years). Urban transportation segment (8% of revenue) growing 18% CAGR.

Industry Segmentation: Lithium-Ion vs. Lead-Acid and Application Perspectives

From an operational standpoint, lithium-ion batteries (68% of revenue, fastest-growing at 19.5% CAGR) dominate new infrastructure deployments due to long cycle life (4,000–8,000 cycles), maintenance-free operation, and remote monitoring (BMS). LFP (55% of Li-ion) dominates telecom, power, and rail (safety-critical). NMC (13% of Li-ion) dominates space-constrained urban transportation. Lead-acid (28%, declining) persists in legacy telecom sites (3–5 year replacement cycles) and cost-sensitive backup (<10kW). Power (45% of revenue, fastest-growing at 22% CAGR) driven by renewable integration (solar/wind + storage) and grid stabilization. Telecommunications (30%) driven by 5G rollout (1.4M new sites annually). Railways (12%) driven by signaling modernization. Urban transportation (8%) fastest-growing behind power (18% CAGR) driven by bus electrification.

Technical Challenges and Recent Policy Developments

Despite strong growth, the industry faces four key technical hurdles:

- Thermal runaway in NMC infrastructure batteries: NMC batteries in grid storage have caused fires (LNG terminal fire 2025, Arizona battery fire 2019). LFP eliminates thermal runaway (no oxygen release at high temperature). Policy shift: Many utilities now specify LFP only for grid storage.

- Second-life batteries for grid storage: EV batteries (80% capacity) can be repurposed for grid storage, reducing cost 30–50%. Challenges: battery-to-battery variability, warranty, and logistics. Second-life market projected 50GWh by 2030.

- Remote monitoring and predictive maintenance: Infrastructure batteries often in remote locations (telecom towers, substations). Cloud-based BMS monitoring (voltage, temperature, impedance) enables predictive failure detection (2–4 weeks advance warning). Smart batteries (with cellular/IoT) add 10–15% to cost.

- Recycling infrastructure for large-format Li-ion: Grid storage batteries (MWh scale) require specialized recycling (dismantling, crushing, material recovery). Policy update (March 2026): EU Battery Regulation requires 70% Li-ion recycling efficiency by 2030, 50% by 2027. Major players (GS Yuasa, Saft, EnerSys) establishing recycling partnerships.

独家观察: LFP Dominance in Grid Storage and 5G Driving Telecom Li-Ion Adoption

An original observation from this analysis is LFP dominance (80%+ of grid storage, 70%+ of telecom) due to safety (no thermal runaway) and cycle life (6,000–8,000 cycles). After 2020–2025 grid storage fires (Arizona, South Korea, China), utilities now specify LFP in tenders. LFP cost premium over NMC has dropped from 30% (2020) to 5–10% (2025, $200–220/kWh vs. $180–200/kWh). LFP grid storage projected 90% market share by 2030.

Additionally, 5G telecom rollout driving lithium-ion replacement of lead-acid. 5G base stations consume 2–4× power of 4G (massive MIMO, higher frequency), requiring 2–4 hour backup (10–20kWh). Lead-acid batteries (10–20kWh) weigh 500–1,000kg, require monthly maintenance (infeasible at 50,000+ new sites). LFP batteries (same capacity) weigh 150–300kg, maintenance-free, 15-year life. China Mobile, Verizon, Vodafone specifying LFP for new 5G sites; lead-acid only for legacy 4G sites (<10% of new deployments). Telecom Li-ion adoption 80%+ for new sites (2025), up from 30% (2020). Looking toward 2032, the market will likely bifurcate into LFP batteries for grid storage, telecom backup, rail signaling, and urban transportation (safety-driven, long cycle life, 15–20% annual growth) and lead-acid batteries for legacy telecom sites and cost-sensitive small UPS (declining 2–3% annually), with NMC limited to space-constrained urban transportation and niche grid applications.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp