Introduction: Addressing Gearbox Failure, Maintenance Downtime, and Energy Loss in Conveyor Systems

For mining operations managers, bulk material handling engineers, and industrial plant directors, traditional geared conveyor drives (motor + gearbox) present significant operational challenges. Gearboxes (helical, bevel, planetary) have limited service life (5–10 years), require regular maintenance (oil changes, bearing replacement, seal replacement), and fail unexpectedly (gear tooth wear, bearing seizure, lubricant leakage), causing unplanned downtime (10–50 hours per failure) and production loss ($50k–500k per hour in mining). Gearbox efficiency is 95–97% (2–5% energy loss), and gear noise is high (90–100 dB). Gearless conveyor drives address these limitations with direct drive technology – motor directly connected to conveyor pulley (no gearbox). Power transmission is achieved through advanced control (variable frequency drives, VFDs) and drive technology (permanent magnet synchronous motors, PMSM; synchronous reluctance motors, SynRM). Gearless drives offer higher efficiency (98–99%), lower noise (70–80 dB), longer service life (20–30 years), reduced maintenance (no oil changes, no gear replacement), and compact design (smaller footprint). As mining companies prioritize operational efficiency (reducing downtime, energy cost), safety (reducing maintenance exposure), and sustainability (energy savings), demand for gearless conveyor drives is growing. Global Leading Market Research Publisher QYResearch announces the release of its latest report “Gearless Conveyor Drive – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Gearless Conveyor Drive market, including market size, share, demand, industry development status, and forecasts for the next few years.

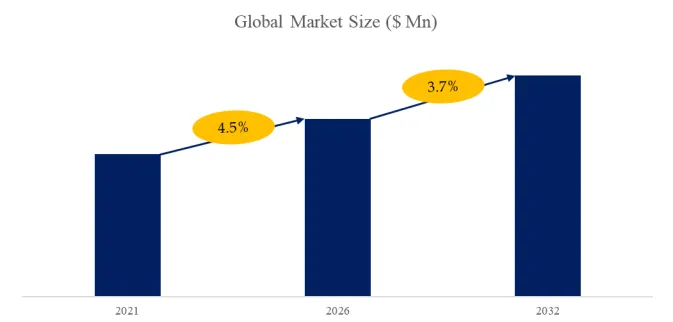

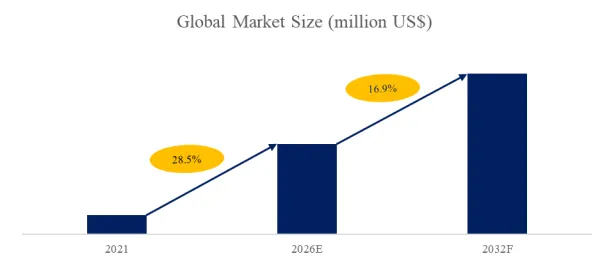

For mining equipment procurement managers, maintenance engineers, and industrial investors, the core pain points include achieving high efficiency (98–99% vs. gearbox 95–97%), long service life (20–30 years vs. gearbox 5–10 years), and reduced downtime (no gearbox failures, oil leaks). According to QYResearch, the global gearless conveyor drive market was valued at US$ [value] million in 2025 and is projected to reach US$ [value] million by 2032, growing at a CAGR of [%] .

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5754253/gearless-conveyor-drive

Market Definition and Core Capabilities

Gearless conveyor drive (direct drive) eliminates traditional gear transmission system (gearbox, coupling), using advanced control and drive technology to transfer power directly from motor to conveyor pulley. Core capabilities:

- Direct Drive Motor: Permanent magnet synchronous motor (PMSM) or synchronous reluctance motor (SynRM) directly coupled to conveyor drive pulley (no gearbox, no coupling). Low-speed, high-torque motor (100–1,000 RPM, 10–100 kNm). Compact design (smaller footprint, lighter weight).

- Variable Frequency Drive (VFD): Controls motor speed, torque, acceleration, deceleration. Soft start (reduced belt tension), load sharing (multiple drives), regenerative braking (energy recovery). Improves conveyor efficiency, reduces mechanical stress (belt, idlers, pulleys).

- Efficiency: Gearless drive 98–99% (motor 96–97%, VFD 98–99%) vs. geared drive 93–95% (motor 96%, gearbox 95–97%, coupling 99%). 3–5% energy savings (significant for high-power conveyors, 1–10 MW, 24/7 operation).

- Maintenance: Gearless drive has no gearbox (no oil changes, bearing replacement, seal replacement). Reduced maintenance cost (50–80%), reduced downtime (no gearbox failure). Service life 20–30 years (vs. gearbox 5–10 years).

- Noise: Gearless drive 70–80 dB (vs. geared drive 90–100 dB). Improved worker safety (hearing protection), reduced environmental noise.

Market Segmentation by Power Rating

- Below 3MW (30–35% of revenue, largest segment): Small to medium conveyors (short length, low tonnage). Used in underground coal mines, aggregate quarries, cement plants, and industrial material handling. Lower cost, simpler installation.

- 3-10MW (45–50% of revenue, fastest-growing at 10–12% CAGR): Large conveyors (long length, high tonnage). Used in open-pit mines (copper, iron ore, gold, coal), overland conveyors (5–20 km), and port terminals (ship loading/unloading). Gearless drive offers significant energy savings (3–5% of 5MW = 150–250 kW = $100k–200k/year electricity), reduced maintenance.

- More than 10MW (15–20% of revenue): Very large conveyors (extreme length, ultra-high tonnage). Used in mining (largest open-pit mines), long-distance overland conveyors (20–50 km), and high-capacity port terminals. Gearless drive essential (gearbox not feasible at >5MW).

Market Segmentation by Application

- Coal Mine (40–45% of revenue, largest segment): Underground coal mines (belt conveyors for coal transport) and open-pit coal mines. Gearless drives reduce methane ignition risk (no gearbox sparks), improve safety. Energy savings, reduced maintenance (underground access difficult). High adoption in China, India, Australia, Indonesia, US.

- Metal Mine (35–40% of revenue, fastest-growing at 10–12% CAGR): Copper, iron ore, gold, zinc, nickel, lithium mines (open-pit, underground). Gearless drives for overland conveyors (long distance), incline conveyors (steep angles), and high-tonnage conveyors. Reduced downtime (critical for 24/7 mining operations), lower operating cost (energy, maintenance).

- Others (15–20% of revenue): Aggregate quarries (crushed stone, sand, gravel), cement plants (limestone, clinker conveyors), port terminals (ship loading/unloading), power plants (coal conveyors), and industrial material handling (factory conveyors).

Technical Challenges and Industry Innovation

The industry faces four critical hurdles. Higher Initial Cost – gearless drive (motor + VFD) has 20–40% higher upfront cost than geared drive (motor + gearbox + coupling + VFD). Energy savings (3–5%), reduced maintenance (50–80%), and longer service life (20–30 years) provide payback 2–5 years. Motor Size & Weight – low-speed, high-torque PMSM is larger, heavier (2–5×) than high-speed motor + gearbox. Requires structural support (concrete foundation, steel frame), and may not fit existing conveyor drive frame (retrofit challenges). VFD Harmonics & Power Quality – VFD (6-pulse, 12-pulse, active front end) generates harmonics (5th, 7th, 11th, 13th), affecting power quality (voltage distortion, transformer heating). Harmonic filters (line reactors, passive filters, active filters) required for grid compliance (IEEE 519). Regenerative Energy & Braking – downhill conveyors (negative load) generate regenerative energy (motor acts as generator). VFD must handle regenerative power (braking resistor, regenerative drive, energy storage). Energy recovery (feed back to grid) improves efficiency.

独家观察: 3-10MW Gearless Drives Fastest-Growing Segment for Open-Pit Mining

An original observation from this analysis is the double-digit growth (10–12% CAGR) of 3-10MW gearless conveyor drives for open-pit mining (copper, iron ore, gold, lithium) and overland conveyors (5–20 km) . Open-pit mines expand deeper (pit depth 500–1,000 m), requiring longer, higher-tonnage conveyors. Gearless drives provide 3–5% energy savings (1–2 GWh/year per conveyor = $100k–200k/year electricity), reduced maintenance (no gearbox oil changes, bearing replacement), and higher reliability (99.5%+ uptime). 3-10MW segment projected 50%+ of gearless drive revenue by 2030 (vs. 45% in 2025). Additionally, permanent magnet synchronous motor (PMSM) gearless drives (higher efficiency, higher power density, lower weight) are replacing induction motor gearless drives. PMSM has 96–97% efficiency (vs. induction 94–95%), higher power factor (0.95–0.99 vs. 0.85–0.90), and smaller size (2–3× power density). PMSM segment projected 60%+ of gearless drive revenue by 2028.

Strategic Outlook for Industry Stakeholders

For CEOs, product line managers, and mining investors, the gearless conveyor drive market represents a steady-growth (8–10% CAGR), energy-efficient opportunity anchored by mining automation, energy cost reduction, and maintenance optimization. Key strategies include:

- Investment in 3-10MW gearless drives for open-pit mining and overland conveyors (fastest-growing segment) with PMSM technology, VFD control, and energy recovery.

- Development of retrofit kits (replace geared drive with gearless drive) for existing conveyors (reduce downtime, installation cost).

- Expansion into digital monitoring & predictive maintenance (IoT sensors, vibration monitoring, thermal imaging, oil analysis) for gearless drives (reduce unplanned downtime, extend service life).

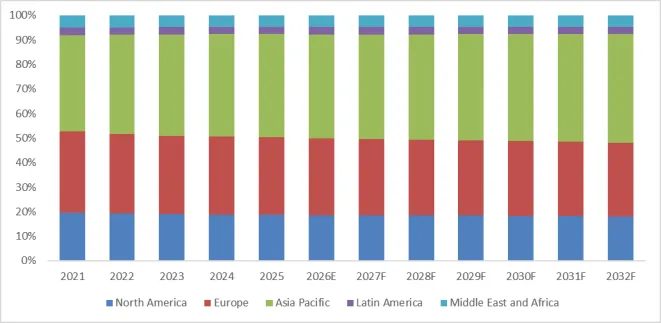

- Geographic expansion into Asia-Pacific (China, India, Australia, Indonesia) for coal, metal, and lithium mining; South America (Chile, Peru, Brazil) for copper and iron ore; Africa (South Africa, Zambia, DRC) for gold, copper, cobalt.

Companies that successfully combine high-efficiency PMSM, VFD control, and predictive maintenance will capture share in a multi-billion dollar market by 2032.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp