QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Ticket Resale Platform- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Ticket Resale Platform market, including market size, share, demand, industry development status, and forecasts for the next few years.

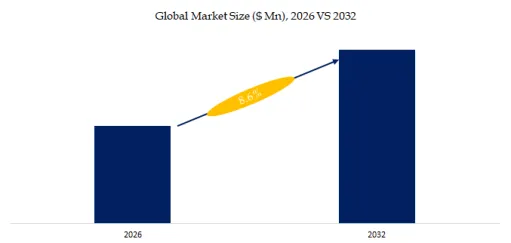

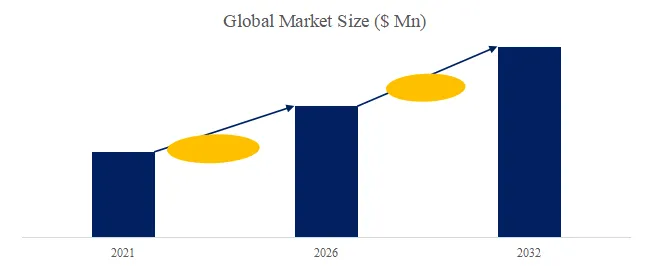

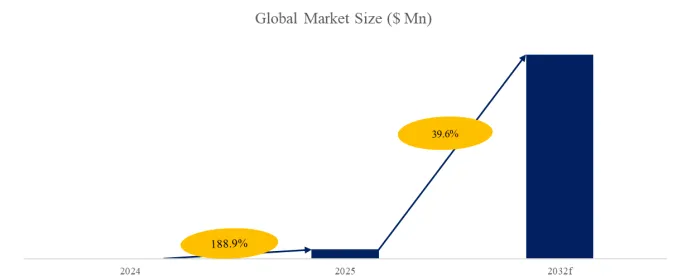

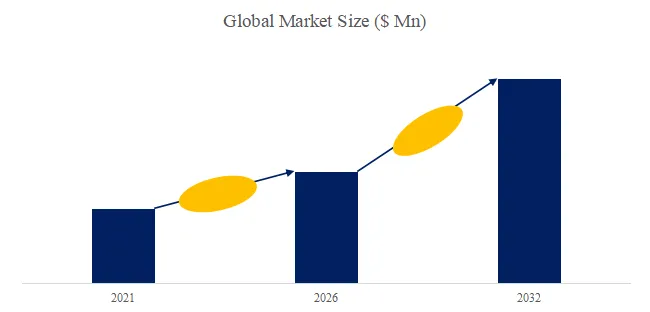

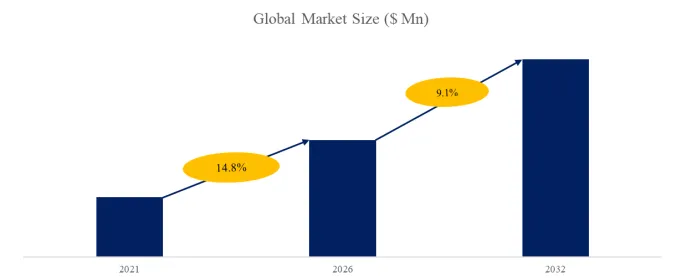

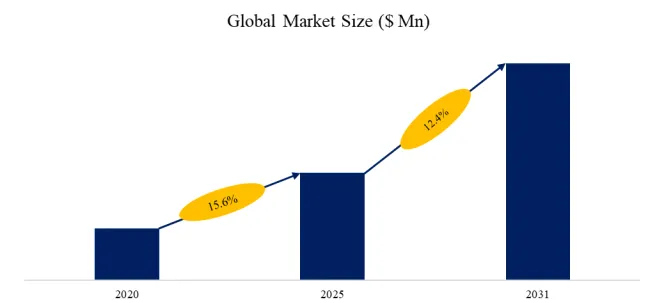

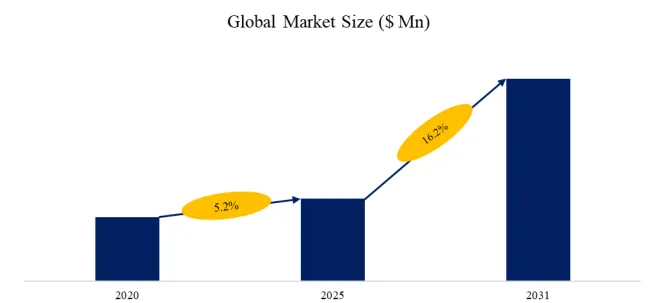

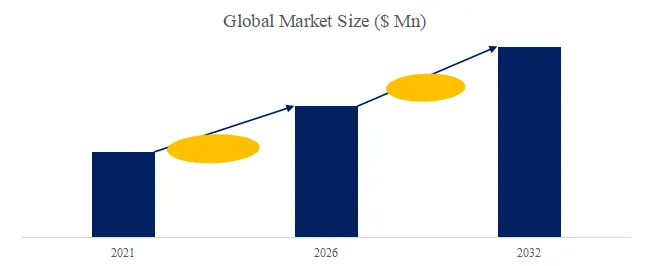

The global market for Ticket Resale Platform was estimated to be worth US$ 2315 million in 2025 and is projected to reach US$ 4098 million, growing at a CAGR of 8.5% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6699577/ticket-resale-platform

Ticket Resale Platform Product Overview

Ticket Resale Platforms are online or offline platforms that provide secondary ticketing services, allowing original ticket purchasers or holders to legally resell purchased tickets to other consumers. These platforms typically offer ticket verification, price formation, transaction security, and ticket delivery services to ensure transaction security and ticket authenticity. Resale platforms support various transaction models, including consumer-to-consumer (C2C), business-to-consumer (B2C), and officially certified resale models, covering sporting events, concerts, theater, festivals, and other large-scale events. Platform features typically include digital ticket transfer, dynamic pricing algorithms, mobile applications, and official barcode verification, capable of meeting the needs of reselling sold-out events, last-minute ticket purchases, and high-value seat upgrades. Resale platforms are an important part of the global ticketing ecosystem, with mature supply systems particularly prevalent in North America and Europe. In 2025, the gross profit margin of Ticket Resale Platforms was approximately 54.43%.

From a supply perspective, the North American market is the most mature region for Ticket Resale Platform, with a high concentration of platforms. Major companies include StubHub (including Viagogo), Ticketmaster Exchange, SeatGeek, and TickPick. The European market is dominated by fan-to-fan platforms such as TicketSwap and Twickets, with numerous but fragmented companies. In Japan and South Korea, the resale market is dominated by officially certified resellers, and independent platforms are relatively few due to real-name registration and anti-scalping policies. In China, the market is still primarily driven by the official resale functions of primary ticketing platforms, with independent secondary ticketing platforms virtually nonexistent. Overall, North America and Europe are the core supply areas, while Japan, South Korea, and China are restricted markets affected by policies and real-name registration.

From a demand structure perspective, Ticket Resale Platform mainly meet the needs of three types of users: first, replenishing tickets for sold-out events; second, last-minute ticket purchases for upcoming performances or events; and third, upgrading to premium seats or VIP areas. Different event types, platforms, and delivery methods significantly impact transaction frequency and price formation mechanisms. Officially certified resale platforms can improve transaction security and ticket credibility, while open C2C platforms emphasize price flexibility and supply diversity.

From an industry trend perspective, technology is driving transparency and compliance in the resale ticket market. Mobile apps, digital wallet transfers, official barcode verification, and dynamic pricing algorithms have become mainstream. In the future, the resale ticket market may see further regional concentration and integration with official platforms, while compliance regulations and fan protection policies will continue to affect price elasticity and platform operating models.

Ticket Resale Platform Market Summary

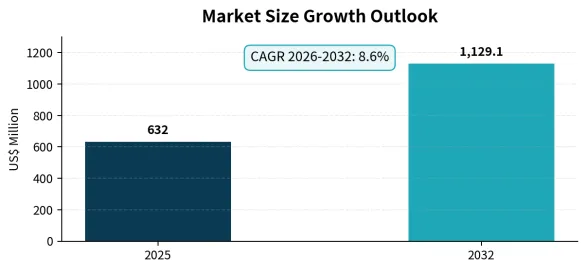

According to the latest market research report from QYResearch, the global Ticket Resale Platform market size will be approximately US$2.315 billion in 2025.

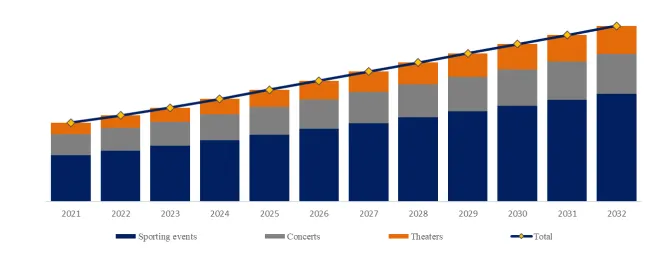

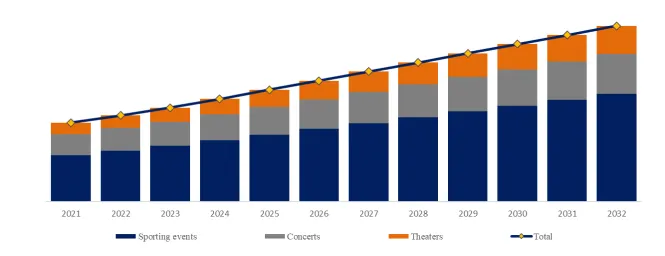

Figure00001. Global Ticket Resale Platform Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global Ticket Resale Platform Market Report 2021-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

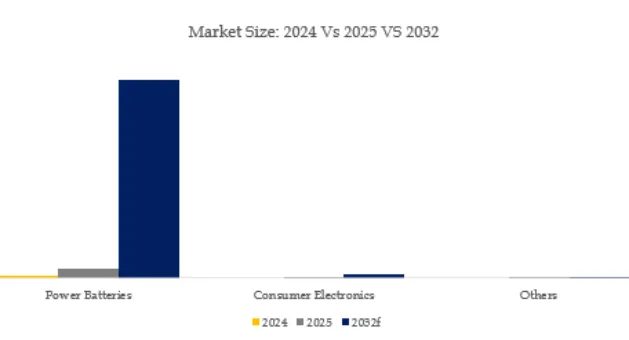

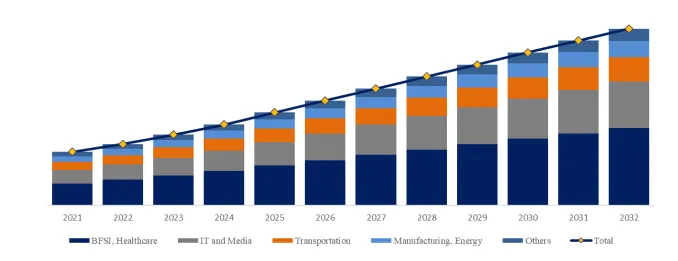

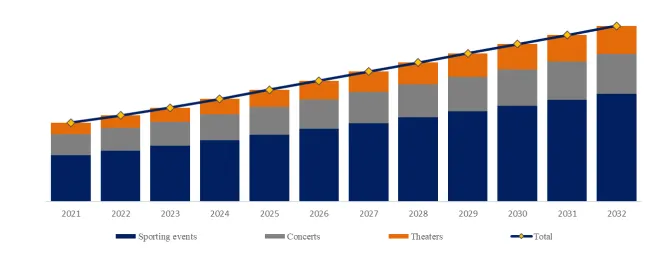

Figure00002. Ticket Resale Platform, Global Market Size, Split by Product Segment

Based on or includes research from QYResearch: Global Ticket Resale Platform Market Report 2021-2032.

In terms of product type, currently Sporting events is the largest segment, hold a share of 59.9%.

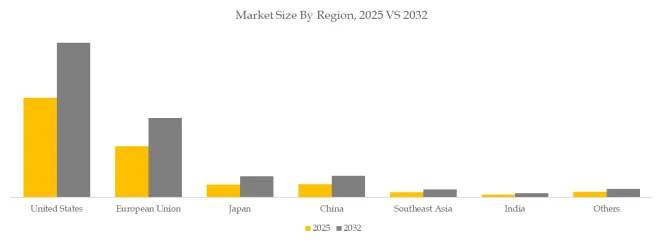

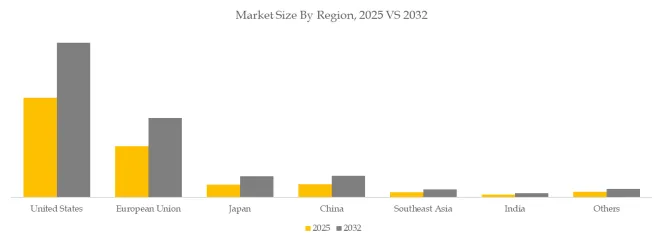

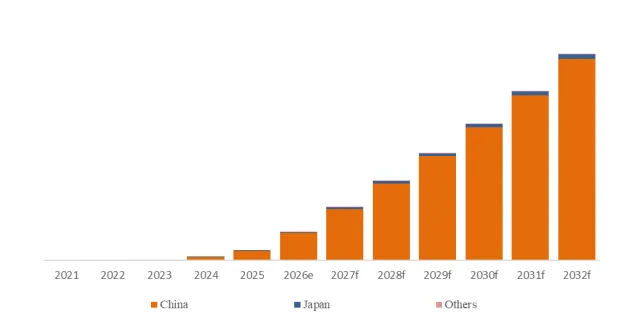

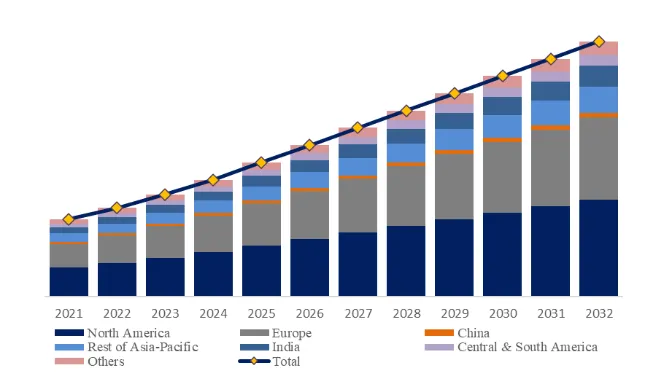

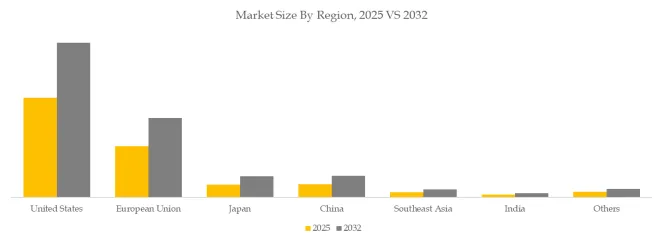

Figure00003. Ticket Resale Platform, Global Market Size, Split by Region

Based on or includes research from QYResearch: Global Ticket Resale Platform Market Report 2021-2032.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Ticket Resale Platform market is segmented as below:

By Company

StubHub(Viagogo)

Ticketmaster(Live Nation Entertainment)

Vivid Seats

TicketIQ

RazorGator(TickPick)

SeatGeek

Alliance Tickets

Coast to Coast Tickets

TicketCity

TicketNetwork

AXS Marketplace(AEG)

Gametime

EventTicketCenter

TicketSwap

Twickets

Ticket Camp(Mixi)

Interpark Ticket

Melon Ticket

GoTickets

Ticmint

See Tickets

Seated

Platinumlist

FanFair Alliance

CashorTrade

BookMyShow Resale

Dice

Tixel

MoreTickets

Dahepiao

Segment by Type

Official Resale

Fan-to-Fan Tickets

Brokered Tickets

Other

Segment by Application

Sporting Events

Concerts

Theaters

Others

Each chapter of the report provides detailed information for readers to further understand the Ticket Resale Platform market:

Chapter 1: Introduces the report scope of the Ticket Resale Platform report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Ticket Resale Platform manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Ticket Resale Platform market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Ticket Resale Platform in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Ticket Resale Platform in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Ticket Resale Platform competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Ticket Resale Platform comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Ticket Resale Platform market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Ticket Resale Platform Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Ticket Resale Platform Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Ticket Resale Platform Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp