1. Autonomous Ride-hailing Vehicles Market Summary

Autonomous ride-hailing vehicles refer to shared mobility vehicles that utilize technologies such as artificial intelligence, sensors, radar, and high-definition maps to provide passenger pick-up and drop-off services without human intervention. They combine the instant booking and route optimization systems of ride-hailing platforms, enabling vehicles to autonomously plan routes, avoid obstacles, and obey traffic rules based on passenger needs, providing a safe and convenient travel experience. Compared to traditional ride-hailing services, autonomous ride-hailing vehicles reduce reliance on human drivers and continuously optimize operational efficiency with the support of data and algorithms.

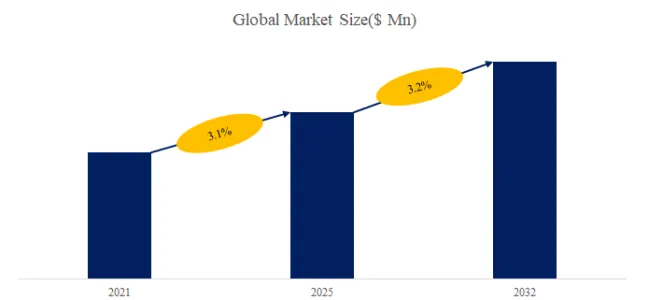

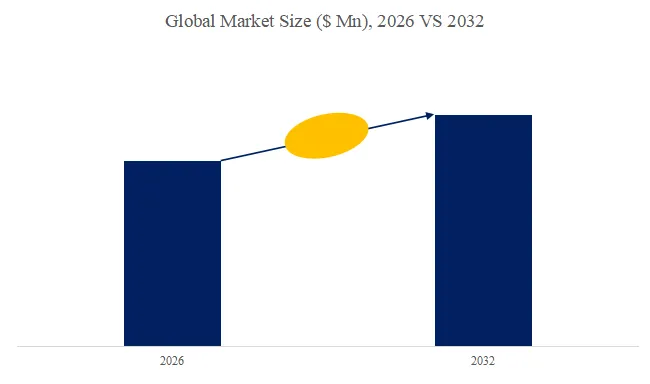

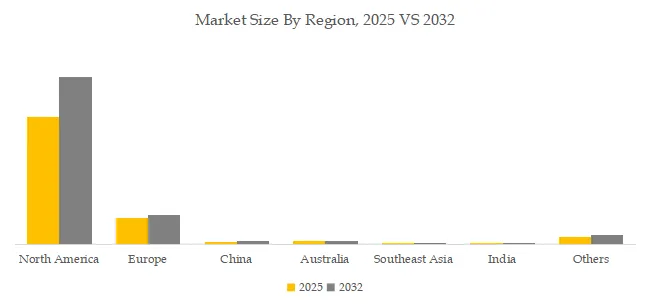

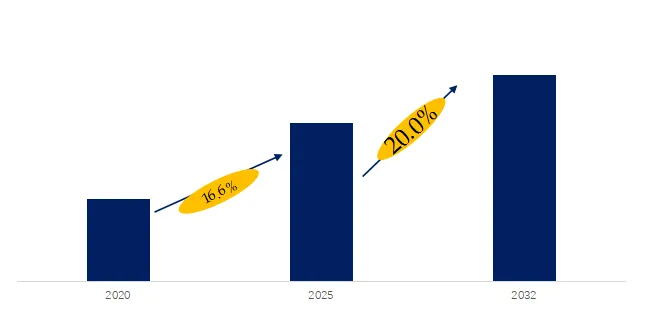

According to the latest research report from QYResearch, in terms of market size, the global Autonomous Ride-hailing Vehicles market size is projected to grow from USD 2 billion in 2025 to USD 7.3 billion by 2032, at a CAGR of 20.00% during the forecast period.

Figure00001. Global Autonomous Ride-hailing Vehicles Market Revenue Growth Rate, 2021-2032

Above data is based on report from QYResearch: Global Autonomous Ride-hailing Vehicles Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

2 Introduction of Major Manufacturers of Autonomous Ride-hailing Vehicles

| Serial Number |

Company |

| 1 |

Waymo |

| 2 |

Motional |

| 3 |

Aptiv |

| 4 |

Uber |

| 5 |

Lyft |

| 6 |

Tesla |

| 7 |

Baidu Apollo |

| 8 |

Honda |

| 9 |

Pony AI |

| 10 |

WeRide |

| 11 |

Verne |

| 12 |

Zoox |

| 13 |

Nuro Driver |

Source: Third-party data, QYResearch Research Team

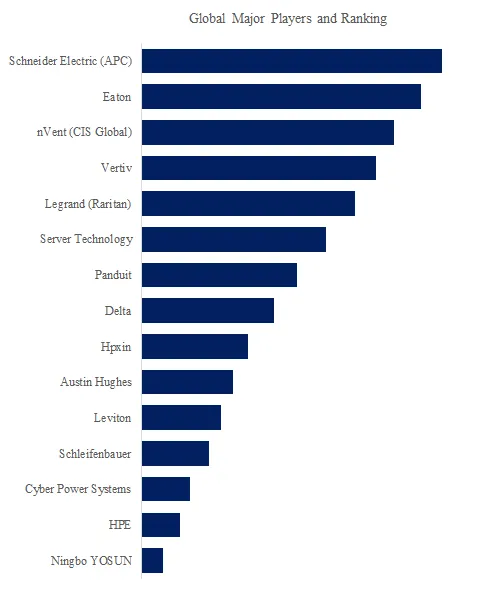

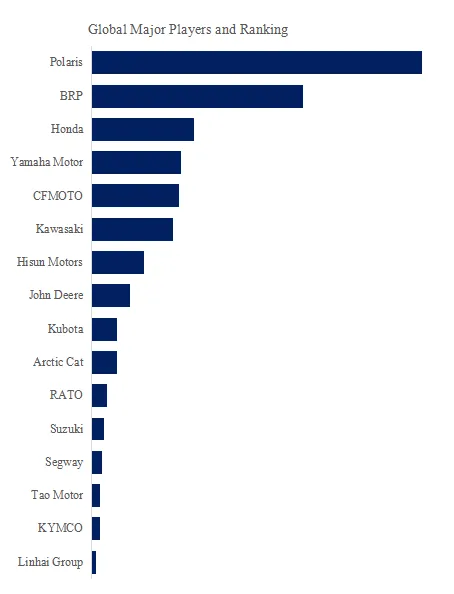

According to a survey by QYResearch’s Leading Enterprise Research Center, global Autonomous Ride-hailing Vehicles manufacturers include Waymo, Motional, Aptiv, Uber, Lyft, etc. By 2025, the top five global manufacturers will hold approximately 29% of the market share.

Introduction to Key Companies

Company 1

| Waymo |

Description |

| Company Introduction |

Founded in 2009, Waymo is a self-driving technology company under Alphabet, Google’s parent company, headquartered in California, USA. The company is dedicated to developing fully autonomous vehicle technology, integrating LiDAR, cameras, sensors, and artificial intelligence algorithms to enable vehicles to navigate autonomously in complex urban environments. Waymo is an industry leader in the safety, reliability, and scalability of driverless technology, driving the transition of autonomous driving from the experimental stage to commercialization. It also collaborates with automakers, logistics companies, and urban transportation departments to accelerate the construction of a smart transportation ecosystem. |

| Product Introduction |

Waymo’s self-driving ride-hailing service, called “Waymo One,” is already in commercial operation in cities such as Phoenix, Arizona. Passengers can book fully autonomous vehicles through a mobile app, requiring no driver intervention. The system uses high-precision maps, LiDAR, cameras, and artificial intelligence algorithms to perceive the environment in real time, plan routes, and drive safely. Waymo One provides services such as daily commutes and airport transfers, supports barrier-free travel, and employs strict safety standards and remote monitoring systems to ensure passenger safety. This product represents a leading global commercial model for driverless ride-hailing. |

Source: Third-party data, QYResearch Research Team

Company 2

| Motional |

Description |

| Company Introduction |

Founded in 2020 as a joint venture between Hyundai Motor and Aptiv, Motional, headquartered in Boston, USA, is a leading global innovator in autonomous driving technology. The company focuses on developing Level 4 highly automated driving systems, combining artificial intelligence, sensor fusion, and advanced driver assistance algorithms to enable vehicles to drive autonomously and safely on urban roads and highways. Motional actively collaborates with traffic management departments, automakers, and ride-hailing platforms to advance autonomous driving technology from experimental verification to large-scale commercialization, while prioritizing passenger experience and safety. |

| Product Introduction |

Motional’s autonomous ride-hailing service, “Motional Robotaxi,” is currently in pilot operation in Las Vegas and other cities in the United States. Passengers book vehicles via a mobile app, and the cars complete urban transportation tasks without human intervention. The vehicles are equipped with LiDAR, cameras, and advanced sensor fusion systems, combined with real-time AI decision-making algorithms to ensure obstacle avoidance, route planning, and adherence to traffic rules. Motional Robotaxi offers services such as daily commutes and airport transfers, and through remote monitoring and safety redundancy design, ensures passenger experience and driving safety, demonstrating advanced practices in the commercialization of autonomous driving. |

Source: Third-party data, QYResearch Research Team

Company 3

| Aptiv |

Description |

| Company Introduction |

Founded in 1994 and headquartered in Ireland, Aptiv is a leading global supplier of automotive electronics and autonomous driving technologies. The company focuses on intelligent mobility solutions, providing autonomous driving systems, vehicle connectivity technologies, and high-performance electrical architectures to support automakers in transitioning from traditional vehicles to intelligent connected vehicles. Aptiv has accumulated extensive experience in sensor fusion, environmental perception, decision-making and planning, and safety redundancy technologies, and collaborates with global mobility platforms to drive the commercialization of autonomous driving technology and the development of an intelligent transportation ecosystem. |

| Product Introduction |

Aptiv’s autonomous ride-hailing service centers on its Robotaxi platform, developed in partnership with other companies. It has previously partnered with Lyft for commercial operations in Las Vegas, USA. Vehicles utilize high-precision sensors, LiDAR, cameras, and AI driving algorithms to achieve autonomous navigation, obstacle avoidance, and safe driving. Passengers can book rides via a mobile application without driver intervention. The platform supports daily commutes, airport transfers, and short-distance travel. Aptiv’s Robotaxi employs multi-layered safety mechanisms and a remote monitoring system, demonstrating the mature deployment capabilities of autonomous driving in the ride-hailing sector. |

Source: Third-party data, QYResearch Research Team

3 Autonomous Ride-hailing Vehicles Industry Chain Analysis

| Industry Chain |

Description |

| Upstream |

The upstream of autonomous ride-hailing services primarily includes core technology suppliers, companies developing perception and decision-making systems, and key component manufacturers. In terms of core technologies, upstream companies provide autonomous driving algorithms, AI perception systems, high-definition maps, and positioning services—the foundation for autonomous driving. Component manufacturers of sensors, cameras, LiDAR, and onboard computing platforms provide hardware support, ensuring high accuracy and reliability in information collection and processing. Furthermore, the upstream also involves operating systems, vehicle-to-everything (V2X) communication modules, and cloud data processing service providers. These companies constitute the technological ecosystem of autonomous ride-hailing services, providing solid technical support for downstream vehicle manufacturing and operation. |

| Midstream |

The midstream segment mainly includes autonomous vehicle manufacturers, system integrators, and ride-hailing platform developers. Vehicle manufacturers design and assemble autonomous vehicles based on upstream technologies and components, while simultaneously conducting safety testing and performance optimization. System integrators are responsible for efficiently integrating perception, decision-making, control systems, and communication modules into the vehicle, forming a commercially viable autonomous driving solution. Meanwhile, the midstream also includes ride-hailing platform development and maintenance companies. These companies provide functions such as scheduling algorithms, user-end applications, operational data management, and payment system interfaces, enabling efficient connections between vehicles, drivers, and passengers. They are key hubs directly connecting upstream and downstream technologies with downstream operations. |

| Downstream |

The downstream segment mainly involves the operation and service of autonomous ride-hailing vehicles, including ride-hailing platforms, leasing companies, enterprise-level mobility solution providers, and passenger-side user experience. Ride-hailing platforms are responsible for vehicle dispatching, order management, route planning, and user services, ensuring that autonomous vehicles can complete travel tasks efficiently and safely. Leasing companies or fleet management organizations provide vehicle maintenance, insurance, and charging or refueling services to ensure operational continuity. Enterprise clients and urban mobility solutions are also gradually becoming a focus of the downstream, providing customized, contactless, and intelligent travel experiences through autonomous ride-hailing vehicles. The service quality, user experience, and operational efficiency of the downstream ultimately determine the market acceptance and commercial value of autonomous ride-hailing vehicles, representing the direct user-facing aspect of the industry chain. |

Source: Third-party data, QYResearch Research Team

4 Autonomous Ride-hailing Vehicles Industry Development Trends, Opportunities, Obstacles and Industry Barriers

Development Trends:

1. Continuous Technological Upgrades. Global autonomous ride-hailing services are undergoing rapid technological iteration. Perception algorithms, LiDAR, high-definition maps, and AI decision-making systems are constantly being optimized, significantly improving vehicle safety and stability. Companies are conducting field tests in different cities and road conditions, driving the transition from L2/L3 autonomous driving to L4 fully driverless operation. Technological maturity is becoming a core indicator for future commercialization.

2. Diversified Business Models. With technological maturity and policy support, autonomous ride-hailing services are exploring various business models, including on-demand transportation, enterprise-level pick-up and drop-off services, shared mobility, and last-mile delivery. Operating platforms optimize resources through intelligent scheduling, data analysis, and dynamic pricing, forming a more efficient and flexible travel service system than traditional ride-hailing services.

3. Rapid Global Market Deployment. Countries worldwide are accelerating their deployment in the autonomous ride-hailing sector. North America and Europe are focusing on technology research and development and regulatory implementation, while the Asian market is leading in large-scale operations and urban applications. Multinational corporations are promoting unified technical standards and international operations through pilot cities, partnerships, and industry alliances, laying the foundation for global market development.

Development Opportunities:

1. Reduced Travel Costs: Autonomous driving technology can significantly reduce reliance on human drivers, lowering operating costs. Simultaneously, autonomous vehicles can optimize routes and energy management, improving vehicle utilization and making travel services more economical and accessible, creating dual value for both operating companies and users.

2. Promoted Smart City Development: Autonomous ride-hailing services can deeply integrate with smart transportation, vehicle-road cooperative systems, and urban big data platforms, improving traffic congestion, reducing accident rates and carbon emissions, and contributing to the intelligent and green development of cities. This also presents strategic opportunities for governments and enterprises to upgrade urban management and infrastructure.

3. Fostered Emerging Industry Development: The development of autonomous ride-hailing services drives rapid growth in upstream technology industries such as sensors, artificial intelligence, cloud computing, and vehicle networking. It also creates new jobs and business opportunities in areas such as unmanned vehicle operation management, data analysis, and maintenance services, forming a broad industrial chain economic effect.

Hindering Factors:

1. Lagging Regulations and Policies. Globally, the legal framework for autonomous ride-hailing services remains incomplete, including aspects such as road driving standards, liability determination, data privacy, and safety supervision. These policy lags limit the rapid deployment of the technology, and companies face compliance costs and operational uncertainties in different countries and regions.

2. Technology Safety and Trust Issues. The reliability of autonomous vehicles in complex road conditions, extreme weather, or emergencies remains controversial. System vulnerabilities and perception misjudgments may lead to traffic accident risks. Insufficient trust from users and the public in driverless cars is a significant obstacle to industry promotion and large-scale application.

3. High Cost Investment Pressure. Developing autonomous vehicles, deploying fleets, building charging and maintenance facilities, and conducting large-scale testing all require substantial financial investment. For startups and SMEs, financial pressure may limit technological innovation and market expansion, potentially leading to further industry concentration.

Barriers:

1. High Technological Barriers: Autonomous ride-hailing involves core technologies in multiple fields, including artificial intelligence, machine vision, deep learning, sensor fusion, and vehicle networking. The R&D cycle is long and difficult to replicate. Leading companies have established significant competitive barriers through technological accumulation and patent portfolios, making it difficult for new entrants to catch up in the short term.

2. Data Resource Barriers: Large-scale autonomous driving training relies on massive amounts of high-quality traffic data, including road condition information, driving behavior, and user travel habits. Companies possessing abundant data can optimize algorithms and operational strategies, forming strong data barriers that restrict other companies from entering the market.

3. Ecosystem and Platform Advantages: Successful autonomous ride-hailing relies not only on vehicle technology but also on mature dispatch systems, user-end applications, payment systems, and operational management capabilities. The formation of a complete industrial ecosystem and platform network effects gives leading companies a significant advantage in market share and user stickiness, creating new industry barriers.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading Global market research and consulting company. With over 16 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are Globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp