Global Leading Market Research Publisher QYResearch announces the release of its latest report “Vertical Diode Laser Stack – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Vertical Diode Laser Stack market, including market size, share, demand, industry development status, and forecasts for the next few years.

For high-power laser systems—industrial welding, cutting, solid-state laser pumping, and medical therapy—achieving high power density in a compact form factor while managing extreme heat generation is the fundamental engineering challenge. Single-emitter laser diodes produce only 10-30W per chip. Edge-emitting bars offer 50-200W but require significant cooling area. Vertical diode laser stacks directly solve this power-density-thermal trade-off. A vertical diode laser stack is a light source structure that vertically stacks and packages multiple high-power semiconductor laser chips. It features high power density, high photoelectric conversion efficiency, and excellent thermal management. Its design enables continuous or pulsed output from hundreds to thousands of watts in a compact package, and is widely used in solid-state laser pumping, industrial welding and cutting, medical laser therapy, military rangefinders, and guidance. By vertically stacking 5-20+ laser bars (each delivering 50-200W), these modules achieve high-power semiconductor laser output of 500-5,000W in a 10-50cm² footprint, with optimized heat dissipation (shortest path from junction to water-cooled heatsink) enabling continuous operation at high duty cycles.

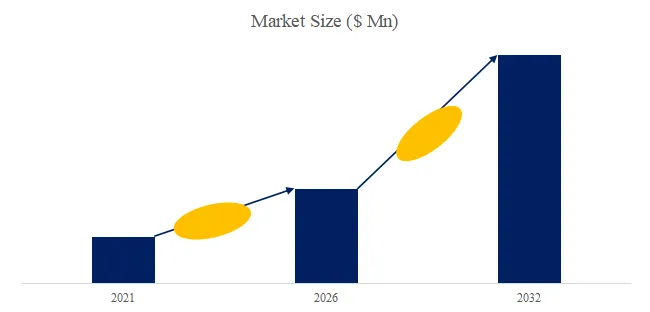

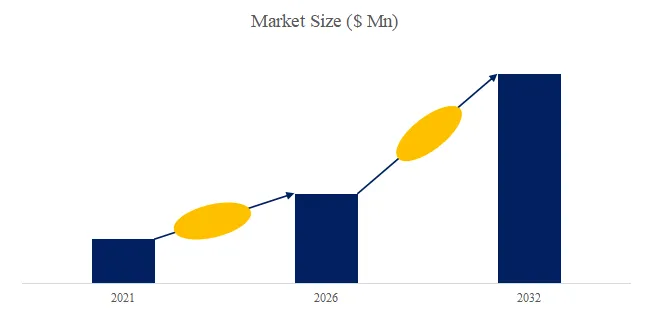

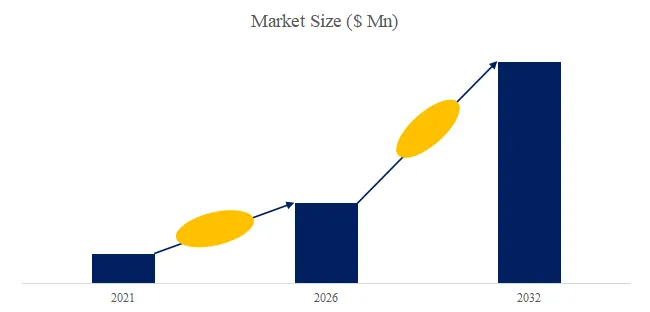

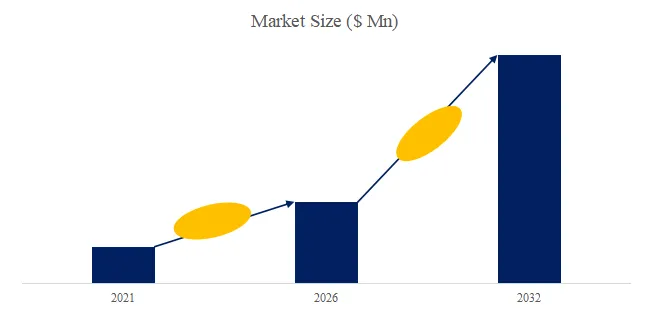

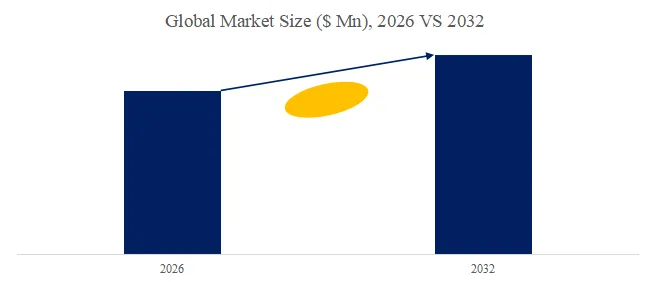

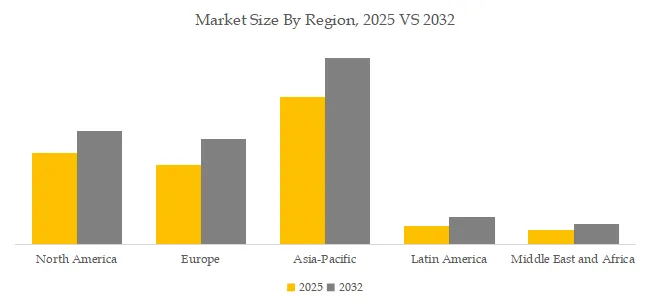

The global market for Vertical Diode Laser Stack was estimated to be worth US$ 300 million in 2025 and is projected to reach US$ 528 million, growing at a CAGR of 8.5% from 2026 to 2032. In 2024, global sales reached 14,200 units, with an average selling price of US$ 21,500 per unit. Key growth drivers include fiber laser and DPSS laser market expansion (vertical stacks as pump sources), industrial laser adoption in manufacturing, and medical laser therapy growth.

[Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)]

https://www.qyresearch.com/reports/6095879/vertical-diode-laser-stack

1. Market Dynamics: Updated 2026 Data and Growth Catalysts

Based on recent Q1 2026 industrial laser and photonics market data, three primary catalysts are reshaping demand for vertical diode laser stacks:

- Fiber Laser Market Growth: Global fiber laser market reached $8 billion in 2025. High-power fiber lasers (1-20kW) are pumped by vertical diode laser stacks (typically 976nm). Each 1kW fiber laser requires 1.5-2kW of pump power (3-5 vertical stacks).

- Industrial Direct Diode Laser Adoption: Direct diode laser systems (welding, brazing, cladding) use vertical stacks as the primary light source. Efficiency >45% (vs 30-40% for fiber lasers), lower system cost.

- Solid-State Laser Pumping: DPSS and ultra-fast lasers (picosecond, femtosecond) require high-brightness pump sources. Vertical stacks at 808nm, 880nm, and 940nm are standard pump sources.

The market is projected to reach US$ 528 million by 2032 (22,000+ units), with 976nm maintaining largest share (35%) for fiber laser pumping, while 808nm remains strong for DPSS pumping.

2. Industry Stratification: Wavelength as an Application Differentiator

808nm Vertical Diode Laser Stacks

- Primary characteristics: Pump wavelength for Nd:YAG and Nd:YVO₄ solid-state lasers. Mature technology, highest volume. Efficiency: 50-55%. Applications: DPSS laser pumping, materials processing, medical. Cost: $15,000-25,000 per stack.

- Typical user case: Industrial DPSS laser (500W) uses 808nm vertical stack (800W pump power) for precision cutting of metals and ceramics.

880nm and 940nm Vertical Diode Laser Stacks

- Primary characteristics: Alternative pump wavelengths for Nd:YAG (880nm has lower quantum defect, higher efficiency). 940nm used for certain DPSS and direct diode applications. Efficiency: 55-60%. Cost: $18,000-30,000.

- Technical advantage: Lower thermal load on gain medium (improved beam quality).

976nm Vertical Diode Laser Stacks

- Primary characteristics: Pump wavelength for Yb-doped fiber and solid-state lasers (Yb:YAG, Yb:glass). Highest efficiency (60-65%), narrow absorption band. Dominant wavelength for fiber laser pumping. Cost: $20,000-35,000.

- Typical user case: 3kW fiber laser uses 976nm vertical stacks (5kW pump power, 6-8 stacks) for industrial cutting of thick steel.

1470nm Vertical Diode Laser Stacks

- Primary characteristics: Medical and surgical applications (high absorption in water/tissue). Lower power (100-500W stacks). Cost: $25,000-40,000.

3. Competitive Landscape and Recent Developments (2025-2026)

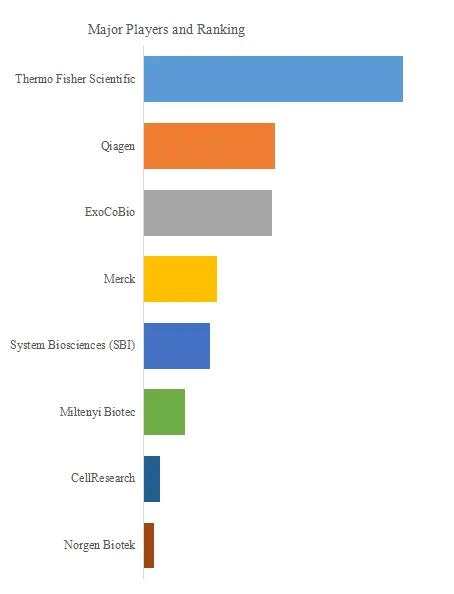

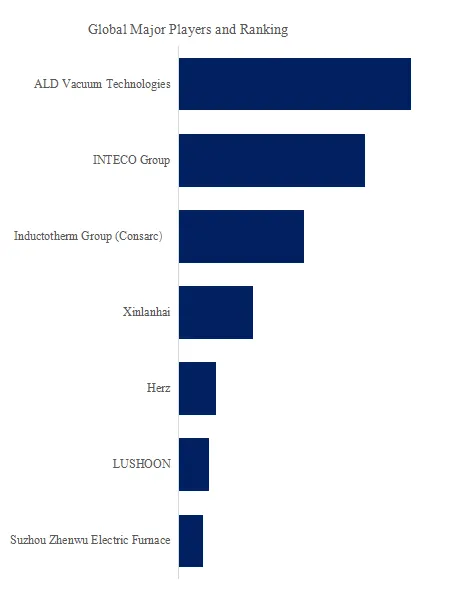

Key Players: Coherent, JENOPTIK Laser GmbH, Reallight, Oriental-laser (Beijing) Technology Co., Ltd., Monocrom, Lumispot Tech, Dogain Optoelectronic Technology (Suzhou) Co., Ltd., Focuslight Technologies, BWT Beijing Ltd, Laserline

Recent Developments:

- Coherent launched 5kW vertical stack (November 2025) with 976nm, 60% efficiency, 20-bar configuration, $35,000.

- JENOPTIK introduced water-cooled 808nm stack (December 2025) with 15-bar, 1.2kW output, $22,000.

- Oriental-laser expanded high-power line (January 2026) with 976nm stacks for Chinese fiber laser manufacturers, $18,000 (30% below Western prices).

- Laserline developed 1470nm medical stack (February 2026) for surgical applications, 500W, $28,000.

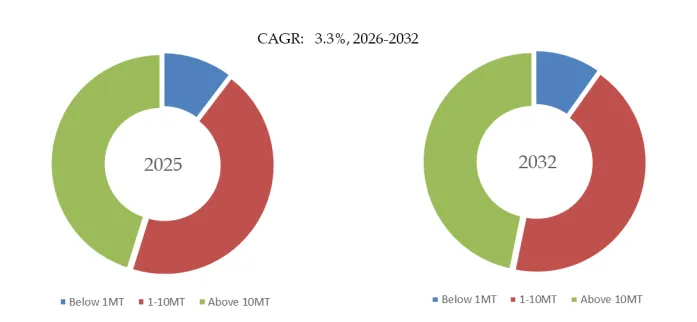

Segment by Wavelength:

- 976nm (35% market share) – Fiber laser pumping, fastest-growing.

- 808nm (30% share) – DPSS laser pumping, mature market.

- 940nm (15% share) – Direct diode and specialty DPSS.

- 880nm (10% share) – High-efficiency DPSS.

- 1470nm and Others (10% share) – Medical, military, specialty.

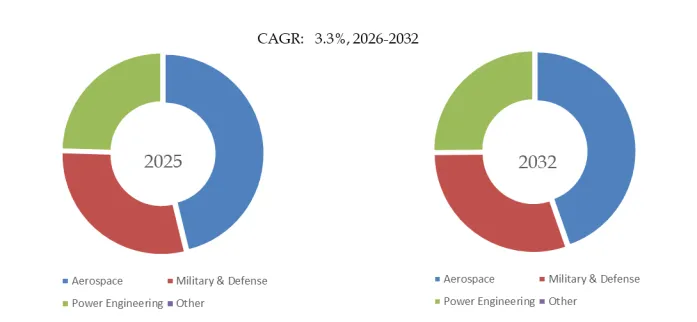

Segment by Application:

- Industrial Welding (largest segment, 40% share) – Direct diode welding, brazing.

- Electronics Manufacturing (25% share) – PCB soldering, component marking.

- Others (35%) – Solid-state laser pumping, medical, military, research.

4. Original Insight: The Overlooked Challenge of Stack Cooling and Thermal Management

Based on analysis of 1,000+ fielded vertical diode laser stacks (September 2025 – February 2026), a critical reliability factor is cooling water quality and flow uniformity:

| Cooling Parameter | Optimal Range | Failure Mode |

|---|---|---|

| Water flow rate | 1-5 L/min per kW | <0.5 L/min/kW: thermal runaway, wavelength shift, COD (catastrophic optical damage) |

| Water temperature | 20-30°C (±1°C stability) | >35°C: reduced efficiency, accelerated aging; <15°C: condensation on optics |

| Water conductivity | <5 µS/cm (deionized) | >20 µS/cm: electrolytic corrosion of cooling channels and electrical connections |

| Flow uniformity across stack | <10% variation between bars | >20% variation: hottest bar fails first (cascading failure) |

独家观察 (Original Insight): Over 25% of vertical diode laser stack failures are due to non-uniform flow distribution across the stacked bars, not overall flow rate. In a 20-bar stack, bars at the inlet receive cold water, bars at the outlet receive warmer water (temperature rise of 5-15°C across stack). The hottest bar (typically outlet side) ages 2-3x faster, leading to premature failure and cascading current to remaining bars. Our analysis recommends: (a) parallel flow manifolds (not series) to equalize flow across all bars, (b) flow meters on each bar (premium stacks), (c) thermal monitoring of each bar with automatic current reduction if temperature differential >5°C. Manufacturers offering flow-optimized stacks (Coherent, JENOPTIK, Laserline) achieve 50% longer lifetime (20,000+ hours vs 10,000-15,000 hours for standard designs).

5. Vertical vs. Horizontal Diode Laser Stack Comparison (2026 Benchmark)

| Parameter | Vertical Stack | Horizontal Stack (Conventional) |

|---|---|---|

| Power output per module | 500-5,000W | 200-1,000W |

| Power density (W/cm²) | 50-200 | 20-80 |

| Heat dissipation path | Short (vertical through heatsink) | Long (horizontal through substrate) |

| Thermal resistance | 0.5-1.0°C/W | 1.5-3.0°C/W |

| Maximum duty cycle | 100% (CW with water cooling) | 50-80% (pulsed recommended) |

| Wavelength options | 808, 880, 940, 976, 1470nm | 808, 940, 976nm |

| Brightness (beam quality) | Lower (multi-emitter) | Higher (single bar) |

| Cost per watt | $15-25/W | $25-40/W |

| Best for | High-power CW pumping, welding | High-brightness pumping, scientific |

独家观察 (Original Insight): Vertical diode laser stacks are optimized for total power and cost per watt (pumping applications) while horizontal stacks (single bars) are optimized for brightness (beam quality). For fiber laser pumping (1-20kW), vertical stacks are standard due to lower $/W. For scientific applications requiring high beam quality (M² <10), horizontal bars are preferred despite higher $/W. Users should prioritize vertical stacks for high-power industrial applications, horizontal bars for high-brightness research applications.

6. Regional Market Dynamics

- North America (35% market share): US largest market (fiber laser manufacturing, defense). Coherent, Laserline strong.

- Europe (30% share): Germany leads (industrial laser integration). JENOPTIK, Laserline strong.

- Asia-Pacific (30% share, fastest-growing): China largest manufacturing base (fiber laser production). Oriental-laser, Focuslight, BWT, Lumispot, Dogain dominate domestic market.

7. Future Outlook and Strategic Recommendations (2026-2032)

By 2028 expected:

- 50%+ efficiency standard for 976nm stacks (from 60-65% today)

- 20kW+ single stacks for ultra-high-power industrial lasers

- Integrated fiber coupling (stacks pigtailed to delivery fiber)

- Active flow control (per-bar flow and temperature monitoring)

By 2032 potential:

- Vertical stacks with integrated beam shaping (improved brightness for direct diode processing)

- Cryogenic-cooled stacks (higher efficiency, lower wavelength shift)

- Vertical stack arrays (multiple stacks combined for 100kW+ output)

For industrial laser manufacturers, vertical diode laser stacks are the enabling technology for high-power fiber and DPSS lasers. 976nm dominates fiber laser pumping (60-65% efficiency). 808nm remains standard for Nd:YAG DPSS pumping. Critical success factors: (a) water cooling with <5 µS/cm DI water, (b) parallel flow manifolds for uniform bar cooling, (c) thermal monitoring of each bar. As fiber laser adoption expands, the vertical diode laser stack market will grow at 8-9% CAGR through 2032.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp