Hospital UPS Market Summary

Hospital UPS systems are uninterruptible power supplies deployed in healthcare facilities to provide continuous, regulated, low-noise power for critical loads during utility disturbances and outages. They protect sensitive medical devices and hospital IT from voltage dips, surges, harmonics, and transfer interruptions, reducing risk of device resets and workflow disruption. Typical configurations include online double-conversion UPS, modular redundant UPS, and distributed UPS for equipment rooms. Key requirements include high reliability, fast or zero transfer, low leakage current, battery safety, and monitoring for preventive maintenance in clinical environments.

The industrial chain of Hospital UPS includes upstream power semiconductors, capacitors, inductors, transformers, batteries, chargers, BMS/PCM parts, EMI filters, sensors, microcontrollers, communication modules, thermal materials, and metal enclosures. Midstream covers UPS topology and control design, firmware, insulation and grounding, assembly, burn-in, battery integration, and safety/EMC compliance testing. Downstream users include hospitals, clinics, labs, imaging centers, operating rooms, ICU wards, and data closets needing backup runtime and power quality. Supporting services include sizing, installation, commissioning, monitoring integration, preventive maintenance, and battery replacement.

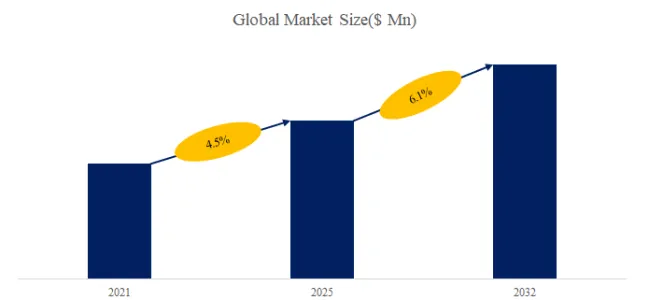

In 2025, global Hospital UPS production reached approximately 3,400 k units,with an average global market price of around US$ 560 per unit, and a gross profit margin of approximately 20%-40%. According to the new market research report “Global Hospital UPS Market Report 2026-2032”, published by QYResearch, the global Hospital UPS market size is projected to reach USD 2.97 billion by 2032, at a CAGR of 6.1% during the forecast period.

Global Hospital UPS Market Size (US$ Million), 2020-2031

Above data is based on report from QYResearch: Global Hospital UPS Market Report 2021-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

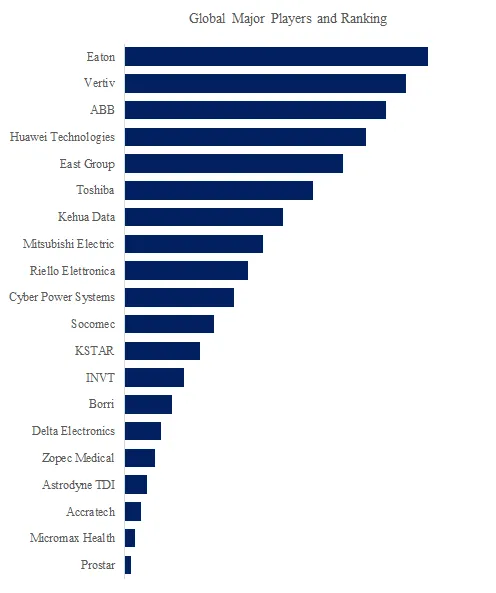

Global Hospital UPS Top 5 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Hospital UPS Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

According to QYResearch Top Players Research Center, the global key manufacturers of Hospital UPS include Eaton, Vertiv, ABB, Huawei Technologies, East Group, Toshiba, Kehua Data, Mitsubishi Electric, Riello Elettronica, Cyber Power Systems, etc. In 2025, the global top five players had a share approximately 41.0% in terms of revenue.

Hospital UPS Market Trends

1. Increasing adoption of smart and IoT-enabled UPS systems in hospitals

Hospital UPS systems are evolving toward intelligent, connected solutions with real-time monitoring and remote management capabilities. Hospitals are increasingly deploying smart UPS systems equipped with IoT-based monitoring, predictive diagnostics, and remote control features. These systems allow facility managers to track power conditions, battery health, and load performance in real time, improving operational reliability and reducing downtime risks. Integration with hospital IT systems and building management platforms further enhances energy efficiency and enables proactive maintenance. This shift reflects the broader digital transformation of healthcare infrastructure, where uninterrupted power is not only required but must also be actively managed. As hospitals become more data-driven, intelligent UPS solutions are becoming essential to ensure continuous operation of critical medical equipment and IT systems.

2. Transition toward lithium-ion batteries and high-efficiency UPS technologies

Hospitals are increasingly adopting advanced battery technologies and energy-efficient UPS systems to improve performance and lifecycle cost. Traditional lead-acid battery systems are gradually being replaced by lithium-ion alternatives due to their longer lifespan, smaller footprint, and faster charging capabilities. These advantages are particularly valuable in hospital environments where space is limited and reliability is critical. At the same time, high-efficiency UPS architectures are being developed to reduce energy losses and operating costs. Hospitals are also exploring hybrid UPS solutions integrated with renewable energy sources to enhance sustainability.

3. Rising demand for high-power-density and modular UPS solutions

Hospitals are increasingly deploying modular and scalable UPS systems to support expanding and complex medical infrastructures. Modern hospitals are becoming more technologically advanced, incorporating imaging systems, surgical equipment, and digital healthcare platforms that require stable and scalable power support. This has led to growing demand for high-power-density UPS systems that can deliver reliable power in compact designs. Modular UPS architectures are also gaining popularity, allowing hospitals to scale capacity as demand grows without significant infrastructure changes.

Hospital UPS Market Driving Factors and Opportunities

1. Expansion of healthcare infrastructure and hospital facilities

Rapid growth in healthcare infrastructure globally is a key driver for hospital UPS system demand. The increasing number of hospitals, clinics, and diagnostic centers—especially in emerging markets—is driving strong demand for reliable backup power solutions. Governments and private investors are expanding healthcare capacity to meet rising population needs and improve service accessibility. Every new or upgraded facility requires dependable UPS systems to ensure uninterrupted operation of medical devices and critical services. This ongoing infrastructure expansion creates a stable and long-term demand base for hospital-grade UPS systems across regions.

2. Critical need for uninterrupted power in life-saving medical applications

The requirement for continuous power supply to essential medical equipment is a fundamental market driver. Hospitals rely heavily on devices such as ventilators, imaging systems, surgical tools, and life-support equipment, all of which require uninterrupted power. Even a brief outage can compromise patient safety and clinical outcomes. Increasing dependence on advanced medical technologies and digital healthcare systems further amplifies this requirement. As a result, hospitals prioritize investment in reliable UPS systems to ensure zero interruption in critical operations, making power continuity a non-negotiable requirement in healthcare environments.

3. Growing prevalence of chronic diseases and aging population

Rising healthcare demand driven by demographic trends creates significant opportunities for UPS system adoption. The increasing prevalence of chronic diseases and the global aging population are driving higher demand for healthcare services and advanced medical equipment. These trends lead to more complex and technology-intensive hospital operations, which in turn require stable and continuous power supply. As healthcare systems expand to accommodate long-term patient care and specialized treatments, the need for reliable UPS solutions continues to grow.

About The Authors

| Zhangyu – Lead Author |

| Email:zhangyu@qyresearch.com |

About QYResearch

QYResearch founded in California, USA in 2007. It is a leading Global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are Globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp