Global Leading Market Research Publisher QYResearch announces the release of its latest report “Thunderbolt 5 Technology – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Thunderbolt 5 Technology market, including market size, share, demand, industry development status, and forecasts for the next few years.

For PC manufacturers, peripheral vendors, content creators, and IT professionals, the persistent challenge remains consistent: moving massive amounts of data (8K video, large AI models, complex 3D renders) between devices quickly while supporting multiple high-resolution displays and charging through a single port. Thunderbolt 5, the latest iteration of Intel’s high-speed connectivity technology, delivers a significant leap forward in data transfer speeds, bandwidth, and versatility. With up to 80 Gbps of bi-directional bandwidth (3x Thunderbolt 4′s 40 Gbps) and support for up to 120 Gbps in specific configurations (Bandwidth Boost mode for display-heavy workloads), Thunderbolt 5 enables new use cases. The market ecosystem includes cables (active and passive), docks (multi-port expansion), laptops (integrated controllers), and others (eGFX enclosures, storage devices, monitors). Applications span personal use (gaming, content creation, prosumer) and commercial use (enterprise IT, creative studios, engineering workstations).

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5646554/thunderbolt-5-technology

1. Market Size & Growth Trajectory (2026–2032)

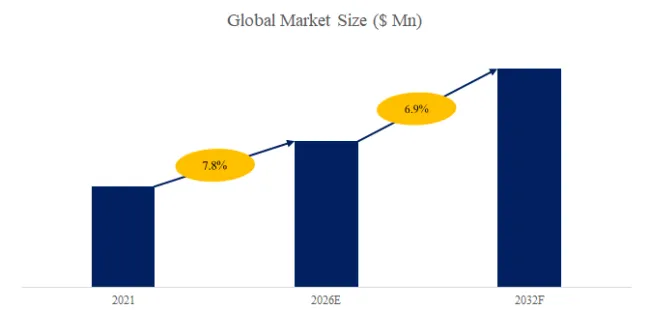

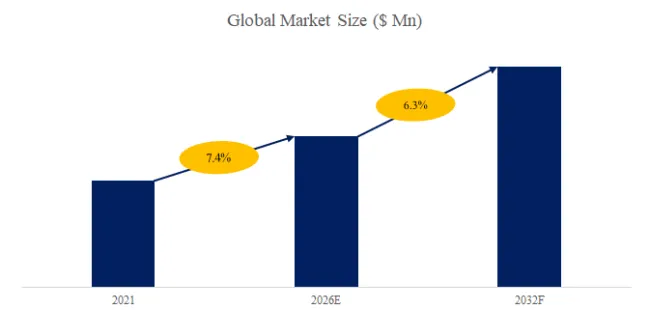

The global market for Thunderbolt 5 Technology was estimated to be worth US$ 180 million in 2025 (initial ramp with Intel Barlow Ridge controllers) and is projected to reach US$ 2.1 billion by 2032, growing at a CAGR of 42.0% from 2026 to 2032. In 2024, the first Thunderbolt 5 products launched (Razer Blade 18 laptop, MSI Titan 18 HX, various docks and cables). Unit volumes are projected to reach 50 million Thunderbolt 5-enabled devices by 2028 (laptops, desktops, peripherals).

Exclusive industry observation: The Thunderbolt 5 market is experiencing explosive early-stage growth (42% CAGR) driven by three transformative factors: (1) AI PC and content creation demand (large model transfers, 8K video editing requiring >40 Gbps); (2) multi-display productivity (dual 8K or triple 4K at 144Hz+); (3) external graphics (eGFX) and storage (eGFX over Thunderbolt 5 achieving 90-95% of native PCIe performance vs. 60-70% for Thunderbolt 4).

2. Industry Segmentation & Key Players

The market is segmented by product type into Cables, Docks, Laptops, and Others (eGFX enclosures, storage devices, monitors, motherboards), and by application into Personal Use and Commercial Use.

By Product Type – Ecosystem Components and Adoption Timeline

| Product Type | Key Features | 2025 Market Share | First Availability | Price Range | Key Vendors |

|---|---|---|---|---|---|

| Cables | Active (40Gbps+ requires active electronics), passive (shorter lengths), 0.2-2m | 15% | 2024 | $30-80 | CableMatters (Lintes), Arin Electronics, Belkin, CalDigit |

| Docks | Multi-port expansion (DP2.1, USB4, Ethernet, audio, SD), 60-140W charging | 35% | 2024-2025 | $250-500 | CalDigit, Razer, Hyper, ACASIS, OWC, Kensington |

| Laptops | Integrated JHL9580/JHL9540 controllers (Intel Barlow Ridge), PCIe 4.0 x4 | 40% | 2024 (Razer, MSI), 2025 (Dell, Lenovo, HP, Apple) | $2,000+ (early), $1,000+ (2026) | Razer, MSI, Dell, Lenovo, HP, Apple (expected 2026) |

| Others (eGFX, storage, monitors) | External GPU enclosures (PCIe 4.0 x4), NVMe RAID, 8K displays | 10% | 2025-2026 | $300-800 (eGFX), $200-500 (storage) | Razer Core, Sonnet, OWC, LaCie, Samsung, LG, Dell |

Industry layer analysis – Discrete vs. Process Analogies: Personal Use (≈55% of Thunderbolt 5 revenue, analogous to “consumer high-end” – gaming, content creation, prosumer) dominates initial adoption, driven by gamers and video editors. Commercial Use (≈45%, analogous to “enterprise IT” – professional workstations, creative studios, engineering) will grow as Dell, Lenovo, HP integrate Thunderbolt 5 into business laptops (2025-2026).

Key Suppliers (2025)

Prominent Thunderbolt 5 ecosystem participants include:

- Laptops: Razer (Blade 18, first Thunderbolt 5 laptop, Q4 2024), MSI (Titan 18 HX), Dell (Alienware, Precision 2025), Lenovo (Legion, ThinkPad 2025), HP (ZBook, Spectre 2025), Apple (MacBook Pro expected 2026 with Thunderbolt 5)

- Docks: CalDigit (TS5), Razer (Thunderbolt 5 Dock), Hyper (HyperDrive), ACASIS (TB5 Dock), OWC, Kensington, Startech

- Cables: Lintes Technology (CableMatters), Dongguan Arin Electronics Technology (active cables), Belkin, CalDigit, Apple

- Controllers (Intel, not directly in market segmentation but enabling): Intel (JHL9580 for hosts, JHL9540 for docks/devices, Barlow Ridge family)

Exclusive observation: Intel controls the Thunderbolt 5 ecosystem through controller supply and certification (Thunderbolt 5 certification program launched 2024). Key controller specs: JHL9580 (host, 80Gbps bi-directional, PCIe 4.0 x4, DP 2.1), JHL9540 (peripheral/dock, similar). Competition from USB4 v2.0 (also 80Gbps) but Thunderbolt maintains advantages in guaranteed performance, daisy-chaining (up to 6 devices), and PCIe tunneling efficiency.

3. Technology Trends, Policy Drivers & User Cases (Last 6 Months)

Recent technology advancements (Q3 2025–Q1 2026):

- Bandwidth Boost mode – Dynamic reallocation: up to 120 Gbps for video (display) + 40 Gbps for data, enabling dual 8K (7680×4320) at 120Hz or triple 4K at 144Hz with single cable.

- DisplayPort 2.1 (UHBR20) – Thunderbolt 5 incorporates DP 2.1 (80 Gbps), supporting 8K @ 120Hz, 10K, 16K displays without compression (DSC optional).

- PCIe 4.0 x4 – 32 Gbps PCIe bandwidth (vs. PCIe 3.0 x4 16 Gbps on Thunderbolt 4), enabling eGFX at 90-95% of native performance (vs. 60-70% for Thunderbolt 4).

- Longer active cables – Active optical cables (AOC) and active copper cables achieving 2m at full 80 Gbps (passive limited to 0.8-1m), with 5-10m optical cables in development (Arin Electronics, Corning).

- Power delivery (PD) 3.1 – 140W (28V/5A) charging over Thunderbolt 5 (vs. 100W Thunderbolt 4), supporting gaming laptops and mobile workstations.

Policy & regulatory updates (last 6 months):

- USB-IF USB4 v2.0 certification (October 2025) – 80 Gbps USB4 v2.0 certified products entering market, but Thunderbolt 5 maintains premium positioning (guaranteed performance, daisy-chaining).

- EU Common Charging Directive expansion (December 2025) – Laptops required to support USB-C charging (Thunderbolt 5 ports qualify), accelerating Thunderbolt 5 adoption in commercial laptops.

- China’s “New Generation Computing” initiative (November 2025) – Domestic laptop OEMs (Lenovo, Xiaomi, Huawei) encouraged to adopt Thunderbolt 5/USB4 v2.0 for high-end models.

Typical user case – Personal Use (Content Creator/Editor):

A professional video editor upgraded from Thunderbolt 4 to Thunderbolt 5 (Razer Blade 18 laptop, CalDigit TS5 dock). Workflow: 8K RAW video (60 minutes, 1.5TB) transferred from external NVMe RAID (Thunderbolt 5) to laptop SSD: 80 Gbps = 10 GB/s theoretical, actual 7-8 GB/s, transfer time reduced from 4 minutes (Thunderbolt 4, 3 GB/s) to 1.5 minutes. Simultaneously driving dual 8K monitors (Dell UP3218K) at 60Hz via single dock cable. Outcome: 40% reduction in project turnaround time.

Typical user case – Commercial Use (Engineering/Architecture):

An architecture firm replaced desktop workstations with Thunderbolt 5 laptops (Dell Precision 2025) + eGFX enclosures (Razer Core X with RTX 6000 Ada). Benefits: Single-cable docking (dual 5K monitors, 10GbE, audio, charging), eGFX providing 95% of desktop GPU performance (vs. 65% with Thunderbolt 4), and hot-desking with data persistence. Firm reduced hardware costs 30% (laptops + eGFX vs. desktops + laptops).

Technical challenge addressed – Signal integrity at 80 Gbps (40 GT/s per lane) over copper cables. Thunderbolt 4 (40 Gbps, 20 GT/s) used passive cables up to 0.8m. Thunderbolt 5 requires active electronics (retimers, redrivers) in cables longer than 0.3-0.5m. Active cables include: (1) active copper (retimer ICs, up to 1-1.5m), (2) active optical (optical transceivers, up to 10-50m, higher cost). Lintes Technology (CableMatters) and Dongguan Arin Electronics lead active cable manufacturing. Cost premium: active copper 2-3x passive, active optical 5-10x.

4. Future Outlook & Strategic Implications (2026–2032)

Demand will be driven by seven primary forces: (1) 8K/16K video and display ecosystem (cameras, monitors, GPUs requiring >40 Gbps); (2) AI PC content generation (large model checkpoint files 10-100GB, faster transfer); (3) external GPU (eGFX) 2.0 (PCIe 4.0 x4 enabling near-native performance); (4) commercial laptop standardization (Dell, Lenovo, HP integrating into business lines 2025-2026); (5) Apple transition (MacBook Pro expected 2026, catalyzing ecosystem); (6) single-cable docking for dual 8K/triple 4K workflows; (7) gaming laptop differentiation (Razer, MSI, Alienware flagship models).

Strategic recommendation for ecosystem participants: Laptop OEMs – integrate Thunderbolt 5 in premium models (2025-2026) as key differentiator. Dock vendors – prioritize dual 8K support, 140W charging, 10GbE. Cable vendors – scale active cable production (copper and optical) to meet demand. Intel – reduce controller costs (JHL9580) to drive adoption beyond $2,000 laptops. Competition from USB4 v2.0 (80 Gbps, potentially lower cost) may pressure Thunderbolt 5 pricing, but Thunderbolt’s guaranteed performance, certification, and ecosystem integration maintain premium positioning.

Exclusive forecast: The Thunderbolt 5 market will reach $2.1 billion by 2032, with laptops largest segment (40-45% of revenue), followed by docks (30-35%), cables (10-15%), and others (10-15%). Personal use will maintain 55-60% share (gaming, content creation), but commercial use will grow faster (45-50% CAGR, reaching 45% by 2030) as enterprise IT adopts Thunderbolt 5 for creative and engineering workstations. Apple’s adoption (expected 2026 MacBook Pro, 2027 Mac Studio/Pro) will be the single largest catalyst, adding 10-15 million units annually and driving peripheral ecosystem growth. Intel will maintain controller monopoly (no third-party Thunderbolt 5 controllers expected until 2027-2028). Active cables will become standard for lengths >0.5m, with active copper dominating 0.5-2m and active optical for 2-50m (studio, data center). By 2030, Thunderbolt 5 will be standard on laptops >$1,500 (80% penetration) and premium docks (90%+), with Thunderbolt 6 (160 Gbps?) expected 2028-2030.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp

MT Ferrule, Global Market Size, Split by Product Segment

MT Ferrule, Global Market Size, Split by Product Segment