Introduction (Covering Core User Needs: Pain Points & Solutions):

Global Leading Market Research Publisher QYResearch announces the release of its latest report “LED Overcurrent Protection Device – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global LED Overcurrent Protection Device market, including market size, share, demand, industry development status, and forecasts for the next few years.

For LED lighting manufacturers, driver designers, and system integrators, excessive current flow presents critical reliability challenges: thermal runaway (LED current increases with temperature, leading to catastrophic failure), voltage spikes from switching power supplies, and short-circuit conditions that can destroy entire lighting arrays. An LED overcurrent protection device is an electronic component or circuit designed to prevent damage to LED lighting systems by limiting excessive current flow. These devices detect abnormal current spikes and either limit, interrupt, or divert the current to protect the LEDs and associated circuitry. Common types include PTC thermistors, polymer resettable fuses, current-limiting ICs, and electronic circuit breakers. They are widely used in LED drivers, lighting fixtures, automotive LEDs, and signage systems. As LED lighting penetration increases (80%+ of new commercial and residential lighting) and applications demand higher reliability (automotive headlights, outdoor street lighting, industrial high-bay fixtures), LED overcurrent protection devices are transitioning from optional safety feature to mandatory design component.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)

https://www.qyresearch.com/reports/6094992/led-overcurrent-protection-device

1. Market Sizing & Growth Trajectory (With 2026–2032 Forecasts)

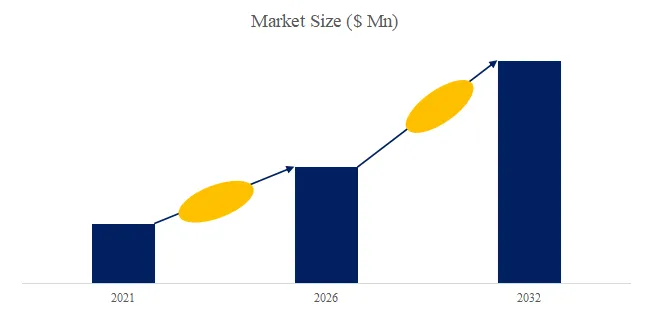

The global market for LED Overcurrent Protection Device was estimated to be worth US$660 million in 2025 and is projected to reach US$1,020 million by 2032, growing at a CAGR of 6.5% from 2026 to 2032. This steady growth is driven by three converging factors: (1) increasing LED adoption across lighting segments (general illumination, automotive, signage, backlighting), (2) rising demand for resettable protection (PTC thermistors, polymer fuses) over one-time fuses, and (3) stricter safety regulations for LED lighting systems (UL, IEC, EN). In 2024, global LED Overcurrent Protection Device production reached approximately 756 million units, with an average global market price of around US$0.82 per unit.

By mounting type, surface-mount devices (SMD) dominate with approximately 70% of unit volume (preferred for automated PCB assembly in LED drivers). Plug-in type accounts for 15% (through-hole, legacy designs), Din-rail mounting type for 15% (industrial lighting control panels).

2. Technology Deep-Dive: PTC Thermistors, Resettable Fuses, and Current-Limiting ICs

Technical nuances often overlooked:

- PTC thermistor (Positive Temperature Coefficient) resettable fuses: Resistance increases sharply with temperature. Under overcurrent, device self-heats, resistance rises (10× to 1,000×), limiting current. After fault removal and cooling, resistance returns to low state (resettable). Trip time: 0.1-10 seconds depending on overcurrent magnitude. Hold current: 50mA-5A typical. Voltage rating: 6-600V. Polymer PTCs (PPTC) vs. ceramic PTCs (CPTC): polymer cheaper, lower voltage; ceramic higher voltage, faster trip.

- Current-limiting ICs (integrated circuits): Active protection using sense FET (field-effect transistor) to monitor current. When overcurrent detected (threshold programmable 50mA-5A), IC shuts off output within 1-10 microseconds. Features: adjustable current limit, thermal shutdown, auto-retry or latch-off modes. Higher cost (US$0.50-2.00) than passive PTC (US$0.10-0.50), used in premium LED drivers and automotive applications.

Recent 6-month advances (October 2025 – March 2026):

- Littelfuse launched “PolySwitch LVR” – low-voltage PPTC resettable fuse (16-72V, 0.5-3A hold current), 30% smaller footprint than previous generation (0402 case size). AEC-Q200 qualified for automotive LED lighting (headlamps, DRLs, interior). Price US$0.15-0.35.

- Bourns introduced “MF-RHS Series” – high-temperature PPTC (125°C operating, vs. 85°C standard) for LED drivers in enclosed fixtures (street lighting, high-bay). Higher hold current stability at temperature (derating reduced from 50% to 30%). Price US$0.25-0.60.

- ON Semiconductor commercialized “NCP457″ – current-limiting IC with integrated 40mΩ power FET, programmable current limit (0.5-4A), 1.5µs response time. Soft-start and reverse current blocking. Automotive AEC-Q100 Grade 1 (-40°C to +125°C). Price US$0.80-1.50.

3. Industry Segmentation & Key Players

The LED Overcurrent Protection Device market is segmented as below:

By Mounting Type (PCB Integration):

- Plug-In Type (through-hole, axial leads) – Legacy designs, easier manual replacement (fuses). Larger footprint, higher assembly cost. Declining share. Price: US$0.10-0.50.

- Surface Mount Type (SMD, SMT) – Automated assembly, compact size (0402 to 1812 case sizes). Dominant for new LED driver designs. Price: US$0.10-0.80.

- Din Rail Mounting Type – Modular protection for industrial lighting control panels (multiple LED drivers). Higher current ratings (5-20A). Price: US$5-25 per module.

By Application (End-Use Sector):

- Electronics (LED drivers, LED bulbs, LED strips, signage, backlighting) – Largest segment at 60% of 2025 revenue. High volume, cost-sensitive. Surface-mount PPTC dominant.

- Power Industry (industrial lighting, street lighting, high-bay fixtures, outdoor lighting) – 20% share. Higher current ratings, wider temperature range, reliability focus.

- Communications (LED indicators in telecom equipment, data centers) – 10% share.

- Other (automotive, medical, aerospace) – 10% share, fastest-growing at 8.5% CAGR (automotive LED lighting).

Key Players (2026 Market Positioning):

Global Leaders: Littelfuse (USA), Bourns (USA), Eaton (USA), ON Semiconductor (USA), STMicroelectronics (Switzerland), Infineon Technologies (Germany), Analog Devices (USA), Murata (Japan), TI (Texas Instruments, USA), LED Overvoltage Protection Device (brand/supplier), JCET (China).

独家观察 (Exclusive Insight): The LED overcurrent protection device market displays a fragmented competitive landscape with distinct specialization. Passive protection specialists (Littelfuse, Bourns, Eaton, Murata) dominate PPTC and CPTC resettable fuses, leveraging materials science expertise (conductive polymer composites, ceramic formulations) and broad distribution (Mouser, DigiKey, Arrow). These players hold ≈50-55% of market value, primarily in SMD and plug-in segments. Active protection semiconductor suppliers (ON Semi, ST, Infineon, Analog Devices, TI) focus on current-limiting ICs and electronic circuit breakers, integrating protection with other LED driver functions (dimming, PWM, fault reporting). These players hold ≈30-35% of market value, primarily in premium and automotive segments. JCET (China) and other Asian manufacturers compete in value PPTC segment (US$0.05-0.15), serving domestic LED lighting manufacturers. The market is seeing integration trend: current-limiting ICs incorporating overvoltage, overtemperature, and reverse polarity protection (single-chip solution), while PPTC manufacturers improve voltage ratings (from 60V to 100V+) for automotive and industrial applications.

4. User Case Study & Policy Drivers

User Case (Q1 2026): Signify (formerly Philips Lighting) – global LED lighting manufacturer. Signify standardized on Bourns MF-RHS high-temperature PPTC for street lighting LED drivers (50W-200W). Over 18 months (2024-2025), deployed in 500,000+ street light fixtures across Europe and North America. Key performance metrics:

- Field failure rate due to overcurrent: reduced 82% (from 0.45% to 0.08% of fixtures annually)

- Driver warranty claims: reduced 65% (extended driver life from 5 to 7 years)

- Resettable protection eliminated service calls for fuse replacement (2,000+ calls eliminated annually)

- Operating temperature range: -40°C to +105°C (suitable for enclosed pole-mounted fixtures)

- Cost per driver: US$0.32 (PPTC) vs. US$0.08 (one-time fuse) – 4× higher component cost but lower total cost of ownership (reduced service visits)

Policy Updates (Last 6 months):

- UL 8750 (Light emitting diode (LED) equipment for use in lighting products) – Revision (December 2025): Mandates overcurrent protection for all LED drivers (Class 2 power sources exempt). Requires protection device to interrupt or limit current within 60 seconds at 2× rated current. Resettable protection (PTC) permitted.

- IEC 60598-1 (Luminaires – Part 1: General requirements and tests) – Amendment (January 2026): Adds overcurrent protection requirements for LED luminaires with integral drivers. Electronic protection (current-limiting ICs) recognized as equivalent to passive devices.

- China GB/T 4208-2025 (LED driver safety standard, effective July 2026): Requires overcurrent protection with specified trip time-current curves. Non-compliant LED drivers cannot receive CCC (China Compulsory Certificate) mark.

5. Technical Challenges and Future Direction

Despite strong adoption, several technical and market challenges persist:

- Trip time vs. overcurrent magnitude trade-off: PTC thermistors have slower trip time (0.1-10 seconds) than ICs (1-10 µs) but are less expensive. For high-sensitivity LED arrays (near max current rating), slower PTC may allow LED damage before protection trips. ICs required for sensitive applications (automotive, medical).

- Temperature derating: PTC hold current decreases at elevated temperatures (30-50% reduction at 85°C vs. 25°C). LED drivers operating in hot environments (enclosed fixtures, automotive under-hood) require over-specification (higher current rating) or active cooling.

- Resettable vs. one-time cost premium: Resettable protection (PTC, IC) costs 3-10× one-time fuses. Price-sensitive LED lighting segments (consumer bulbs, linear tubes) continue using one-time fuses, increasing failure-related service costs.

独家行业分层视角 (Exclusive Industry Segmentation View):

- Discrete high-reliability applications (automotive headlamps, street lighting, medical lighting, aerospace) prioritize resettable protection (no service access), wide temperature range (-40°C to +125°C), and fast trip time (<100 µs). Typically use current-limiting ICs or high-performance PTC (Littelfuse PolySwitch, Bourns MF-RHS). Key drivers are field reliability and reduced service calls.

- Flow process high-volume applications (consumer LED bulbs, LED strips, signage, backlighting) prioritize cost (US$0.05-0.20 per device), automated assembly (SMD), and adequate protection for expected life (10,000-25,000 hours). Typically use PPTC or one-time fuses from value-tier suppliers (JCET, Asian manufacturers). Key performance metrics are cost per million units and failure rate.

By 2030, LED overcurrent protection devices will evolve toward smart, integrated protection ICs. Prototype products (ON Semi, Infineon, TI) integrate current sensing, overtemperature protection, reverse polarity, and diagnostic reporting (I²C fault flag) into single 3×3mm QFN package. The next frontier is “predictive protection” – monitoring LED current trends over time, detecting degradation (increasing leakage current, decreasing dynamic resistance), and predicting failure before overcurrent event occurs. As PTC thermistor resettable fuses and current-limiting ICs continue improving performance-to-cost ratio, LED overcurrent protection devices will remain essential for LED lighting reliability across consumer, commercial, automotive, and industrial applications.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666 (US)

JP: https://www.qyresearch.co.jp

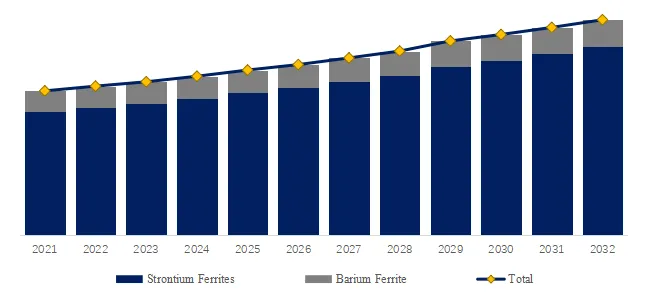

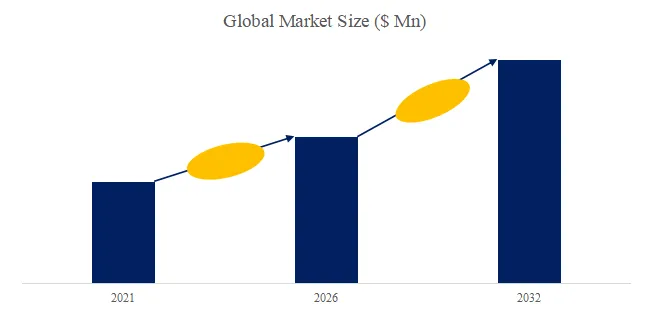

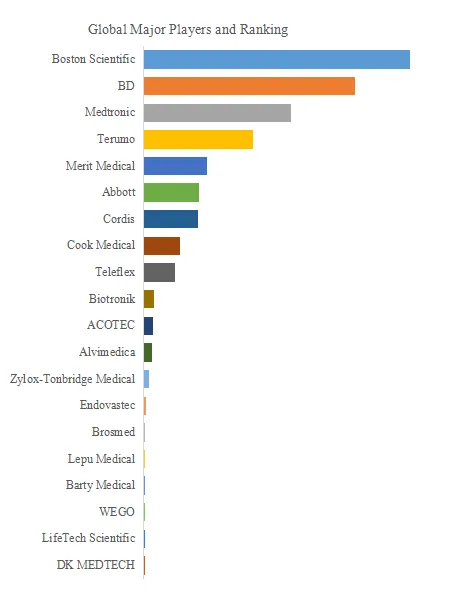

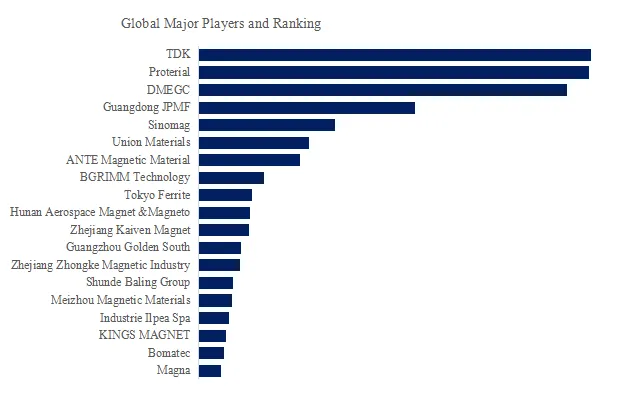

. Global Permanent Magnet Ferrite Magnet Top 19 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

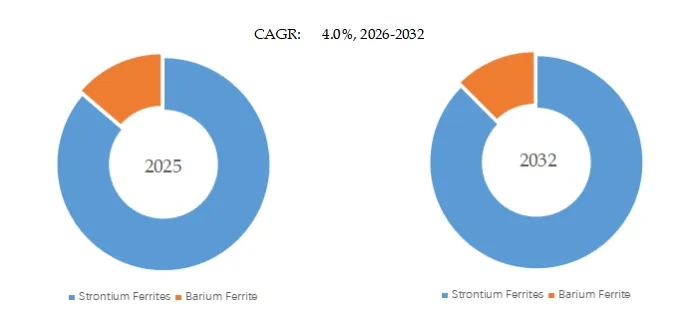

. Global Permanent Magnet Ferrite Magnet Top 19 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated) Permanent Magnet Ferrite Magnet, Global Market Size, Split by Product Segment

Permanent Magnet Ferrite Magnet, Global Market Size, Split by Product Segment