Vector Search Engine Market Summary

A vector search engine is a system that retrieves data based on high-dimensional vector representations. It converts unstructured data such as text, images, and audio into numerical vectors and uses similarity calculations (such as cosine similarity or Euclidean distance) to perform efficient matching in a large-scale vector space, thereby achieving semantic-level rather than keyword-level search. Its core relies on indexing and retrieval algorithms such as Approximate Nearest Neighbor (ANN), enabling it to quickly return the most similar results from massive amounts of data. It is widely used in semantic search, recommendation systems, multimodal retrieval, and large-scale model RAG (Retrieval Augmentation Generation), and is an important component of artificial intelligence and data infrastructure.

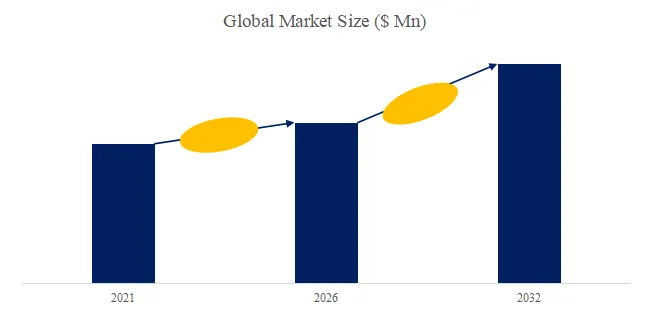

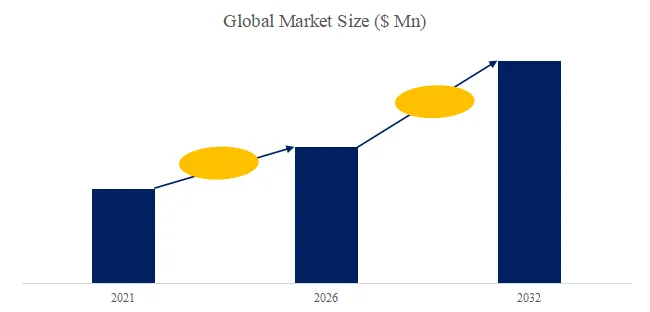

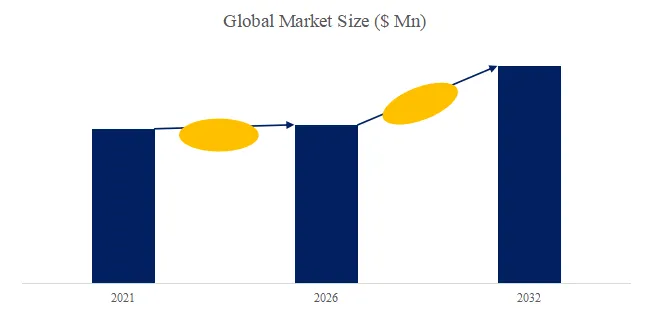

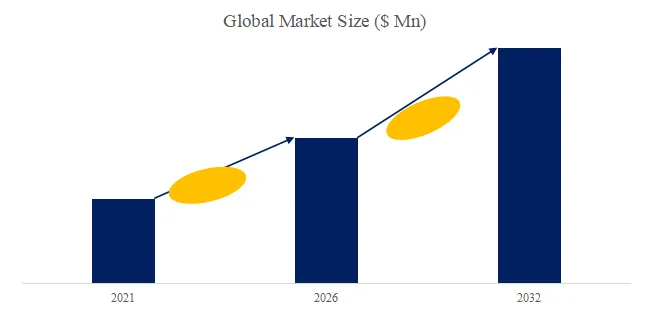

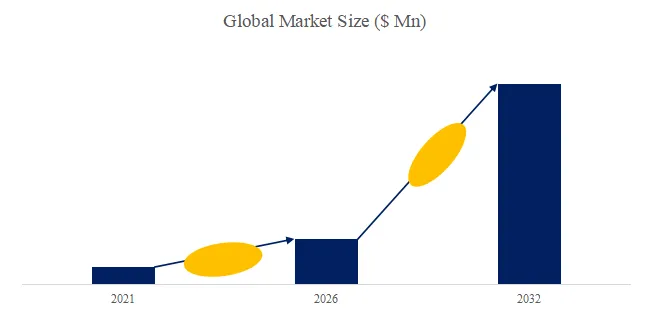

According to the new market research report “Global Vector Search Engine Market Report 2026-2032”, published by QYResearch, the global Vector Search Engine market size is projected to reach USD 20.28 billion by 2032, at a CAGR of 28.8% during the forecast period.

Figure00001. Global Vector Search Engine Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global Vector Search Engine Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

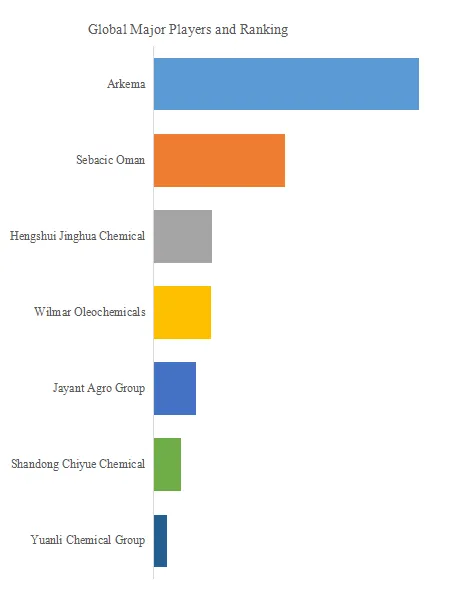

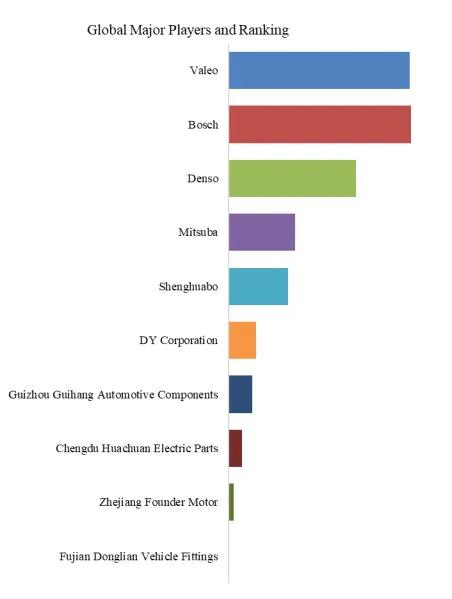

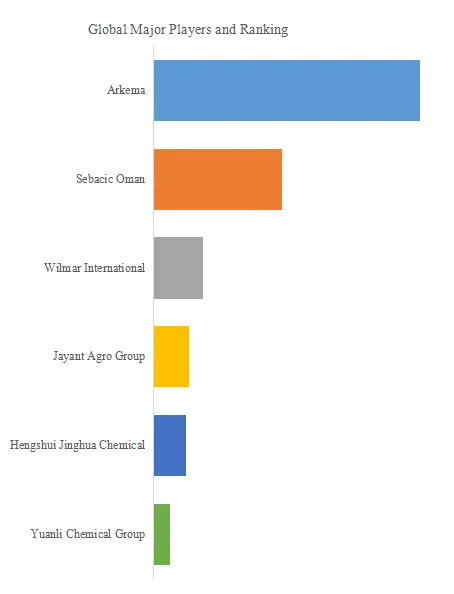

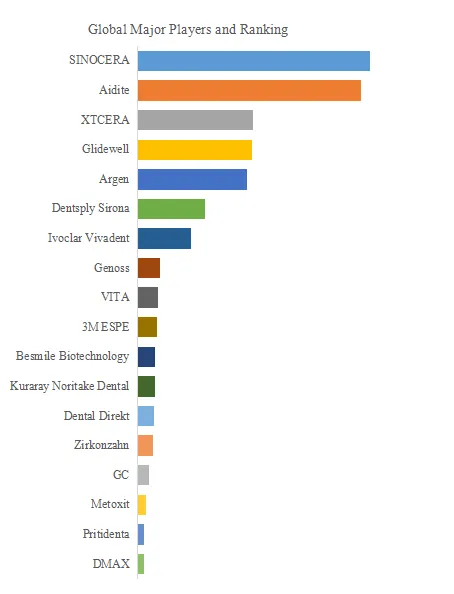

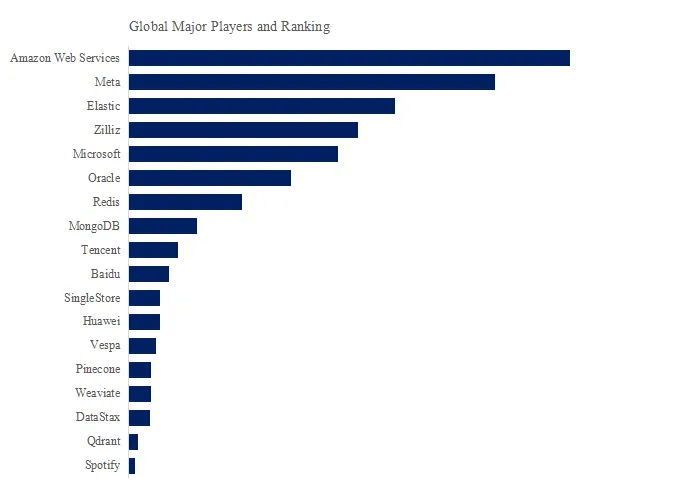

Figure00003. Global Vector Search Engine Top 18 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Vector Search Engine Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

According to QYResearch Top Players Research Center, the global key manufacturers of Vector Search Engine include Amazon Web Services, Meta, Elastic, Zilliz, Microsoft, Oracle, Redis, MongoDB, Tencent, Baidu, etc. In 2025, the global top five players had a share approximately 71.0% in terms of revenue.

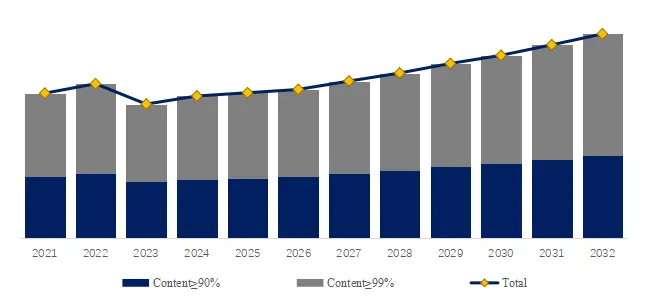

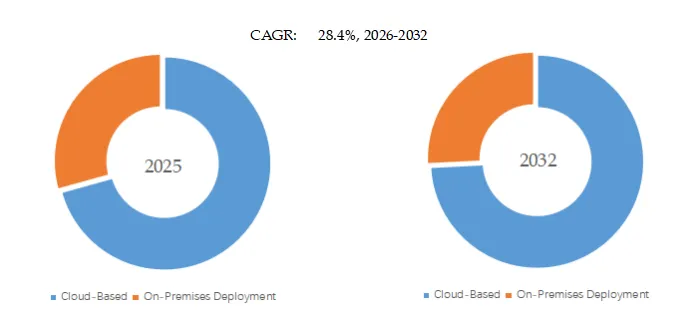

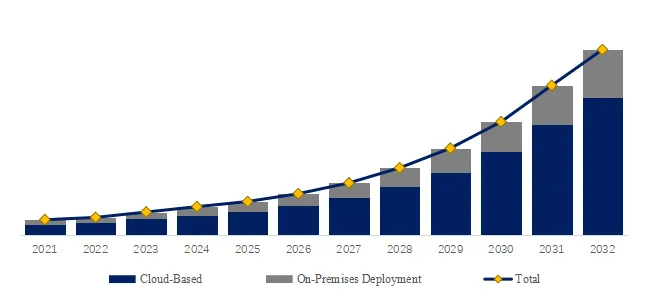

Figure00004. Vector Search Engine, Global Market Size, Split by Product Segment

Vector Search Engine, Global Market Size, Split by Product Segment

Based on or includes research from QYResearch: Global Vector Search Engine Market Report 2026-2032.

In terms of product type, Cloud-Based is the largest segment, hold a share of 70.7%,

Market Drivers:

Rapid Development of Generative AI and Large-Scale Models

A new wave of technologies, represented by large-scale models and generative AI, has made “semantic understanding” a core capability, rendering traditional keyword-based retrieval methods insufficient. Vector search engines, as a key infrastructure for RAG (Retrieval Augmentation), are widely used to provide external knowledge support for large models, significantly improving the accuracy and reliability of responses and becoming an essential component for AI applications.

Explosive Growth in the Scale of Unstructured Data

With the advancement of the internet and digitalization, the proportion of unstructured data such as text, images, videos, and audio continues to rise. Traditional databases struggle to perform efficient semantic retrieval of this type of data, while vector search, through embedding, maps data into high-dimensional vectors to achieve similarity matching, better unlocking data value and driving rapid demand growth.

Increasing Demand for Personalized Recommendations and Intelligent Search

E-commerce, content platforms, social media, and other industries are increasingly demanding accurate recommendations and personalized search. Vector search engines can perform similarity calculations based on user behavior and content semantics, significantly improving recommendation effectiveness and user experience, becoming a core technological support for recommendation systems, semantic search, and intelligent question answering scenarios.

Advances in Artificial Intelligence and Embedding Technology

Continuous breakthroughs in Natural Language Processing (NLP) and deep learning technologies have enabled more accurate vector representations (embeddings) of text, images, and other data. High-quality vector representations directly determine retrieval results. As model capabilities continue to improve, the accuracy and application scope of vector search are simultaneously increasing, further driving industry development.

Restraint:

High Technical Complexity and High Implementation Barriers: Vector search involves multiple layers of technology, including embedding modeling, vector indexing (such as ANN algorithms), similarity calculation, and system optimization, resulting in a complex overall architecture. Enterprises need to balance performance, accuracy, and cost in practical implementation, requiring strong algorithmic and engineering capabilities. Small and medium-sized enterprises (SMEs) often lack the relevant technical expertise, leading to barriers to application and promotion.

Retrieval Accuracy and Stability Remain Challenges: Vector search relies on embedding quality and Approximate Nearest Neighbor (ANN) algorithms. In large-scale data scenarios, inaccurate recall or unstable results may occur. Furthermore, different data types (text, images, etc.) have significantly different requirements for vector representation, affecting overall retrieval performance and limiting its application in high-precision scenarios.

High Computational Resource Consumption and Cost Pressure: Vector generation (embedding) and high-dimensional vector retrieval typically rely on GPUs or high-performance computing resources. In massive data scenarios, the demand for storage, computing power, and network bandwidth increases significantly. Enterprises face high infrastructure costs during deployment and operation, especially in real-time retrieval and large-scale concurrency scenarios.

Data Security and Privacy Compliance Risks

Vector search typically involves modeling and storing sensitive information such as internal enterprise data and user behavior data, posing risks of data leakage and misuse. Furthermore, increasingly stringent data protection regulations in different countries and regions present compliance challenges for enterprises deploying vector databases and processing cross-border data, hindering their application and promotion.

Low Standardization and Immature Ecosystem

The vector search industry is currently in its early stages of development, lacking unified technical standards and interface specifications. Significant differences exist between vendors in data formats, index structures, and query methods, leading to high system compatibility and migration costs. In addition, the immature toolchain and ecosystem also restrict the industry’s large-scale development.

Opportunity:

The accelerated commercialization of generative AI is driving incremental demand. As generative AI and large-scale models move from the experimental stage to large-scale commercial applications, enterprises are rapidly increasing their demand for “external knowledge access” and “real-time retrieval enhancement.” Vector search, as a core component of the RAG architecture, will continue to penetrate scenarios such as intelligent customer service, enterprise knowledge assistants, and code generation, leading to explosive market demand.

The trend towards private AI and localized deployment is strengthening. Due to data security and compliance requirements, more and more enterprises are inclined to build private large-scale models and local knowledge base systems. Vector search engines can support semantic retrieval and management of internal enterprise data, becoming a key infrastructure in private AI architectures, with broad development prospects in finance, healthcare, and government sectors.

The application of multimodal data fusion is rapidly expanding. Future data formats will be more diverse, and the demand for unified retrieval of multimodal data such as text, images, voice, and video continues to rise. Vector search is naturally adapted to multimodal embedding expressions, enabling cross-modal similarity searches (such as “image search” and “text search”), and has significant application opportunities in content platforms, security monitoring, and industrial vision.

Vertical industry solutions are continuously deepening. Vector search is evolving from a general-purpose tool to an industry-specific solution, forming customized applications in vertical fields such as e-commerce, finance, healthcare, and manufacturing. Examples include product recommendations in e-commerce, fraud detection in finance, and case matching in healthcare, driving the industry’s transformation from “technology-driven” to “scenario-driven” and enhancing business value.

About The Authors

|

Ziyi Fan |

|

| Lead Author |

| Consumer Goods,

Equipment & Parts, Packaging, etc. |

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 19 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp